管理人オススメコンテンツはこちら

「悲観する必要は無い|“破綻しない”年金のカラクリ、あなたは知ってる?」

今日は【総論】

年金の受給額は少なくなるのか?

悲観的になりすぎなくても良い3つの理由

というお話しをします。

●年金は消えない〜何もしなければ“安心”は消える〜

知り合いが相談を受けたそうです。

「なんとか生活を安定させたいと

考えている30代独身の契約社員です。

老後資金として年金以外に

2千万円必要という話に

不安が大きくなるばかりです。

結局年金は

もらえなくなってしまうのでしょうか?

もらえたとしても

生活が成り立たなくなるほど

少なくなるのでしょうか?

自分なりに調べても

ややこしくて

あまりよくわかりません。

わかりやすく

解説してもらえないでしょうか?」

とのこと。

私個人としては

年金制度について

そこまで

悲観する必要は無いのではないかと

思っています。

今回は

年金に悲観的になりすぎなくても良い

3つの理由についてお話しします。

まず前提について

2点確認なんですけど

私の考えでは

年金制度の完全な破綻は

無いのではないかと思います。

前提1:年金制度が完全に破綻するには3つの条件が同時に起きる必要がある

なぜかというと

年金がもらえなくなる

3つの条件というのが

同時に満たされる事が

あり得ないからです。

その条件とは

条件(1)現役世代が誰も年金保険料を納めない

条件(2)誰も税金を納めない

条件(3)積立金が完全に枯渇する

この3つが同時に起きないと

年金が完全に破綻するという事は

あり得ません。

これについては

#106 老後資金が2000万円不足?年金は崩壊するのか?どう備えれば良い?

↑

こちらでもう少し

詳しくお話ししていますので

参考にしてみて下さい。

前提(2)所得代替率について

年金制度が完全破綻して

もらえる年金が

ゼロになるという事は

あり得ないと思いますが

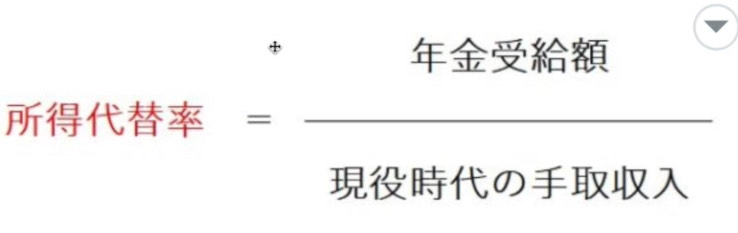

所得代替率は

減っていくという事が

わかってるんですよね。

(出典:リベラルアーツ大学)

また後でお話ししますけど

この所得代替率とは何かというと

現役時の収入の何%を

年金で賄えるかという

指標なんですね。

『年金受給額』とは

会社員と専業主婦世帯の

標準的な受給金額ですね。

『現役時代の手取り収入』とは

被保険者の平均手取り収入の事です。

なんとなくそうなんだと

聞いてもらえれば

よろしいかと思います。

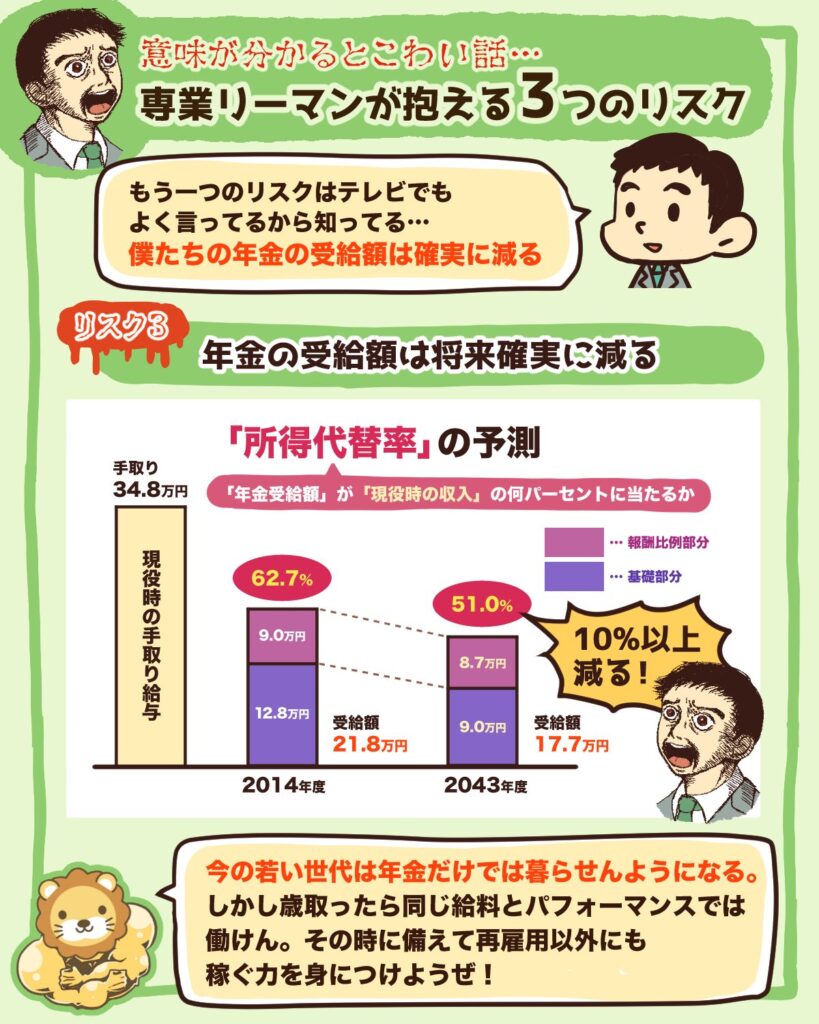

厚生労働省が出してるモデルで

平成26年の所得代替率というのを

見てみると

.jpeg)

こんな感じになってるんですね。

所得代替率は

62.7%という事になりました。

現役の時に

34.8万円もらってて

もらえる年金が

21.8万円ということは

現役の時の所得代替率は

62.7%もらえる。

公的年金の給付水準は

この所得代替率で

考える事になっています。

の所得代替率について-1024x364.jpg)

(出典:https://www.shaho-net.co.jp/nenkin_guide/98.html?utm_source=chatgpt.com)

また2024年のデータだと

61.2%まで下がっています。

その数値はこれから

40〜50%程度になると

予測されてるんですね。

前提のまとめとしては

年金制度が破綻する確率は

著しく低い。

所得代替率は

62.7%から40〜50%に減少する。

こう聞くと

「年金が2〜3割も減るかもしれないのに

なぜ悲観的にならなくてもいいというのか?

大丈夫なのか?」

と思いますよね?

「破綻はしないかもしれないけど

2〜3割も年金が減っちゃったら

ヤバいんじゃないの?」

と思いますよね?

悲観的にならなくてもいい理由3つを

これからお話しします。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

年金制度については、「将来もらえなくなるのでは?」という不安がよく聞かれますが、過度に悲観する必要はありません。

完全に破綻するには、現役世代が誰も保険料を払わず、税金収入もなく、積立金もゼロになるという3つの条件が同時に起きる必要があり、現実的には極めて起こりにくいからです。

確かに、公的年金の給付水準を示す所得代替率は、平成26年の62.7%から2024年は61.2%に下がり、将来は40〜50%程度になると予測されています。

しかし、これは年金がゼロになるわけではなく、減少分は資産形成や生活設計で補うことが可能です。

重要なのは、「年金は必ず一定額は受け取れる」という前提で、早めに老後資金の準備を始め、将来の生活を安定させる戦略を立てることです。

-

- https://www.aeon-allianz.co.jp/mane-kineko/article/page048.html

- https://www.nikkei.com/article/DGXZQOUB193Z40Z10C24A2000000/

- https://financial-field.com/pension/entry-160106

- https://money-bu-jpx.com/news/article054290/

- https://www.shaho-net.co.jp/nenkin_guide/98.html

- https://www.mbs.jp/news/feature/specialist/article/2025/03/105689.shtml

- https://www.am-one.co.jp/hagukumu/article/column-20240731-1.html

- https://kumitateru.jp/media/series/R240909001

- https://www3.nhk.or.jp/news/html/20241125/k10014648871000.html

- https://www.mhlw.go.jp/nenkinportal/chapter2/topic03.html

- https://diamond.jp/zai/articles/-/209359

- https://shuchi.php.co.jp/article/5959?p=3

- https://restyle.tokyo/forbeginners/collapse-pension.html

- https://diamond.jp/articles/-/7927

- https://news.yahoo.co.jp/articles/d0a0a9a9439bf4cfe57e8eff80b800590f106ce0

- https://www.smbc.co.jp/kojin/money-viva/money-news/0017/

≪≪Chat-GPTくんによる英訳≫≫

Today’s Topic: General Overview

Will pension benefits decrease?

Three reasons why you don’t have to be overly pessimistic.

—

Pensions will not disappear – but if you do nothing, your “peace of mind” will.

An acquaintance of mine recently received this consultation:

> “I’m a single man in my 30s, working as a contract employee.

> I’ve heard that, in addition to my pension, I’ll need 20 million yen for retirement.

> This only makes me more anxious.

>

> Will pensions eventually stop being paid?

>

> Even if I do receive one, will it be so small that I can’t make a living?

>

> I tried researching it myself, but it’s complicated and I don’t really understand.

>

> Could you explain it to me in simple terms?”

Personally, I don’t think we need to be overly pessimistic about the pension system.

Today, I’ll talk about three reasons why you don’t have to be overly pessimistic about pensions.

—

Before that, I want to confirm two points of premise.

—

Premise 1:

I believe the complete collapse of the pension system will not happen.

Why?

Because for pensions to become completely unavailable, three conditions would have to occur at the same time, and that’s highly unlikely.

The conditions are:

1. No one in the working-age population pays pension premiums.

2. No one pays taxes.

3. The reserve funds are completely depleted.

Unless all three of these happen simultaneously, a total collapse of the pension system is impossible.

(I talk about this in more detail in

\[#106 Will you be short 20 million yen for retirement? Will pensions collapse? How should you prepare?])

—

Premise 2: The “Income Replacement Rate”

I don’t think the pension system will collapse entirely and leave us with zero benefits.

However, we do know that the income replacement rate will decrease.

(The term “income replacement rate” comes from Liberal Arts University.)

In short, the income replacement rate is the percentage of your pre-retirement income that can be covered by your pension.

Pension benefit amount: the standard amount received by a model household (a company employee and a full-time homemaker).

Pre-retirement take-home income: the average take-home income of an insured worker.

—

Looking at the Ministry of Health, Labour and Welfare’s model for 2014 (Heisei 26):

Pre-retirement monthly income: ¥348,000

Monthly pension benefit: ¥218,000

Income replacement rate: 62.7%

Public pension benefit levels are considered in terms of this income replacement rate.

(Reference: [https://www.shaho-net.co.jp/nenkin\_guide/98.html](https://www.shaho-net.co.jp/nenkin_guide/98.html?utm_source=chatgpt.com))

In 2024, that figure has already dropped to 61.2%.

It’s projected to fall further to around 40–50% in the future.

—

Summary of the premises:

The probability of the pension system collapsing is extremely low.

The income replacement rate will decrease from 62.7% to around 40–50%.

—

Hearing this, you might think:

> “If pensions might drop by 20–30%, why shouldn’t I be pessimistic? Is that really okay?”

Or:

> “It might not collapse, but if my pension is cut by 20–30%, that’s still bad, right?”

That’s why I’ll now explain three reasons you don’t have to be overly pessimistic.

Special Thanks OpenAI and Perplexity AI, Inc