「タコ足配当|投資信託の落とし穴:知られざる高コスト」

〜前回のつづき〜

●分配金の裏で、あなたの資産が減っている~喜んでる場合か?それ、返されたのは“元本”だぞ~(つづき)

(3)売る側の視点

顧客の事など

どうでもいい商品です。

なぜ仕組みが複雑なのか。

毎月分配型の

投資信託を買ってる人の中で

ちゃんと

解説できる人はいますか?

今持ってるという人で

私この商品をちゃんと

全部理解していて

・どういうもので

・どこに投資されてて

・なぜこのパーセント利回りが出てて

を

全部解説出来る人は

いますか?

多分ほとんどいないと思います。

理解してる人だったら買わない。

もしくはリスクが高い投資先や

そういうモノに投資されてる。

イマイチわからないと思うので

実例で解説したい。

人気ランキングとか

信用したらダメです。

投資商品

どれがオススメですか?

とか

ネット証券でも

人気ランキング上の方に

毎月分配型が

まだ入ってたりします。

まだ上位に入ってる商品

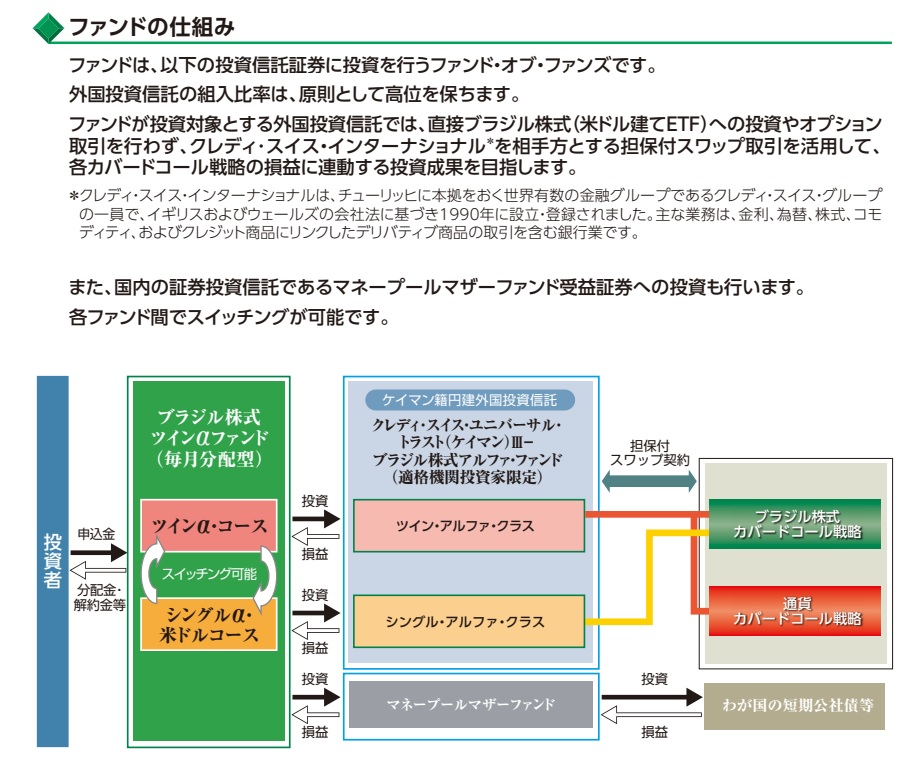

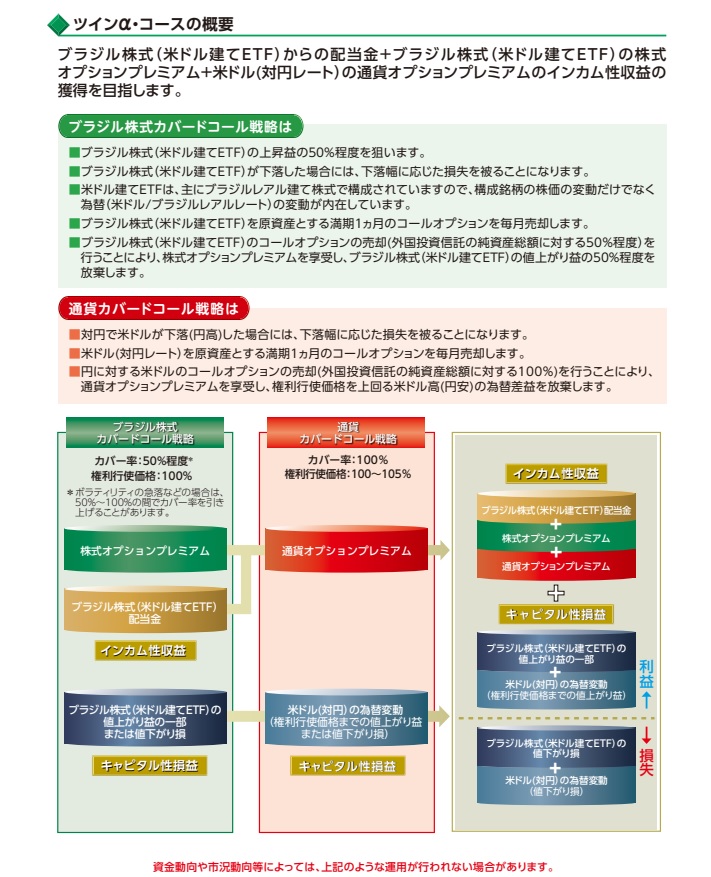

・ブラジル株式ツインαファンド(毎月分配型)ツインαコース

https://www.rakuten-sec.co.jp/web/fund/detail/?ID=JP90C000B5A8

これ今でも売れてるんですよ。

人気ランキング上の方です。

仕組みを

目論見書から取ってきました。

ファンドの仕組みが

ザーっと描いてますけど

これ誰でも

インターネットで見れますからね。

これ買ってる人とか

読んでる人の中で

わかる人います?

パッと見て

私も良くわからないです。

私自身の

勉強不足かもしれませんが。

でも普通分かりません。

要は

わざと複雑にしてるんです。

それと高い手数料。

持ってる人に聞いても

手数料いくらかわかるか聞いても

全くわかってない。

こういう商品というのは

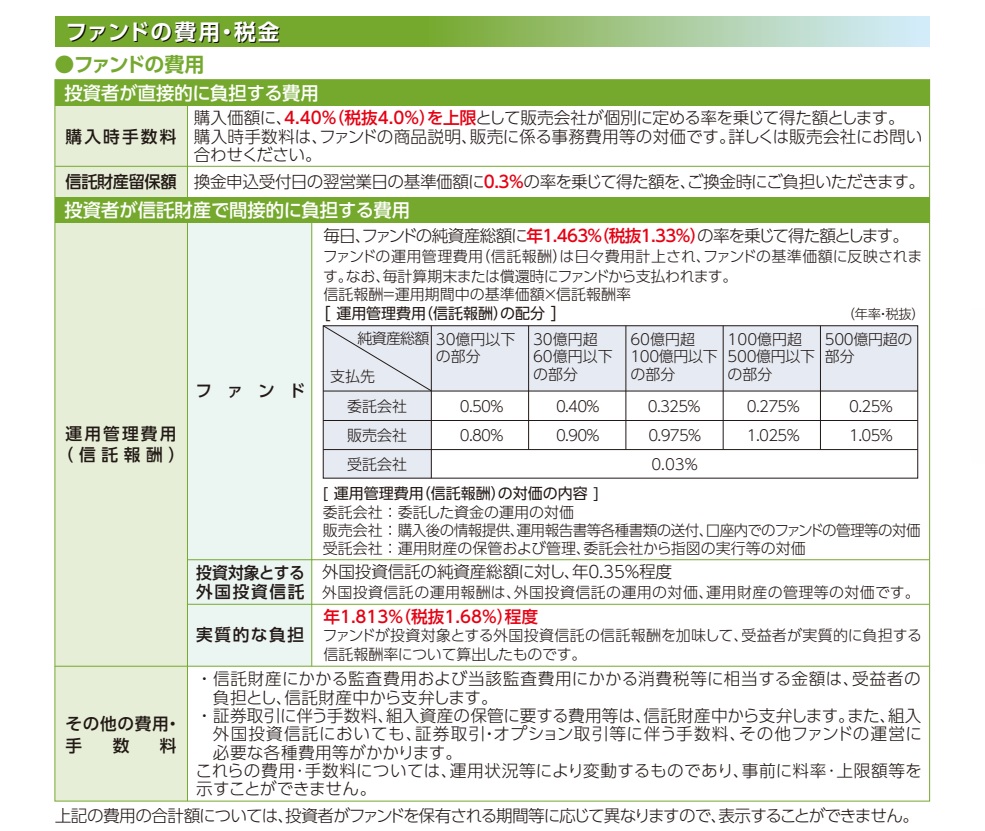

このようにちゃんと書いてあります。

購入時の手数料は4%(最大)

販売会社が決めます。

実際

ネット証券で買ったら

ここは無料だったりします。

もしくはこの運用管理。

買った時に最大4%

(購入手数料)

毎年約1.8%

(信託報酬)

辞める時に0.3%

(信託財産留保額)

かかる。

毎年2%ぐらい

いいじゃないかという気に

なるかもしれませんが

このパーセンテージは

メチャクチャ大きいです。

これが

・恐ろしい手数料

・異常に高い手数料

だという事です。

気づくようになって欲しい。

典型的なタコ足配当です。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the last time~

【Behind the Distribution, Your Assets Are Shrinking – Why Are You Happy About This? That “Payout” Was Your Principal! (continued)】

(3) From the Seller’s Perspective

They don’t care about the customer at all.

Why is the structure so complicated?

Among the people buying monthly-distribution investment trusts…

Are there any who can actually explain them properly?

I mean, people who currently own them and can say:

What exactly it is

Where it’s invested

Why it generates that percentage of yield

…and explain it all in detail?

I bet almost no one can.

If you did understand it, you wouldn’t buy it.

Or, it’s invested in high-risk assets or similar products.

I think it’s hard to picture, so let me explain with a real example.

Don’t trust popularity rankings.

When people ask, “Which investment product do you recommend?”

—Even with online brokers—

monthly-distribution types still make it into the top rankings.

One example that still ranks high:

Brazil Equity Twin Alpha Fund (Monthly Distribution) – Twin Alpha Course

[https://www.rakuten-sec.co.jp/web/fund/detail/?ID=JP90C000B5A8](https://www.rakuten-sec.co.jp/web/fund/detail/?ID=JP90C000B5A8)

Yes, this is still selling. It’s near the top of the popularity charts.

I pulled the structure diagram from the prospectus.

The fund’s mechanism is laid out in broad strokes—

and anyone can view it online.

But among the people buying or reading about it,

how many actually understand it?

At first glance, even I don’t fully get it.

Maybe that’s my own lack of study.

But normally, people won’t understand it.

The point is—they make it complicated on purpose.

And the fees are high.

Even when I ask holders if they know the fees,

they have no idea.

These products clearly state the fees:

Purchase fee: up to 4% (decided by the distributor)

If you buy through an online broker, this might be free.

Management fee: about 1.8% annually (trust fee)

Exit fee: 0.3% (trust property reserve fee) when you sell

So—up to 4% when you buy,

about 1.8% every year,

0.3% when you leave.

You might think, “Around 2% a year? That’s fine.”

But these percentages are huge.

This is—

An outrageous fee

An abnormally high fee

I want people to notice this.

It’s a textbook example of a return-of-capital dividend (“octopus eating its own legs”).

Special Thanks OpenAI and Perplexity AI, Inc