管理人オススメコンテンツはこちら

「Strongest Insurance|明日への保証は世界最高レベルの最強の盾」

〜前回のつづき〜

●民間保険にムダ金払ってるあなたへ~最強の保険、もう国が用意してくれてますけど?~

あなたはすでに

世界最強の保険に

入っているんですよ。

これは色々有るんですけど

(1)健康保険

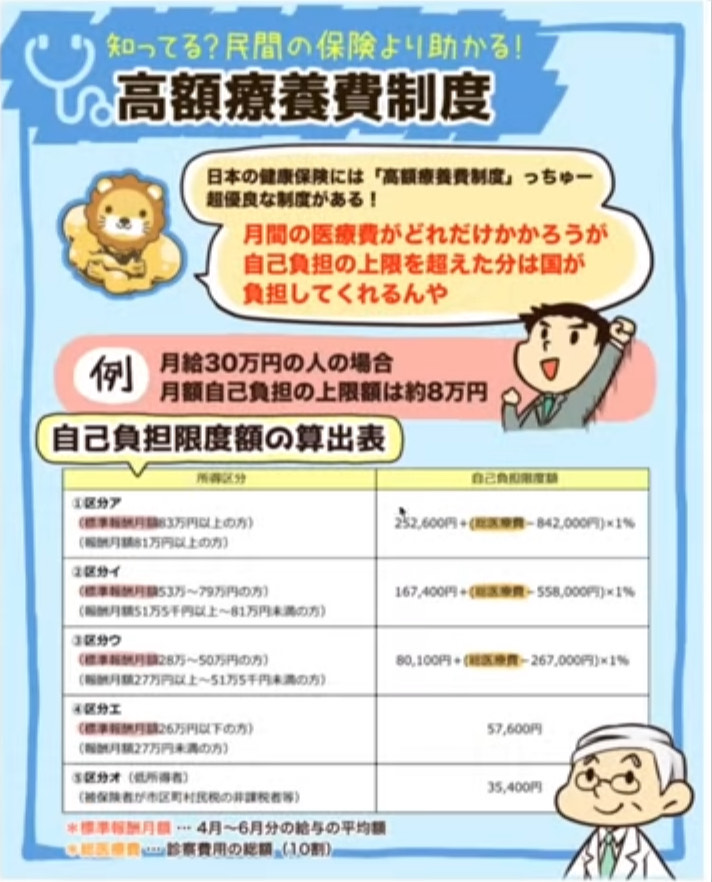

1-a)高額療養費制度

(出典:リベラルアーツ大学)

月間の医療費がどれだけ掛かっても

自己負担の上限を超えた分は

国が負担してくれる。

もっと言うと

保険適用の治療なのであれば

どれだけ治療費が掛かったとしても

普通の収入の人であれば

月額9万円前後ぐらいですね。

だから保険適用の治療が

◯百万円かかると言われても

実際自分が払う分は

これだけだという事ですね。

高額療養費制度は

・国民健康保険

・会社の健康保険

どっちも付いてます。

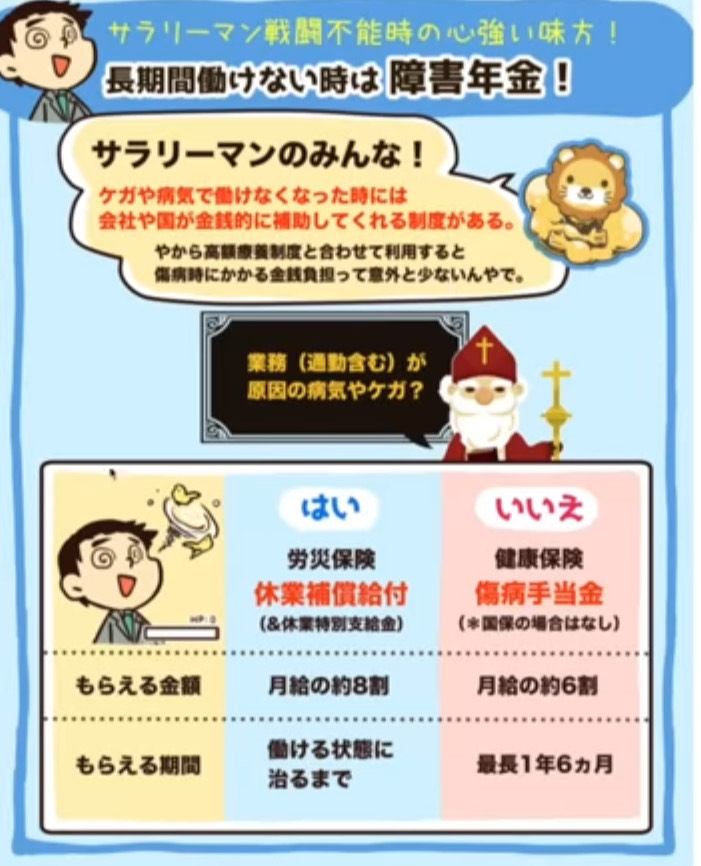

1-b)傷病手当金

(出典:リベラルアーツ大学)

サラリーマンの人だったら

特になんですけど

傷病手当金が付いてるんですよね。

これはどういう制度かと言うと

・病気

・怪我

そういうもので

働けなくなってしまった場合

大体月給の6割ぐらいを

1年6ヶ月もらえる。

急に病気で入院してしまって

給料が突然来月から無くなってしまっても

困りますよね?

でもこの傷病手当金が出るので

収入が無くなりはしない。

月給45万円の人だったら

30万円ぐらいは出ますから

だから

すぐ生活が困るという事は

少ないですよね。

セーフティネットとして

だいぶ優秀です。

そして大企業なのであれば

付加給付という制度も有って

入ってる健康保険組合の中に

上乗せがある場合も有ります。

そういう場合であれば

月給の7〜8割出たりすることが有るので

結構

大企業とかであれば

有ったりするので

ちょっとその辺を

確認してみてください。

この傷病手当金というのは

会社をクビになったとしても

ちゃんと支給されるので

ここはちゃんと

知っておきたいですよね。

その上でやはり

民間保険に入るかどうかというのを

判断したい。

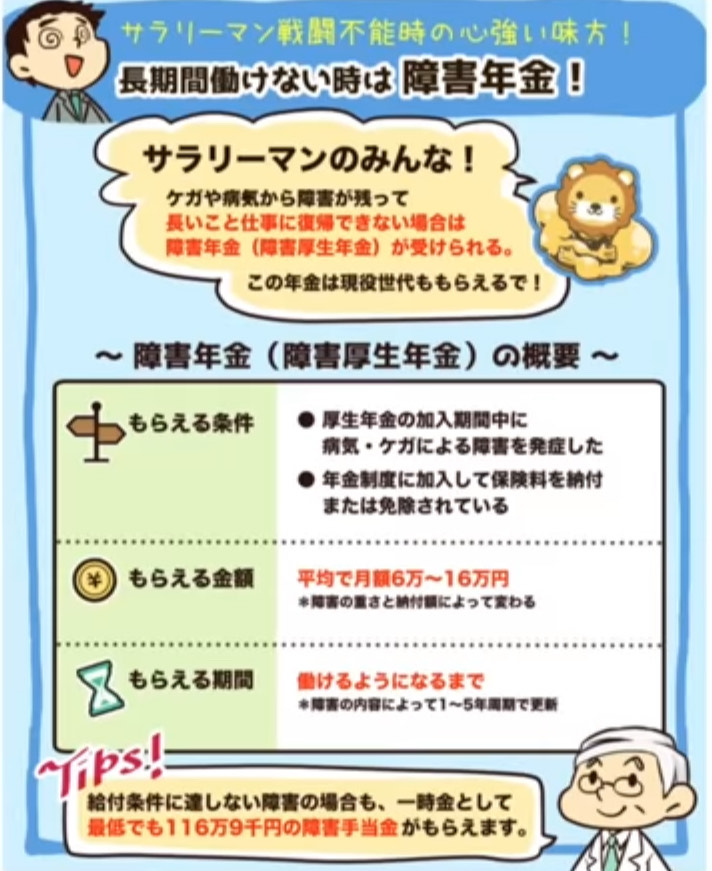

1-c)障害年金

(出典:リベラルアーツ大学)

それからプラスアルファ

障害なんかが残った場合とか

障害年金というのも出ますからね。

(2)有給休暇

国の制度とは

ちょっと違うんですけど

有給休暇も有る訳ですよね。

大きい企業であれば

有給休暇も有る。

だから

まず有給を使って

足りなかったら

傷病手当金の支給を受ける

という事もしていけるので

取れる取れないという話は置いておいて

この有給休暇というのも考えたい。

(3)失業給付

それから雇用保険の方からは

失業保険と呼ばれるものですよね。

もしかして

もしも病気や怪我が原因で

会社をクビになってしまった場合なんかでも

病気が原因で失業して

働ける状態になったとしたら

最大で10ヶ月の

失業給付が受けられる

可能性もある。

次の職を探してる間も

失業給付を受けられる

可能性があるという事です。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

2025年8月から、高額療養費制度の自己負担上限額が引き上げられます。例えば、年収370万円から770万円の一般的な収入層では、これまで約8万円だった月の自己負担上限が約8万8千円に増額され、約1割の負担増となります。

この制度は、医療費が高額になっても自己負担額に上限を設け、超過分を国が負担する仕組みで、多くの人が安心して治療を受けられるよう支えています。さらに、2027年8月には区分が細分化され、より高い収入層の負担上限も引き上げられる予定です。

こうした見直しは医療費の増加を背景に行われており、公的医療保険の持続可能性を確保するための措置です。民間保険に加入する前に、まずはこの国の充実した制度を理解し、活用することが大切です。

Citations:

[1] https://www.shiruporuto.jp/public/document/container/kogakuiryohi/

[2] https://www.mhlw.go.jp/stf/seisakunitsuite/bunya/kenkou_iryou/iryouhoken/juuyou/kougakuiryou/index.html

[3] https://www.kyoukaikenpo.or.jp/g3/sb3030/r150/

[4] https://www.city.meguro.tokyo.jp/kokuho/kurashi/kokuho/kokuho_kyufu_kogaku.html

[5] https://www.life8739.co.jp/product/iryo/column02

≪≪Chat-GPTくんによる英訳≫≫

~Continuing from the previous message~

【Still wasting money on private insurance? The ultimate coverage — the government’s already got you covered.】

You’re already enrolled in the world’s strongest insurance.

There are several key aspects to it:

1. Health Insurance

a) High-Cost Medical Expense System

(Reference: Liberal Arts University)

No matter how much medical treatment costs per month, the government will cover the amount that exceeds the set limit of your out-of-pocket expenses.

To put it simply, if the treatment is covered by insurance, no matter how expensive it gets, for an average income person, the out-of-pocket cost is about 90,000 yen per month.

Even if the treatment costs hundreds of thousands of yen, you’ll only need to pay this much.

The High-Cost Medical Expense System applies to:

National Health Insurance

Company Health Insurance

b) Sickness and Injury Allowance

(Reference: Liberal Arts University)

For salaried workers, this allowance is particularly important.

If you’re unable to work due to illness or injury, you can receive about 60% of your monthly salary for up to 18 months.

For example, if you suddenly get sick and can’t work next month, and your salary is suddenly cut off, it would be tough, right?

But with this allowance, you won’t lose all your income.

For a person with a monthly salary of 450,000 yen, around 300,000 yen will be provided.

This is an excellent safety net.

Additionally, large companies might offer an additional benefit, which could top up the allowance to 70-80% of your salary, depending on the health insurance union you’re enrolled in.

If you’re in a large company, check if this benefit is available.

This sickness and injury allowance is also paid if you lose your job, so it’s important to be aware of this.

With this knowledge, you can then make an informed decision on whether or not to purchase private insurance.

c) Disability Pension

(Reference: Liberal Arts University)

Additionally, if you are left with a disability, you can also receive a disability pension.

—

2. Paid Leave

While it’s not a government program, paid leave is available.

If you work in a large company, paid leave is likely part of your benefits.

So, you can first use your paid leave, and if that’s not enough, you can also receive sickness and injury allowance.

You should think about the availability of paid leave when considering your options.

—

3. Unemployment Benefits

Unemployment benefits from employment insurance are also available.

If you lose your job due to illness or injury, and if you’re capable of working again, you can potentially receive up to 10 months of unemployment benefits while looking for a new job.

You might also receive unemployment benefits while searching for a new position.

Special Thanks OpenAI and Perplexity AI, Inc