管理人オススメコンテンツはこちら

「泣きっ面に蜂|未来が読めない時代に老後資金を計算するという無謀」

〜前回のつづき〜

●老後資金を計算出来ない理由(つづき)

(2)老後の年数

こっちは更に難易度が高くて

・何歳で退職するのか

・何歳まで生きるのか

両方ともかなり

予測しにくいですよね?

定年というものだけ見ても

この40〜50年の間に

15年も伸びてるんですね。

最近も70歳定年法が

話題になってましたけど

退職するのは

・65歳

・70歳

・75歳

退職直前の年収を

400万円とした場合

5年間働くだけで

2千万円も

稼げる事になる訳ですよね?

だからいつまで働くかで

老後資金の必要額というのは

何千万円も違ってくる訳ですよね?

ここでも必要な金額が

大きく変わってくる。

寿命の予測なんて

更に最難関で

FPに相談しても

多分こんなふうに

言われるんですよね。

・とりあえず平均寿命で考えて

・あなたが何歳まで生きたいかでイメージして

など

そう言うしか無いですよね?

・あなたの命は何歳何ヶ月で尽きるんです

なんて事は誰にも言えない訳ですね。

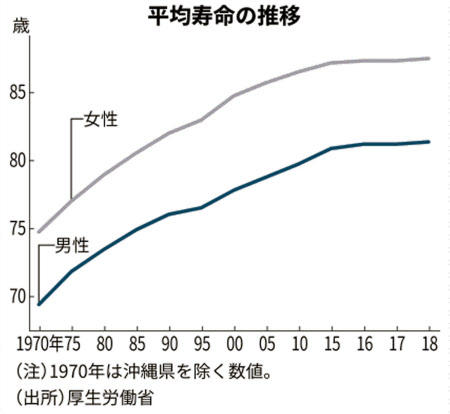

男性の平均寿命は

81歳ぐらいですけど

現在30代の人は

95歳ぐらいまで生きると

言われています。

更にこの平均寿命は

ひらすら伸び続けています。

(出典:https://www.nikkei.com/article/DGXMZO47950740Q9A730C1CR8000/)

日本で

2007年に生まれた子供の50%は

何と107歳まで生きると

言われてるんですね。

ドンドン平均寿命というのは

伸びてるんですね。

色々な情報が有る中で確かな事は

人の寿命は誰にもわからない

という事ですよね。

これが確かな事ですよね。

老後資金を計算するための

2つの要素

(1)年間生活費

(2)老後の年数

この2つとも

わからないんですよ。

だから

老後資金の必要額もわからない。

論理的に考えて

当然の事ですよね。

しかも更に

何とか年間生活費と老後年数で

老後資金を出したとしても

そのうちどれだけの金額を

公的年金でカバー出来るか

わからないんですね。

今50代以降の人は

現実の年金受給額に近い数字が

わかるんですけど

若い世代の場合は

「年金?本当にもらえるの?」

と泣きっ面に蜂状態ですね。

こういう状況なので

老後資金のシミュレーション結果に

ピンと来ないというのは

当たり前なんですね。

だからみんな

モヤモヤした感覚を抱えて

生きている。

「何となく

それぐらいいるかもしれないけど

なんかちょっとピンと来ない・・・」

みたいな感じですよね。

ではどうすればいいのか?

今の20〜40代の若い世代は

一体どうやって老後に備えればいいのか?

という話になってくるんですね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

老後資金を計算するのが難しい理由は、退職時期や寿命など予測できない要素が多いからです。

例えば定年の年齢も過去の数十年で大幅に延び、今では70歳定年も話題です。65歳で退職するか、70歳まで働くかで、5年間で2千万円もの収入差が生まれます。

また、寿命も確実には分かりません。

平均寿命は現在も延び続けており、2007年生まれの日本人の半数が107歳まで生きるとも言われています。

老後資金の計算には「年間生活費」と「老後の年数」が必須ですが、そのどちらも正確には分かりません。

さらに公的年金が将来どれだけ受け取れるかも不透明です。

このため、若い世代ほど老後資金のシミュレーションに現実感を持ちにくく、将来に対する不安やモヤモヤを抱えやすい状態にあります。

- https://www.nikkei.com/article/DGXZQOUB167XE0W5A610C2000000/

- https://news.yahoo.co.jp/articles/4fa31927b54d1479a316a565f560b0d0c425b974

- https://diamond.jp/articles/-/271577

- https://jinjibu.jp/article/detl/hr-survey/2431/

- https://www.sankei.com/article/20250524-ZHVIAS32VBOYBFL27EERN7UOBY/

- https://www.nikkei.com/article/DGXZQOUC160JK0W5A110C2000000/

- https://news.yahoo.co.jp/expert/articles/3c83c144a76d1c75e113a099cfd4ed42a85536aa

- https://sdgs.yahoo.co.jp/originals/239.html

- https://ksi-corp.jp/topics/survey/2024/web-research-72.html

- https://news.yahoo.co.jp/articles/f500c5eb4f81632e3c531ca912f26fa499bdcf30

- https://www.nttdata-strategy.com/newsrelease/201202.html

- https://news.yahoo.co.jp/articles/53e6b6f7408001d6e08f2bded4a18ce9dcf9d232

- https://works-via.co.jp/article/retirement-funds/

- https://www.yomiuri.co.jp/column/wideangle/20240520-OYT8T50004/

- https://diamond.jp/articles/-/349815

- https://www3.nhk.or.jp/news/html/20250328/k10014763211000.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from last time~

【Why We Can’t Calculate Retirement Funds (continued)】

(2) Number of Retirement Years

This one is even more difficult:

At what age will you retire?

Until what age will you live?

Both are extremely hard to predict, aren’t they?

Even if we just look at the retirement age, it has already been extended by 15 years over the past 40–50 years.

Recently, the idea of setting the retirement age at 70 has also been in the news.

So, will you retire at:

65?

70?

75?

If your annual income just before retirement is 4 million yen, then working for an extra 5 years would bring in as much as 20 million yen.

That means the age at which you stop working can make a difference of tens of millions of yen in how much retirement savings you’ll actually need.

So again, the amount you’ll need changes drastically.

Predicting your lifespan is an even greater challenge.

Even if you ask a financial planner, they’ll probably just say things like:

“For now, let’s plan based on the average life expectancy.”

“Imagine how long you’d like to live.”

That’s really all they can say, isn’t it?

Nobody can ever tell you,

“Your life will end at exactly XX years and XX months.”

The average life expectancy for men is about 81 years.

But it’s said that people currently in their 30s will live until around 95.

And what’s more, life expectancy just keeps increasing.

(Source: [https://www.nikkei.com/article/DGXMZO47950740Q9A730C1CR8000/](https://www.nikkei.com/article/DGXMZO47950740Q9A730C1CR8000/))

In fact, half of the children born in Japan in 2007 are expected to live to 107.

Life expectancy just keeps climbing.

Among all this information, the one certain fact is:

Nobody knows how long a person will live.

That much is certain.

Now, there are two elements needed to calculate retirement funds:

1. Annual living expenses

2. Number of retirement years

But the truth is, we don’t know either of them.

And that’s why we can’t know how much retirement savings we’ll need.

Logically, it’s only natural, right?

And even if you somehow managed to estimate your retirement savings based on annual expenses and retirement years, there’s still no way of knowing how much of that amount will be covered by public pensions.

For those currently in their 50s and older, it’s possible to get a figure close to the actual amount of pension they’ll receive.

But for younger generations, it’s more like:

“Pensions? Will we even get them at all?”

A double whammy.

Given this situation, it’s no wonder that people don’t really connect with the results of retirement fund simulations.

So everyone ends up living with this vague, uneasy feeling.

“Somehow…

I feel like I might need that much,

but it just doesn’t quite click…”

That’s the kind of feeling, isn’t it?

So, what should we do?

For today’s younger generations in their 20s to 40s,

the real question becomes:

How should they prepare for retirement?

Special Thanks OpenAI and Perplexity AI, Inc