「ドンドンいい流れに|固定費を減らして賢く貯めて豊かな暮らしを!」

今日は【貯める力】

まとめ=おさらいをしていきます。

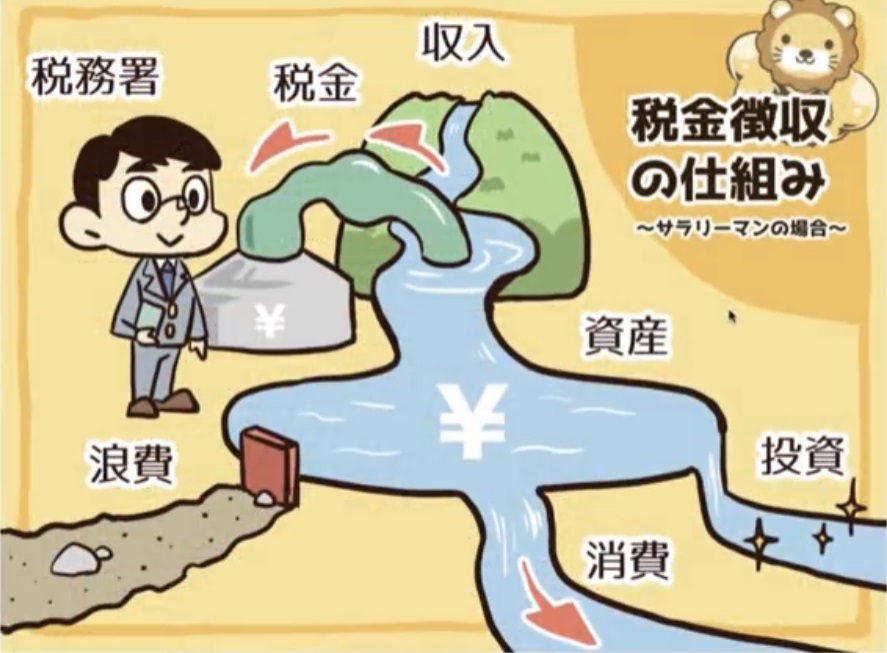

●貯めないヤツは、垂れ流してるだけ~資産の泉、今すぐ止水栓を閉めろ~

(出典:リベラルアーツ大学)

大体のサラリーマンの方の場合

『貯める力』=資産の泉を貯める

という事です。

いま通常意識せずに生きてると

泉からドンドン浪費の方に

出て行ってしまっている状態です。

まずは浪費を食い止めよう!

という事です。

ここをせき止める。

これが誰にでも当てはまるだろうし

誰にでもすぐ出来るということです。

収入の山を増やせれば一番いい。

しかしいきなりは難しい。

出来る所からやりましょう。

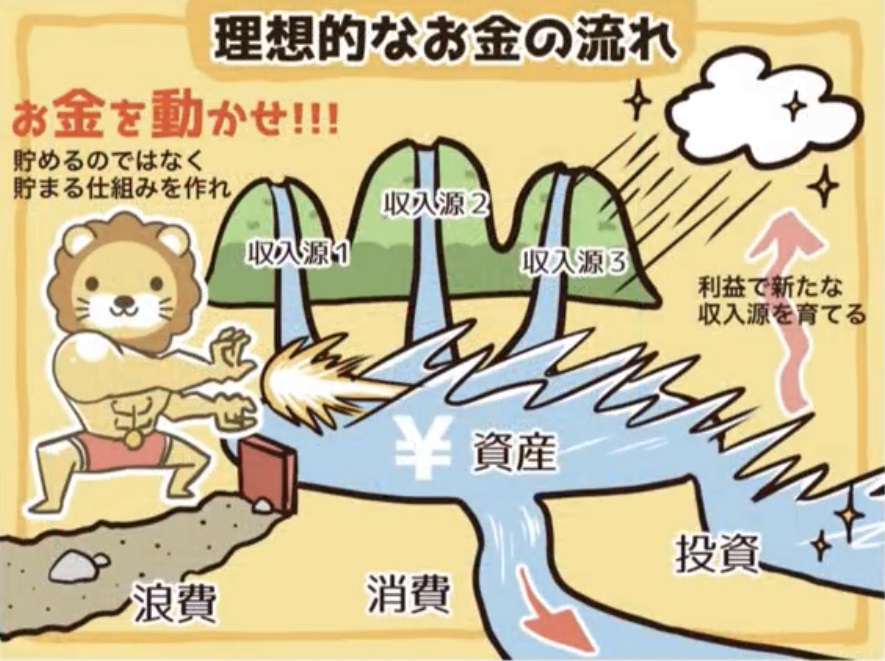

●浪費は穴、投資は種。どこに流す?~金の流れを変えろ、未来が変わる~

(出典:リベラルアーツ大学)

今後の理想的なお金の流れですが

収入源の山を沢山作る。

↓

浪費をせき止める。

↓

出来るだけ投資に流して

新たな収入源を作る。

この流れを作っていきたい。

●貯める力まとめ

(1)人生での大きな買い物

・家

・車

・保険

この3つ全部やると

お金がかなり

無くなってしまいます。

家:賃貸・中古を検討しましょう。

車:中古車で十分です。

保険:掛け捨て・自動車・火災以外は不要。

最低限だけで十分

(2)価格と価値

(出典:リベラルアーツ大学)

物の『価格』と『価値』は違います。

価格:購入する時に自分が払うただの値札

価値:色々な要因があり人によって違う

・精神的な部分

・安心感

・満足感

・売却時の価値

どの部分の価値があるのか

物を買う時に自分にとって

どこの部分に価値があるのか

ちゃんと見極めて

買いましょう。

資産を買ってるつもりが

負債を買ってるような状態に

ならないように。

(3)固定費を下げる

給料を上げるより

固定費を下げるほうが

効率が良いことが多いです。

普通は

給料を上げるのは難しく

すぐには上がらない。

でも給料を上げるよりも

固定費を下げるほうが

簡単であることが多い。

固定費を1万円下げるのは

給料で1万円上げるのと

同義ではないです。

給料は税金が引かれる。

手取り1万円を得ようとすると

1万3千円ぐらい給料を

上げなければいけません。

だから

固定費を下げる方が

圧倒的に効率的がいい。

(出典:リベラルアーツ大学)

まずは流出する水を

食い止めることから始める。

ジャブジャブ

水が流れ出ている状態なのに

一生懸命水だけ沢山入れても

水は溜まりません。

固定費を下げるというのは

(出典:リベラルアーツ大学)

精神安定剤にもなる。

コストが

沢山掛かっている状態というのは

やはり苦しい。

のマインドになってしまいます。

ただし

極端に生活の質を落とす節約は

長続きしません。

●固定費は“見直せる給料”~稼げないなら削れ~

固定費を見直してどうなったか?

賛否両論あるとは思いますが

実際にずっと

お話ししてきた事を実践して

固定費を見直してくれたら

どうなっていたか見比べてみたい。

手取り25万円の家庭の

平均的な支出を出してみた。

(→#4 「貯める力」が最重要。参照)

| 家賃(ローン) | 7.9万円 |

| 保険 | 2.5万円 |

| 車 | 3.5万円 |

| 食費 | 6万円 |

| 電気ガス水道 | 2万円 |

| 携帯電話 | 2万円 |

| 衣類 | 2万円 |

| 美容衛生 | 2万円 |

| 交際費 | 2万円 |

| 教養学費 | 2.3万円 |

| 計 | 32.2万円 |

普通の生活水準といわれる

生活をしていても

合計30〜40万円使う。

だからどこの家でも

お金が足りない。

だから

奥さんもパートに出たり

じゃあ

交際費を削ろうとか

色んな事のどこかを

すごく我慢してる人が多い。

もしくは独身時代の貯金を

少しずつ使っている人など

色々いると思います。

↓改善案

| 家賃 | 7万円 |

| 保険 | 0.5万円 |

| 交通費 | 1万円 |

| 食費 | 6万円 |

| 電気ガス水道 | 2万円 |

| 携帯電話 | 0.5万円 |

| 衣類 | 2万円 |

| 美容衛生 | 2万円 |

| 交際費 | 2万円 |

| 教養学費 | 2万円 |

| 計 | 25万円 |

そうすると家は買わずに

賃貸でいいいじゃないか。

保険というのが

これだけ差額が出る。

上と下で見比べるのが

難しいかもしれませんが

・保険はひとつだけ

・車は持たない→手放す

・中古の車にする

・携帯を格安SIMに変える

これで大分変わります。

もちろん

田舎住まいで

車が手放せないとか

色々な事情がある。

それはそれで構いません。

それは必要に応じて

各自で判断してもらっていいです。

田舎であればその分

・家賃が安かったり

・生活費が安かったり

そういう所もあるので

その分プラスマイナスゼロに

なってくるかと思います。

その辺は

各自の考えで構わないと思います。

ここをもし皮算用ですけど

全部見直せたというだけで

支出が

30〜40万円使ってたのが

合計25万円になった。

かなり下がります。

給料にしたら

7〜10万円

仮に

10万円固定費の削減ができたとすると

13万円給料が上がったのと同じです。

そのぐらい

固定費削減というのは

効果があります。

無理なく我慢できる

レベルじゃないかと思います。

こういうのをやり出すと

意識が変わってくるので

無理なくやめていけるのではないかと。

その辺は

各自が判断していただければ。

今日必要だったものも

1年後不要になってるものも

有ると思うので

定期的に見直してください。

●結局、お金が“お金”を産む~だから、まずは貯めろ~

お金を産むというのは

結局お金なんですよ。

これについては

今後お話ししていきます。

お金が全てではありませんが

やはり

・消費に使うにせよ

・資産に使うにせよ

お金が原資というのは

変わりないです。

だからまずは

ある程度貯めるのが大事です。

・心の豊かさに使うにせよ

・投資に回すにせよ

お金はある程度必要です。

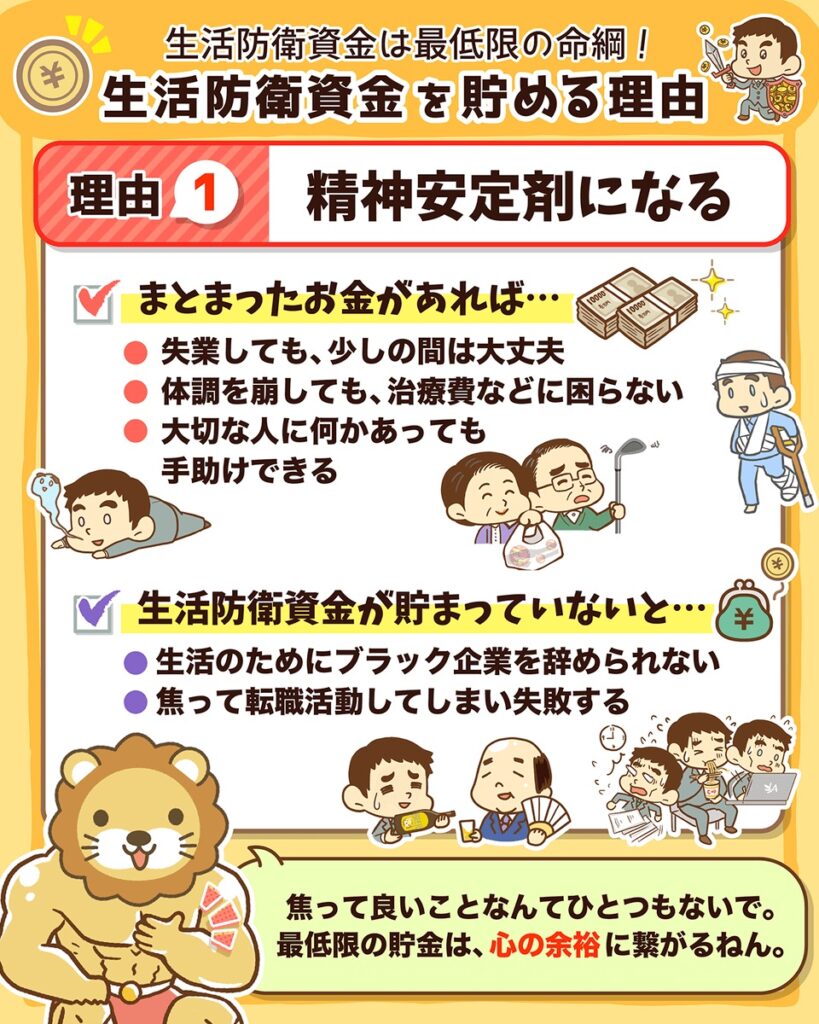

最低限貯めたら

医療保険も不要になる。

いざという時

本当に最低限の医療費を

払うお金も無いから

どうしても医療保険に

入らないといけないとか

どうしても今車が壊れたら

修理費も払えないから

車両保険も入らないといけない

だからそれより

最低限ちゃんと

お金を貯めましょう。

そうすると余計な金利も

払わなくて済みます。

車も一緒です。

カーローンじゃなくても済むし

カーローンは金利が高い。

気持ちに余裕もできる。

いつでも買えるとなれば

何かあった時にも安心ですし

不思議なことに

今まで欲しかったものでも

そんなにでもなくなる。

そんな事も出てきます。

ドンドン

いい流れになっていきます。

●“貯める力”がない奴は、稼いでも溺れる~家計を制す者だけが、金を扱える~

貯める力が無いと

稼いでもお金を失ってしまう。

自分の家計という所から

ちゃんと今の現在の収入の中で

ちゃんと

見直す力というのが

すごく大事です。

今後大きく

お金を稼いだりとか

たくさんのお金を

取り扱っていく中でも

すごく大事な力になっていくので

ここをちゃんと

やはりできるようになって欲しい。

●まとめ

これが

今までずっと『貯める力』として

お話ししてきた内容です。

色々お疲れ様でした。

まだまだ

始まりなので

これから

・投資=お金を増やす

・稼ぐ

とか

いろんな勉強を

たくさんしていきたいと思います。

また次回からも

一緒に勉強していきましょう。

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

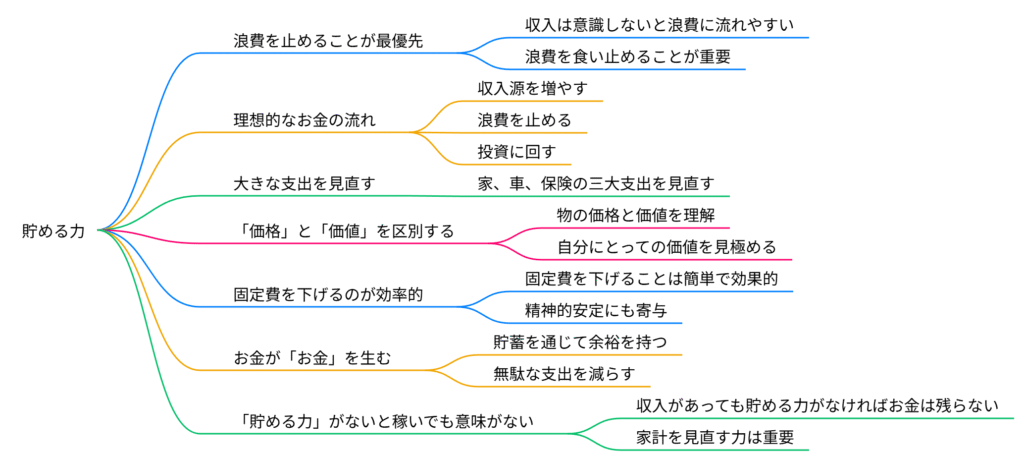

「貯める力」とは、収入を無駄に浪費せず、しっかりと資産を蓄える力のことです。

まずは生活の中で流れ出ている「浪費」を止めることが最優先です。

特に家・車・保険などの大きな支出は見直し、必要以上にお金を使わない工夫が大切です。

また、物の「価格」と自分にとっての「価値」をしっかり見極めて購入することも重要です。

給料を上げるよりも、固定費を下げる方が簡単で効果的なので、通信費や保険料などを見直しましょう。

貯めたお金は将来の投資や安心につながります。

どれだけ稼いでも貯める力がなければお金は残りません。

まずは支出を見直し、無理のない範囲で「貯める力」を身につけましょう。

Citations:

[1] https://fp-bu.com/saving-point/

[2] https://diamond.jp/articles/-/358464

[3] https://d21.co.jp/book/detail/978-4-7993-2907-8

[4] https://www.nagano-rokin.co.jp/money/detail/59

[5] https://miraii.jp/financial-7

≪≪Chat-GPTくんによる英訳≫≫

Today’s Topic: “The Power to Save”

Let’s summarize and review what we’ve covered so far.

—

【If You Don’t Save, You’re Just Letting It All Flow Out – Stop the Leak in Your Asset Fountain Immediately】

(Source: Liberal Arts University)

For most salaried workers,

“The power to save” = Accumulating wealth in your financial fountain.

If you go through life without being conscious of your money,

you’ll find that wealth is constantly leaking out through wasteful spending.

So first, we must stop the leaks.

This is something that applies to everyone,

and anyone can start doing it immediately.

Ideally, you’d increase your income streams.

But that’s not easy to do right away.

So let’s begin with what we can do.

—

【Wasteful Spending is a Hole, Investment is a Seed – Where Will You Pour Your Money? Change the Flow, Change Your Future】

(Source: Liberal Arts University)

The ideal future flow of money looks like this:

1. Build multiple income streams

2. Plug the leaks of wasteful spending

3. Funnel as much as possible into investments

4. Generate new income streams

This is the cycle we want to create.

—

Summary: The Power to Save

—

(1) The Three Major Expenses in Life

Housing

Cars

Insurance

If you commit to all three,

you’ll see your money disappear fast.

Housing: Consider renting or buying used.

Cars: A used car is more than enough.

Insurance: Other than term life, car, and fire insurance – most aren’t necessary.

Stick to the minimum.

—

(2) Price vs. Value

(Source: Liberal Arts University)

The price of an item is different from its value.

Price: The number on the tag, what you pay upfront

Value: Depends on individual perception and many factors, including:

Emotional satisfaction

Peace of mind

Resale value

Personal fulfillment

Know where the value lies for you personally before buying.

Don’t mistake liabilities for assets.

—

(3) Lower Fixed Costs

Reducing fixed costs is often more efficient than increasing income.

It’s hard to get a raise.

And even when you do, it takes time.

But cutting fixed costs is usually easier.

Also, reducing your expenses by ¥10,000 is not the same as earning ¥10,000 more in salary.

Because salary gets taxed –

to take home an extra ¥10,000,

you might need to earn around ¥13,000 more.

So cutting costs is way more efficient.

(Source: Liberal Arts University)

Start by stopping the outflow.

You could pour in more and more water (income),

but if there’s a hole in the bucket (expenses), it’ll never fill up.

Cutting fixed costs also helps reduce mental stress.

Having high expenses feels suffocating and leads to a mindset of:

> “I have to earn more!”

But severe lifestyle cutbacks aren’t sustainable either.

—

【Fixed Costs = Adjustable Salary – If You Can’t Earn More, Cut More】

So what happens when you actually review and reduce your fixed costs?

Opinions may vary, but let’s compare what happens when someone truly implements this advice.

Here’s a typical breakdown for a household with ¥250,000 in take-home pay:

Before cost-cutting:

Rent (loan): ¥79,000

Insurance: ¥25,000

Car: ¥35,000

Food: ¥60,000

Utilities: ¥20,000

Phone: ¥20,000

Clothing: ¥20,000

Beauty/Hygiene: ¥20,000

Socializing: ¥20,000

Education: ¥23,000

Total: ¥322,000

> (Overspending by ¥72,000)

Even with a “normal” lifestyle, families easily spend ¥300,000–¥400,000.

So they end up:

Sending the spouse to work part-time

Cutting back on social life

Dipping into savings from their single days

—

After cost-cutting:

Rent: ¥70,000

Insurance: ¥5,000

Transportation: ¥10,000

Food: ¥60,000

Utilities: ¥20,000

Phone: ¥5,000

Clothing: ¥20,000

Beauty/Hygiene: ¥20,000

Socializing: ¥20,000

Education: ¥20,000

Total: ¥250,000

This shows:

You don’t have to buy a house – rent is fine.

Insurance costs can drop significantly.

Just one policy is enough.

Consider selling your car or switching to a used one.

Switch to a budget SIM for your phone.

Of course, if you live in the countryside and need a car, that’s understandable.

But rural life often comes with:

Cheaper rent

Lower living costs

So it evens out.

If you manage to cut fixed costs by ¥100,000,

that’s like getting a ¥130,000 raise (after taxes).

That’s how powerful cost reduction can be.

It’s realistic and manageable for most.

And once you start, your mindset changes.

You stop spending needlessly.

Remember, something you need today

might not be needed a year from now.

So review your expenses regularly.

—

【In the End, Money Produces More Money – So Save First】

The truth is, money creates more money.

This is something we’ll dive deeper into in the future.

Money isn’t everything, but still—

Whether for:

Spending

Investing

You need money as a base.

So first, build your savings.

Whether it’s for mental peace or for investments,

you’ll need a certain amount.

Once you have savings, you may not even need insurance.

If you can afford basic medical costs in emergencies,

you don’t need to rely on medical insurance.

If your car breaks down and you can pay for repairs,

you don’t need expensive coverage.

Save first – and you’ll avoid:

Paying interest

Taking out loans

Emotional stress

You’ll gain peace of mind knowing

you can buy something if needed.

And funny enough—

things you once desperately wanted

may no longer seem necessary.

It all begins to flow positively from there.

—

【Without the Power to Save, Even High Earners Will Drown – Only Those Who Control Their Household Finances Can Handle Wealth】

If you lack the power to save,

you’ll lose your money no matter how much you earn.

You need to regularly review your household finances

and manage your income wisely.

Even as you begin to earn more and handle greater sums,

this ability remains vital.

So please develop this skill properly.

—

【Final Summary】

This concludes the discussion on

“The Power to Save.”

Great job sticking through it all!

But this is just the beginning.

From here on:

Investing = Growing money

Earning more

…will become our next learning goals.

Let’s keep studying together in the next session!

Special Thanks OpenAI and Perplexity AI, Inc