管理人オススメコンテンツはこちら

「小金持ちへのファーストステップ|月5万円の副収入が、あなたを“その他大勢”から救う」

〜前回のつづき〜

●大金持ちになれる方法と小金持ちになれる方法(つづき)

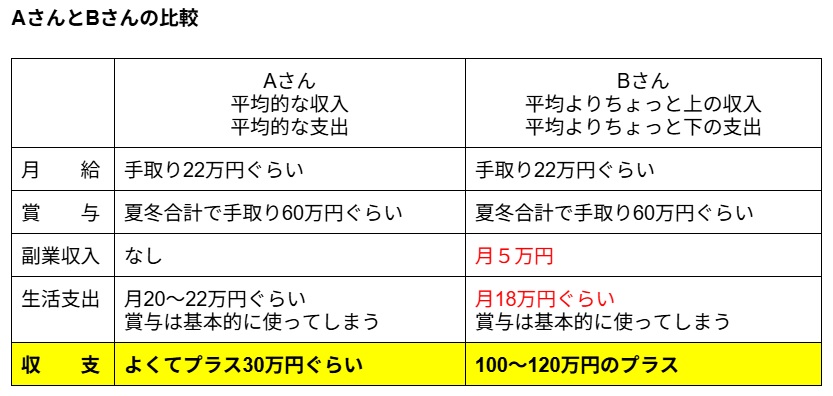

平均的なAさんと

小金持ちチューニングのBさんを

比べてみると

こんな感じになるんですね。

・平均的な収入

・平均的な支出

のAさんと

・平均よりちょっと上の収入

・平均よりちょっと下の支出

というBさん。

この違いですね。

小金持ちチューニングBさんは

副業で月に5万円多く稼いで

生活費を平均的な水準より

10〜20%落とすだけで

100〜120万円

貯められるようになるんですね。

これが小金持ちへの

ファーストステップなんですよ。

このお金を

平均よりちょっと上の

投資利回りで運用してみる。

優良なインデックスファンド

例えば

・eMaxis Slim S&P500

・eMaxis Slim オールカントリー

など今は色々有ります。

リスクを取って

この比率を高めれば

他の投資家たちの平均成績よりも

いい成績が出せる可能性が

高い訳ですね。

例えば

Bさんの場合はこうして

利回り5%ぐらいで運用を続ける。

Aさんの場合は

ひたすら毎年30万円を

貯金するだけ。

この二人を比べた場合

最終的にAさんとBさんは

.jpg)

(BさんとAさんの資産額推移)

こんなに差が付くんですよ。

青色がBさんの資産です。

赤色のこの小さい方が

Aさんの資産という事で

これだけ30年の間で

差が付くんですよ。

すごいですよね。

小金持ちチューニングのBさんは

54才の時点で

資産5千万円を突発する。

人生100年時代と言われる

日本において

ゼロから始めて

50代で上位8%の小金持ちに入れたら

十分だと思いませんか?

違いはこれだけなんですよ。

Aさんは

平均的な収入で

平均な支出をしていた。

Bさんは

平均よりちょっと上の収入で

平均未満の支出をしていた。

これが将来的に

とんでもなく大きな差に

なる訳ですね。

この事に気がついた人は

必ず小金持ちになれる訳ですね。

ゼロから始めてという事なので。

「25年も時間がかかるんじゃぁ

夢が無いよなぁ」

と思うかもしれないですけど

これは一例ですから。

副収入等で

5万円稼いだ場合の話なので

もっと稼ぐという事も

やっていけば

十分出来るでしょうし

5万円副業で稼げる人というのは

もっと稼げるようになりますから。

そうすると

もっともっと時間というのは

早まりますし

生活の支出というのも

コツを覚えてきたら

もっと下げる事が出来る。

これはあくまでも一例であって

まずここの違いに気づく

というのが大事だという事です。

大体否定したり

やらない理由から探す人というのは

「そんな25年後の事なんて考えたくないよ!」

とか

そんな所からスタートするんですけど

25年後に

いきなりドーンと

金持ちになる訳じゃない。

それまでの間に

どんどん良くなっていく

という事なので

今日から始めることで

来年も良くなってるという

事なんですね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

平均的な収入・支出のAさんと、収入をやや増やし支出をやや減らす「小金持ちチューニング」のBさんを比較すると、資産形成に大きな差が生まれます。

Bさんは副業などで月5万円多く稼ぎ、生活費を平均より10~20%削減することで年間100万円以上を貯蓄し、それをインデックスファンドなどで運用していきます。

その結果、30年後にはBさんの資産はAさんを大きく上回り、例えば5000万円を超えることも可能です。

「平均よりわずかに上の収入」と「平均よりわずかに下の支出」の組み合わせが、長期間の運用によって大きな成果につながるのです。

大きな資産は一夜で築かれるものではありませんが、今日から始めることで確実に未来は変わります。

この違いに気付き、実践することが小金持ちへの第一歩です。

- https://www.churio807.com/entry/littlerich

- https://info.monex.co.jp/fund/guide/emaxis-slim-usa.html

- https://itf.minkabu.jp/fund/03311187

- https://www.rakuten-sec.co.jp/web/fund/detail/?ID=JP90C000GKC6

- https://note.com/tomokoyoshimura7/n/n51ac7abb13d2

- https://manimanikun.com/news/457/

- https://www.nri.com/jp/media/column/kiuchi/20220902.html

- https://www.fsa.go.jp/policy/nisa2/invest/

- https://note.com/suganumahiroyuki/n/n0a0846510b7f

- https://news.yahoo.co.jp/articles/471e9a491133cb1630b86ea751ad7aa3bbc4ac32?page=2

- https://froggy.smbcnikko.co.jp/60718/

- https://www.rieti.go.jp/jp/papers/journal/0703/bs01.html

- https://advance.quote.nomura.co.jp/meigara/nomura2/qsearch.exe?F=users%2Fnomura%2Fdetail2&KEY1=03311187

- https://www.nihonzaitaku.co.jp/mailmag/category03/2024-11-28.html

- https://diamond.jp/zai/articles/-/293816

- https://www.fa-a.co.jp/column/increase-money/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous part~

【How to Become Super-Rich vs. How to Become Moderately Wealthy (Continued)】

Let’s compare an average person, Person A,

with Person B, who is “tuned” to become moderately wealthy.

Here’s what that looks like:

Person A has an average income

and average expenses.

On the other hand,

Person B earns slightly more than average

and spends slightly less than average.

That’s the difference.

Person B, with a small-wealth strategy, earns an extra 50,000 yen per month through a side job,

and simply reduces their living expenses by 10–20% compared to the average.

This alone allows them to save about 1,000,000 to 1,200,000 yen per year.

This is the first step toward becoming moderately wealthy.

Then, they invest that money with slightly above-average returns.

There are now many high-quality index funds, such as:

eMaxis Slim S\&P500

eMaxis Slim All Country

If you’re willing to take some risk and increase your investment ratio,

you have a good chance of outperforming the average investor.

For example, Person B keeps investing at around a 5% return.

Meanwhile, Person A simply saves 300,000 yen each year.

When we compare these two over time…

(The graph of A and B’s asset growth)

You’ll see a huge difference in the end.

The blue line represents B’s wealth.

The red line, the much smaller one, is A’s.

This much of a gap forms over 30 years.

Pretty amazing, right?

By age 54, Person B—who followed this modest wealth strategy—surpasses 50 million yen in assets.

In Japan, where people now often live to 100,

starting from zero and reaching the top 8% of wealth in your 50s

is quite an accomplishment, don’t you think?

And the difference was really just this:

Person A had average income and average expenses.

Person B had slightly higher income and below-average expenses.

That small gap leads to a huge difference in the future.

Anyone who realizes this can definitely become moderately wealthy.

Because they’re starting from zero.

You might think:

“It takes 25 years? That’s not very inspiring…”

But remember, this is just one example—

based on earning an extra 50,000 yen per month.

If you work to earn more than that,

it’s absolutely possible.

And if you can earn 50,000 yen through a side hustle,

you’ll probably be able to increase that amount over time.

That means you’ll get there faster.

And once you get the hang of managing your spending,

you can lower your expenses even more.

Again, this is just one example.

The key point is recognizing this difference.

People who tend to make excuses or deny things say things like:

“I don’t want to think about what will happen 25 years from now!”

That’s usually where they start.

But it’s not like you suddenly become rich after 25 years.

You’ll see gradual improvement along the way.

If you start today,

your life will already be better next year.

Special Thanks OpenAI and Perplexity AI, Inc