「地獄の始まり|カードローンの呪縛を解き、負担を減らし、未来を取り戻そう!」

今日は【貯める力】

リボ払いとカードローンからの脱出手順

をお話しします。

●気軽に借りた代償が、一生残るレッスン料~リボは“リボルバー” 撃たれるのはあなたの人生~

前回

リボ払いとカードローンには

本当に注意して下さいという

お話しをしました。

もう既に使ってしまってる人

についてお話ししていきます。

現にリボやカードローンを

使ってしまっている人は

とにかくすぐに頑張って

返済して下さい。

じゃないと

本当にシンドくなります。

地獄の始まりです。

これで苦しんでる人が

いっぱいいます。

借りてしまってるのであれば

とにかく早く返済していく。

次にこれ以上使わないというのが

大事です。

●“分割のつもり”が、“搾取の地獄”~何も得ずに、金利だけが太っていく~

必ず自分の手数料(金利)の

現状を確認して下さい。

大体の人が15%です。

これが2〜3%だったら

まだいいんですけど

まずそんなことは無い。

リボ払いを使っていて

せいぜいいい所で12〜3%

という所だと思います。

ほとんどが

15%になってると思います。

例)

100万円を借りてるとします。

100万円をもしリボ払いで

まだ支払いが残っている場合

年間15万円の

手数料が掛かります。

年間15万円というのは

毎月1万2千円。

1万2千円を毎月

金利(手数料)だけで

払ってるんですよ。

毎月1万2千円給料を

上げようとすると

非常に大変です。

手取りで

1万2千円上げなければならない。

いつも言うように

税金が引かれるので

1万5千円ぐらい

給料を上げなければならない。

だから金利というのは

支払っていくのが

凄く大変です。

なので何とかしたい。

これを返すんだけど

・そんなことわかってる!

・すぐ返済できるものならしたい

・それが出来ないから困ってるんだ!

という人が結構いると思います。

●どんなに苦しくても“知らないまま払う”だけはやめろ~交渉しろ、下げろ、取り戻せ~

具体的に返す方法を

見てみましょう。

(1)親から借りる

優先度が一番高い。

お金的には一番いい。

気持ち的には言いにくいとか

色々あると思います。

しかし実際

親や親族に話をして借りて

毎月返していくというのが

本当は一番やりやすい。

兄弟でもいい。

金利(=手数料)で

毎月1万2千円も払っている訳です。

だから

ちゃんと返す意思が有るのであれば

親に話をして借りて

ちゃんと毎月返していく。

もしも同じ金利を払うにしても

クレジット会社に払うより

自分の親に払う方が

いいと思いませんか?

クレジット会社に1万2千円以上

毎月取られている訳です。

100万円の人で

1万2千円です。

中には200万円の人も

いるかもしれない。

だからそこから考えたら

クレジット会社に払うよりも

親から借りてでも

毎月返していくという方が

トータルでいい。

でも

どうしてもそれも出来ない。

そういうことも話せない。

親も大変な状況だし

頼れる人もいない。

そういう人もいるので

そういう人の場合は

自力で返していかないと

仕方ないです。

(2)カードの手数料を下げる

手数料15%というのが

非常に高いのでここを下げたい。

現在15%の手数料であれば

ちょっとは下がる余地があります。

限度額と手数料を確認する。

今の自分の限度額によるんです。

おおよその目安ですが

・100万円以下であれば15%

・100〜200万円であれば12%

・200〜300万円であれば10%

・300万円以上 5〜6%

これは

不思議に思うかもしれませんが

沢山借りる枠が有る人ほど

手数料は安い。

これはクレジット会社の立場

=お金を貸す方の立場にに立ってみると

分かるのですが

・限度額100万円の人3人に貸す

・300万円一括ドン!と貸す

手間はどっちが少ないか?

という事です。

『貸し倒れ』といって

返してくれなくなるリスクとか

色々ありますが

手間からすると

沢山借りてくれる人の方が

貸す側からすると嬉しい。

だから沢山借りてくれる人ほど

手数料というのは基本的には安くなる。

特に

限度額が高い人というのは

ある程度の実績がないと

いきなり高い金額を

安い金利では借りられない。

(それでも高いですが)

ほとんどの人が

うまくいって

10%ぐらいでしょうか。

15%の人が10%ぐらいになる

確率は十分あります。

やはりそこは頑張りたい。

(3)複数社から借りてるならまとめる

A社から150万円

B社から70万円

借りてるのであればまとめてC社

もしくは片方

AもしくはB社にまとめてもいい。

一社にまとめる。

すると金利が下がりやすい。

200万円借りてる人が

15→10%になれば

私の友達が

全く同じ状況だったのですが

まとめて200万円にした。

すると交渉したら

15→10%になって

年間10万円得することになった。

金利5%というのは

凄く大きい。

投資で

5%の利回りを出そうとすると

結構大変です。

これだけで支払い手数料が

月々8,000円減ったそうです。

そうすると給料にしたら

1万円くらい給料が上がったのと

同じ事です。

最初は簡単には

下げてくれないかもしれませんが

何社にも見積もりを取って

返済していくだけで

手数料が下がって

給料が1万円上がるのと

同じことになります。

どこに

借り換えればいいのかというと

答えだけ言うと

銀行系のカードローンです。

大手ですね。

10%ぐらいには

なる可能性がある。

借り換えローンというのが

設定してあって

・三井住友カード おまとめローン premium/plus

・三菱UFJバンクイック

・みずほ銀行おまとめローン

・auじぶん銀行カードローン

等各社取り合いです。

ただし

審査に落ちてしまうこともあります。

自分が口座を持っている銀行だと

借りやすい等いろいろあるので

試してみてはいかがでしょうか。

ただやはり理想は

親兄弟から借りて返す

というのが本当はいいです。

カードローンや

リボ払いをしている人というのは

まずは投資の前に頑張って返しましょう。

●固定費は“沈黙のドロボウ”~何も変えずに、“自己破産”に逃げるな~

そして固定費を抑えて下さい。

今まで

管理してこなかった所も

あると思うので

これを機会に

・金利

・無駄な保険

・携帯

・車

全部見直して

固定費を抑えて下さい。

それから

副業をして稼ぐ金額を増やす

のも一つです。

今後その手法についても

お話ししていきます。

該当する人は

結構耳が痛いのではないでしょうか?

それでも限界だという人には

自己破産という手があります。

ただこれは最終手段なので

まずは現実的な返済から始めていく。

それからです。

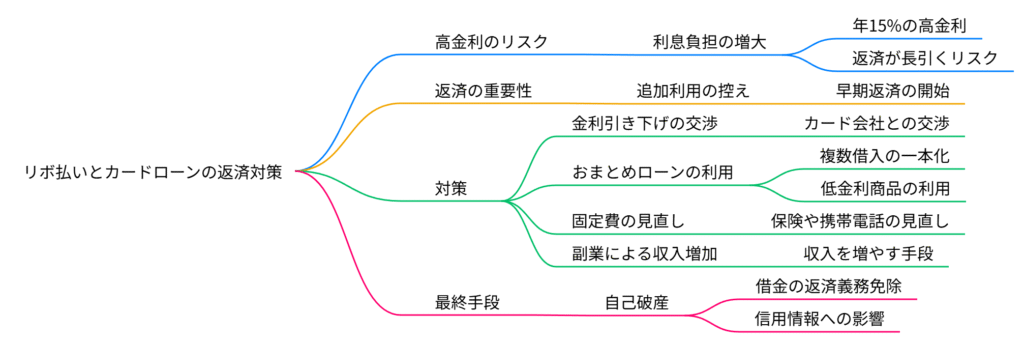

●まとめ

◆すぐに返済して!

→次にこれ以上使わない

◆現状確認する

→ほとんどが15%

◆具体的に返す方法

→(1)親から借りる

(2)カードの手数料を下げる

(3)複数社から借りてるならまとめる

◆どこに借り換えればいいのか?

→銀行系カードローン

◆まずは頑張って返す

→固定費を抑える

副業する

◆限界だという人

→自己破産

(最終手段なのでまずは現実的な返済から始めていく)

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

リボ払いやカードローンは高金利(多くは年15%)で、返済が遅れるほど負担が大きくなります。

すでに利用している場合は、まず追加利用をやめ、できるだけ早く返済を始めましょう。

具体的な方法としては、親や親族から借りて返済するのが一番負担が少なくおすすめです。

難しい場合は、カード会社に交渉して金利を下げたり、複数社から借りている場合は「おまとめローン」で一本化し、銀行系カードローンなど低金利への借り換えを検討しましょう。

また、保険や携帯、車などの固定費も見直し、場合によっては副業で収入を増やすことも大切です。

どうしても返済が難しい場合は、自己破産も最終手段として考えましょう。

- https://www.jcb.co.jp/loancard/special/ribo_payment.html

- https://www.bk.mufg.jp/column/loan/0002.html

- https://www.mizuhobank.co.jp/loan_card/article/no_50/index.html

- https://www.j-credit.or.jp/customer/basis/revolving.html

- https://www.82bank.co.jp/column-card-loan/return.html

- https://www.tokyostarbank.co.jp/feature/education/borrow/20230807_2.html

- https://lakealsa.com/repayment/selection/

- https://www.resonabank.co.jp/kojin/cardloan/payment.html

- https://loan.docomo.ne.jp/article/revolving_repayment_card_loan/

- https://www.smbc.co.jp/kojin/cardloan/beginners/column40.html

≪≪Chat-GPTくんによる英訳≫≫

Today’s Topic: “The Power of Saving”

How to Escape from Revolving Payments and Card Loans

—

【The Price of Easy Borrowing Is a Lifelong Lesson~ Revolving credit is like a revolver—what gets shot is your life 】

Last time, I talked about how important it is to be extremely careful with revolving payments and card loans.

This time, I’ll speak to those who have already used them.

If you’ve already used revolving payments or card loans, then the most important thing is to make a serious effort to repay them right away.

If you don’t, things will get really painful.

It’s the beginning of a financial nightmare.

Many people are suffering because of this.

So if you’ve already borrowed money, do whatever it takes to repay it quickly.

Next, make sure you never use them again. That’s critical.

—

【What You Thought Was Installment” Turns Into a “Hell of Exploitation~ You gain nothing while only the interest gets fat】

You must check what interest (fees) you are currently paying.

For most people, it’s around 15%.

If it were only 2–3%, that would be manageable—but that’s almost never the case.

Even in the best cases, revolving payment rates are about 12–13%.

But for most people, it’s 15%.

Example:

Say you borrowed 1 million yen.

If you’re still paying it off through revolving payments, you’re paying 150,000 yen per year in interest alone.

That’s 12,000 yen every month—just in interest.

Trying to increase your monthly salary by 12,000 yen is extremely difficult.

Because of taxes, you’d actually have to increase your gross salary by 15,000 yen or more just to get 12,000 yen in your hands.

That’s how burdensome interest payments are.

So you want to do something about it.

But many people will say:

“I know that already!”

“I’d pay it off if I could!”

“I can’t do that, and that’s exactly why I’m struggling!”

I get it.

—

【No Matter How Tough It Is, Stop “Blindly Paying Without Knowing~ Negotiate, Lower the Rate, Take Back Control 】

So let’s talk about concrete repayment strategies:

—

(1) Borrow from Your Parents

This is the highest priority.

Financially, this is the best option.

It may be awkward emotionally, but realistically, borrowing from parents or relatives and repaying them monthly is the easiest and cheapest way.

Even siblings are fine.

You’re currently paying 12,000 yen per month in interest.

So if you’re serious about repaying the debt, talk to your parents, borrow the money, and repay them monthly.

Even if you pay the same interest, wouldn’t you rather pay it to your parents than to a credit card company?

Some people owe 2 million yen or more, which means paying 24,000 yen/month in interest.

So from a total cost perspective, borrowing from family is far better than staying with a credit company.

But I understand—

Some people can’t do that.

They may not be able to talk to their parents, or their parents may also be financially tight.

In that case, you’ll need to repay on your own.

—

(2) Lower Your Credit Card Interest Rate

If you’re paying 15%, that’s way too high.

There might be room to negotiate.

Check your credit limit and your current interest rate.

Here’s a general guide:

Under 1 million yen → \~15%

1–2 million yen → \~12%

2–3 million yen → \~10%

Over 3 million yen → \~5–6%

This may seem strange, but the more you’re able to borrow, the lower the interest rate becomes.

From the lender’s perspective, it’s less hassle to lend 3 million yen to one person than 1 million yen each to three people.

Despite the risk of default, it’s less work to manage one big borrower.

So people with higher credit limits often get lower interest rates.

Of course, this still isn’t “low”—but getting from 15% down to 10% is quite realistic.

—

(3) Consolidate Multiple Loans

If you’ve borrowed:

1.5 million yen from Company A

700,000 yen from Company B

Then consolidate the debt into Company C—or even into just one of the existing companies.

Merging into a single loan often reduces the interest rate.

For instance, my friend had the exact situation:

They consolidated 2 million yen into one loan and negotiated the rate from 15% → 10%.

That saved them 100,000 yen per year.

A 5% reduction in interest is a huge win.

To earn a 5% return on investment is not easy—but saving it through refinancing is.

In their case, monthly interest payments dropped by 8,000 yen—

That’s like getting a 10,000 yen raise without changing jobs.

You might not succeed on your first try, but getting multiple estimates can lower your rate.

Where should you refinance?

The answer: Bank-affiliated card loans.

For example:

Sumitomo Mitsui “Omatome Loan Premium/Plus”

Mitsubishi UFJ “Banquic”

Mizuho Bank “Debt Consolidation Loan”

au Jibun Bank Card Loan

These banks compete for customers.

That said, approval isn’t guaranteed—

But if you already have a bank account with them, it may increase your chances.

Still, ideally, borrowing from family is the best route.

—

【Fixed Costs: “The Silent Thief~ Don’t default just because you won’t change anything ~】

Next, reduce your fixed costs.

You may not have been managing these before, but now is the time.

Review everything:

Interest rates

Unnecessary insurance policies

Phone bills

Car-related costs

Cutting these will help free up cash.

Then, consider side hustles or additional income streams.

I’ll talk more about specific side jobs in future posts.

Some of you may find this tough to hear—but it’s necessary.

For those at their absolute limit, bankruptcy is an option.

But that is a last resort.

Start with realistic repayment plans first.

—

【Summary】

◆ Start repayment ASAP

→ Then stop using loans completely.

◆ Check your current interest rates

→ Most are around 15%.

◆ Repayment methods:

→ (1) Borrow from parents

→ (2) Lower your credit card interest

→ (3) Consolidate multiple loans

◆ Where to refinance:

→ Bank-affiliated card loans

◆ Start by repaying what you can

→ Cut fixed costs

→ Earn extra through side jobs

◆ If you’ve hit the wall:

→ Bankruptcy is an option (but only as a last resort)

Special Thanks OpenAI and Perplexity AI, Inc