「バケツの穴をふさぐ|賢く貯めて豊かな未来を築く方法」

今日は最重要な

【貯める力】

についてお話します。

お金の成る木を増やして

豊かな人生を送るための5つの力

・貯める力

・稼ぐ力

・増やす力

・守る力

・使う力

についてお話ししてきました。

今回はこの中で最重要の

『貯める力』についてお話します。

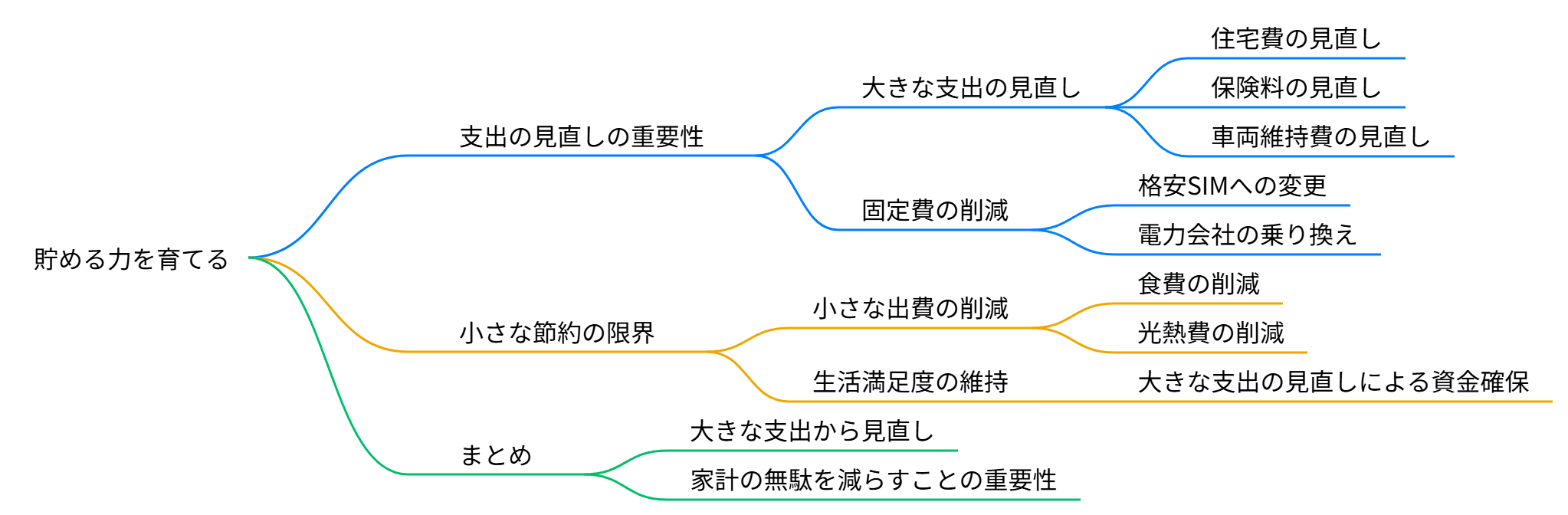

●収入が増えなくても、貯金は増やせる~あなたの未来は、“今の支出”で決まる~

『貯める力』をなぜ

最優先にするのか?

給料を増やせたら

一番いいのですが

といきなり会社に言っても

難しいじゃないですか。

出来たら苦労しない。

副業や投資を

すぐに出来ればいいのですが

・元手

・時間

・スキル

が必要です。

では

自分の判断だけですぐに出来て

効果が高いのは何か。

支出を減らす

という事です。

これは

・自分の判断ですぐに出来る

・しかも効果が高い

だから支出を減らす事を

最優先にしたい。

と言うと

と思いがちです。

お金の成る木を作っていくに当たって

お金を貯めなければならない。

そうするには

節約をしようとする。

これは

半分正解で半分間違っています。

ほとんどの人が

節約の仕方を間違えがちです。

それは何かと言うと

・食費を削る

・電気をこまめに消す

・節水

etc・・・

(例1)トイレタンクに水の入ったペットボトルを入れたりしようとしたりする。

(例2)隣町のスーパーまで特売の卵を買いに行ったりする。

これらは手間の割に効果が低い。

だからやるのは

そこではない。

やはり節約をするのであれば

大きな所から抑えないと駄目です。

では大きな所とは何でしょう?

●贅沢してないのに、お金が足りない理由~家・保険・車で人生が詰む前に~

人生の買い物の中で

高価なものTOP3は何でしょう?

イメージしてみて下さい。

1位 家

2位 保険

3位 車

この3つです。

この3つが

やはり非常に大きい買い物です。

支出の中でも一番大きい。

1位の『家』。

平均3,000万円ぐらいの家を

35年ローンで買うのが一般的です。

支払う利息が

1,300万円程度(条件による)。

これで4,300万円。

次に『保険』。

一般的に平均で

生涯2,000万円程度支払う。

そして『車』。

50年間乗り続けたら

車種によりますが

約4,000万円掛かります。

全部所有すると人間が一生ギリギリ

最低限生きていけるぐらい(約1億円)の

支出になります。

それだけ大きいんです。

実際の例を挙げると

旦那さんの給料が

30万円の家庭の場合

| 家賃(ローン) | 7.9万円 |

| 保険 | 2.5万円 |

| 車 | 3.5万円 |

| 食費 | 6万円 |

| 電気ガス水道 | 2万円 |

| 携帯電話 | 2万円 |

| 衣類 | 2万円 |

| 美容衛生 | 2万円 |

| 交際費 | 2万円 |

| 教養学費 | 2.3万円 |

各々特段贅沢していると言える

数字ではないと思います。

合計3〜40万円使っています。

だから

旦那さんの稼ぎだけでは

足りないんです。

ボーナスがある場合も

あるでしょう。

でも

生活費の補填に充てているのが

ほとんどではないでしょうか。

足りないから

奥さんもパートに出る。

支出を減らすためタバコや外食など

我慢を強いられていると思います。

子供が出来たら奥さんが

働けなくなったり

なかなか厳しくなってくる。

ですよね?

●小さな出費より“大きな漏れ”を止めよ~まずは家・保険・車・スマホ代から見直し!~

生活費のどこを削ったらいいのか?

大きいところから削る必要があります。

貯金という

水道水を貯めようとしても

家計というバケツに

穴が空いた状態では

水は一向に貯まりません。

電気代や水道代は

ごく小さな穴なんです。

ここをふさごうとすると

生活満足度が下がります。

家計バケツの

大きな穴をふさぐ必要がある。

例えば

食費を削ると言っても

ツラいじゃないですか。

衣類・化粧品・・・

我慢すればするほど

生活の質が

ドンドン寂しくなっていきます。

だから大きな所から

削っていかなければならない。

どうせ削るなら大きな所から削る。

気持ちが寂しくなる節約は

長続きしません。

だから大きな所から

削る必要があります。

・家賃

・保険

・車

あとは

・携帯料金

この項目を見直す必要があります。

●まとめ

◆支出を減らして貯める力を育てる

◆家計バケツの穴をふさぐ

◆大きな支出から見直す(家・保険・車)

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

お金を増やすためには「貯める力」が最も重要です。

収入を増やすのは簡単ではありませんが、支出を減らすことは自分の判断で今すぐ始められ、効果も高い方法です。

多くの人が節約というと食費や光熱費など小さな出費を削ろうとしがちですが、これでは効果が薄く、生活の満足度も下がってしまいます。

本当に見直すべきは「家」「保険」「車」といった大きな支出です。これらを見直すことで家計の「大きな穴」をふさぎ、無理なく貯金ができるようになります。

まずは大きな支出から見直し、家計の無駄を減らすことが「貯める力」を高める第一歩です。

Citations:

[1] https://toyokeizai.net/articles/-/862349?display=b

[2] https://diamond.jp/articles/-/283757

[3] https://toyokeizai.net/articles/-/683983?display=b

[4] https://diamond.jp/articles/-/324895

[5] https://39mag.benesse.ne.jp/money/content/?id=201587

≪≪Chat-GPTくんによる英訳≫≫

Today, Let’s Talk About the Most Important Skill:

The Power to Save

We’ve discussed the five key financial powers needed to grow your “money tree” and live a rich life:

The power to save

The power to earn

The power to grow wealth

The power to protect

The power to spend wisely

Among these, the power to save is the most crucial.

【You can grow your savings even if your income doesn’t increase】

Your future is determined by how you spend today.

Why is “the power to save” the most important?

Sure, it would be great if we could just increase our salary.

But saying:

> “Can you raise my salary by ¥○○ from next month?”

…doesn’t exactly work in the real world, does it?

If only it were that easy.

Starting a side hustle or investing might help, but you need:

Capital

Time

Skills

So, what can you do right now, on your own, that’s highly effective?

Cutting expenses.

This is:

Something you can decide and act on instantly

Something that brings quick and meaningful results

That’s why expense reduction should be the top priority.

But people often think:

> “Does that mean I just need to be frugal?”

To grow your money tree, you first need to save money.

That leads people to think about cutting costs.

But this thinking is half right, half wrong.

Most people go about saving the wrong way.

They cut:

Grocery bills

Electricity usage

Water usage

Examples:

(1) Putting a bottle of water in the toilet tank to reduce water use

(2) Driving to a far-away store just to buy discount eggs

These bring minimal results for the effort involved.

So what should you do?

You need to cut from the big categories, not the small ones.

—

【Why You Feel Broke Even Without Living Extravagantly

Before your life collapses under housing, insurance, and car costs…】

Let’s think:

What are the top 3 most expensive purchases in life?

1. A house

2. Insurance

3. A car

These three are your biggest financial commitments.

1. The House

On average, people buy a ¥30 million house with a 35-year mortgage.

They end up paying around ¥13 million in interest, bringing the total to about ¥43 million.

2. Insurance

Over a lifetime, the average person pays about ¥20 million in insurance.

3. The Car

Over 50 years, depending on the car type, you’ll likely spend around ¥40 million.

Together, these total about ¥100 million, which is roughly the cost of just scraping by over a lifetime.

—

## A Real Example

In a household where the husband earns ¥300,000/month:

| Category | Cost |

| ————— | ——- |

| Mortgage/Rent | ¥79,000 |

| Insurance | ¥25,000 |

| Car expenses | ¥35,000 |

| Food | ¥60,000 |

| Utilities | ¥20,000 |

| Phone bills | ¥20,000 |

| Clothing | ¥20,000 |

| Beauty/Hygiene | ¥20,000 |

| Social expenses | ¥20,000 |

| Education | ¥23,000 |

The total reaches around ¥300,000–¥400,000.

That’s why a single income often isn’t enough.

Even bonuses usually go toward making ends meet.

So, the wife also needs to work part-time.

And both spouses may have to give up on things like tobacco or dining out.

When a child is born, the wife might have to stop working — making things even tougher.

> “What should we do…?”

> Right?

—

【Fix the Big Leaks First

Don’t stress over the small stuff — start with your home, insurance, car, and phone bill!】

Where should you cut from?

Start with the big expenses.

Trying to fill a bucket (your savings) that has holes in it (your spending) is pointless.

Even if you turn off the lights more often or save water, these are tiny holes.

Plugging small holes won’t help much — and often lowers your quality of life.

What really matters is closing the big leaks.

Cutting food expenses, clothing, or cosmetics sounds doable —

but it hurts your lifestyle and happiness.

That kind of saving won’t last.

So if you must cut, cut from the big areas:

Housing (rent/mortgage)

Insurance

Car

Mobile phone plan

—

【Summary】

✅ Build your power to save by cutting expenses

✅ Plug the leaks in your financial “bucket”

✅ Focus on big-ticket items first — house, insurance, car, phone

Special Thanks OpenAI and Perplexity AI, Inc