管理人オススメコンテンツはこちら

「本当にヤバい金利|一歩踏み外せば、借金炎上アメリカン・ドリーム」

〜前回のつづき〜

●借金に依存するアメリカ人の実態(つづき)

2010年以降

約107兆円も消費者ローンが増えて

消費者ローンの総額は

約450兆円有ると言われています。

そのうち4分の1を占める

カードローンの平均金利は何と

17%なんですよ。

高いですよね!

この17%という金利を聞いて

「あ!ヤバい!」

とすぐにピンと来た人は

マネーリテラシーが高いですね。

17%という金利が

高いか低いかわからないという人は

まだちょっとこれから

勉強していく必要が有りますね。

17%という金利が

どれだけヤバい金利かというと

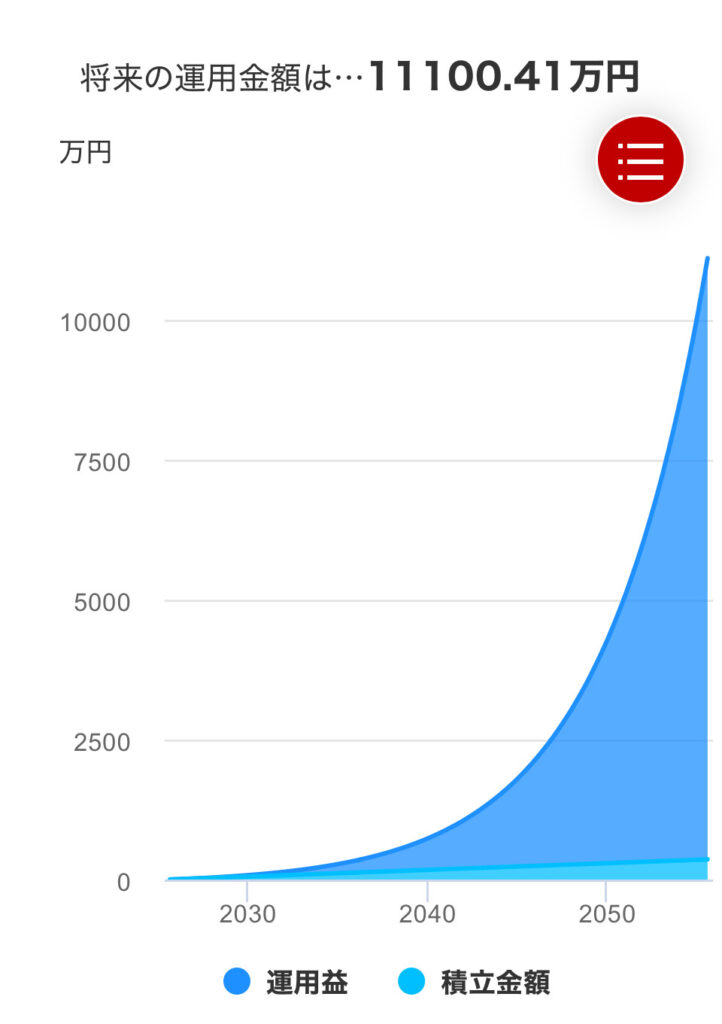

毎月1万円積み立てて

利回り17%で30年間運用すると

なんと元本360万円が

1億1千万円になるんですよ。

これって

すごい数字だと思いませんか?

利回り17%ですよ。

30年間毎月1万円ずつ

積み立てていくだけで

利回り17%だと

1億1千万円になるんですね。

本当にヤバい金利なんですね。

(出典:Amazon)

モシェ・ミレブスキー著

『人生100年時代の資産管理術』によると

典型的なアメリカ人家計は

約50〜200万円の

消費者ローンを抱えてるんですよ。

これに住宅ローンなんかも加えると

35歳未満の世帯では

資産と負債の比率が

ほぼ1:1になってるらしいんですね。

言い換えると

もしあなたが300万円貯金するとしたら

借金も300万円有るという状態なんですね。

結構ビビりませんか?

300万円持ってるかもしれないけど

300万円借金も有るという状態。

結構ドキドキしますよね?

しかも消費者ローンですよ。

更に学生ローンも

激増中なんですよ。

2008年には

6,400億ドルだったのが

2018年には

1兆4,600億ドルという事で

学生ローンが

非常に増えてるんですね。

アメリカでは

学費を借金でまかなうというのは

普通の事で

現在4,500万人もの人が

学生ローンの支払いに

追われてるんですね。

約300万円の借金を抱えて

4年制の大学を

卒業するという事で

これが卒業した時に

借金を抱えている状態で

これが平均的な数字なんですよ。

借金の返済が

出来なくなっちゃう人も

当然少なくない訳ですよ。

なので

民主党の大統領選に出馬している

議員候補のほぼ全員が

学生の債務を減らす

政策を打ち出していて

「学生ローンを全て帳消しにする!」

という政策が

一番人気になってるんですね。

そのぐらい政府や国民の関心が

非常に強いテーマなんですね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

2010年以降、アメリカの消費者ローンは約107兆円増加し、総額は約450兆円に上ります。その25%を占めるカードローンの平均金利は17%と非常に高く、これは毎月1万円を30年積立運用すれば元本360万円が1億1千万円になるほどの複利効果を生む水準です。多くの家庭は約50〜200万円の消費者ローンを抱え、住宅ローンも含めると35歳未満の世帯では貯金と借金がほぼ同額という不安定な構造です。

さらに、学生ローンも激増し、卒業時に約300万円の借金を抱えてスタートするのが平均的となっています。学生ローン救済政策が大統領選の主要争点になるほど、ローン問題はアメリカ社会で深刻な課題です。

- https://www.experian.com/blogs/ask-experian/research/consumer-debt-study/

- https://www.statista.com/chart/19955/household-debt-balance-in-the-united-states/

- https://www.statista.com/statistics/248258/consumer-credit-sector-debt-in-the-united-states/

- https://www.debt.org/faqs/americans-in-debt/demographics/

- https://www.ceicdata.com/en/indicator/united-states/household-debt

- https://fred.stlouisfed.org/series/CCLACBW027SBOG

- https://www.newyorkfed.org/microeconomics/hhdc

- https://www.federalreserve.gov/releases/z1/dataviz/household_debt/msa/table/

- https://www.federalreserve.gov/releases/g19/current/

- https://fred.stlouisfed.org/series/HDTGPDUSQ163N

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous section~

【The Reality of Americans Dependent on Debt (continued)】

Since 2010,

consumer loans have increased by about ¥107 trillion.

Today, the total amount of consumer loans in the U.S. is said to be around ¥450 trillion.

Of that, one-quarter is made up of credit card loans,

with an average interest rate of 17%.

Pretty high, right?

If you hear “17% interest” and immediately think,

> “Whoa, that’s bad!”

> then your financial literacy is quite high.

But if you’re not sure whether 17% is high or low,

you still have some learning to do.

Just to show you how dangerous a 17% interest rate really is—

If you invest ¥10,000 per month at an annual return of 17% for 30 years,

your total contributions of ¥3.6 million would grow to ¥110 million!

Isn’t that an incredible number?

That’s the power of 17% returns.

Simply by saving ¥10,000 every month for 30 years at 17%,

you end up with ¥110 million.

That’s how truly insane that interest rate is.

(Source: Amazon)

According to Moshe Milevsky’s book

“Your Money Milestones: A Guide to Financial Security in the Age of Longevity,”

the typical American household carries between ¥500,000 and ¥2 million in consumer debt.

When you add mortgages and other liabilities,

for households under 35 years old,

their assets and debts are nearly 1:1.

In other words,

if you’ve saved ¥3 million,

you likely have ¥3 million in debt as well.

That’s pretty scary, isn’t it?

You might have ¥3 million in the bank—

but also owe ¥3 million.

Kind of makes your heart race, doesn’t it?

And remember, we’re talking about consumer loans here.

What’s worse, student loans have been skyrocketing too.

In 2008, the total student loan debt was $640 billion,

but by 2018 it had ballooned to $1.46 trillion.

In the U.S., it’s completely normal to borrow money to pay for college tuition.

Currently, 45 million Americans are struggling to pay off their student loans.

The average graduate leaves a four-year university with about ¥3 million (roughly $25,000) in debt.

That means most students start their working lives already in debt.

And of course, not everyone can keep up with their loan payments.

That’s why, among Democratic presidential candidates,

almost every one has proposed policies to reduce student debt,

with the most popular one being:

> “Cancel all student loans!”

That’s how deeply this issue has captured the attention

of both the government and the American people.

Special Thanks OpenAI and Perplexity AI, Inc