管理人オススメコンテンツはこちら

「ローンの罠から脱出!賢い選択で未来に繋ぐ節約術」

今日は【貯める力】

金利や手数料を抑えて

人生で1,200万円以上得する方法

についてお話しします。

●金利は静かに、あなたの一生を食い尽くす~ローンを組むたび、人生の自由が削れていく~

今日の相談はこちら。

「ガンガンローンを組んで

暮らしていった場合

一生でどれぐらい金利・手数料を

支払うことになるのでしょうか?」

とのこと。

平均的な年収の人が可能な範囲で

ローンを組んで生活していくと

一生で

1,200万円以上の金利・手数料を

支払う事になります。

住宅ローンを組まずに

保険を必要最小限にして

・車

・奨学金

・生活費

などでローンを使わなければ

1,200万円以上の節約になります。

でも実際には

もっと大きい節約になるんですよね。

そこも含めてお話ししていきます。

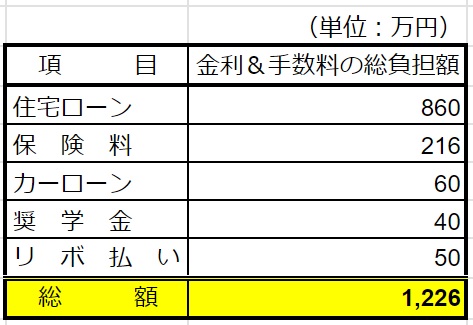

●人生で支払う金利・手数料

高い金利・手数料がかかる商品で

良く利用されるのは・・・

(1)住宅ローン

(2)生命保険・医療保険

(3)カーローン

(4)教育ローン

(5)リボ払い

この5つです。

この5つが本当に金利・手数料が高い。

全部をフル活用すると約30年で

このぐらいの金利手数料がかかります。

住宅ローンの場合だったら

860万円ぐらい金利がかかり

保険料であれば

200万円以上の手数料がかかって

カーローンも60万円程度

奨学金も40万円程度

リボ払いが50万円

とそんな感じになってきます。

●内訳を詳しく見てみよう

シミュレーションの前提条件として

・性別 男性

・年収 500万円

・生涯賃金 2.5億円

・手取り 390万円(年間)

25万円(月間)

・賞与 2ヶ月✖️年2回

今回のシミュレーションでは

(1)住宅ローン

(2)生命保険・医療保険

(3)カーローン

(4)教育ローン

(5)リボ払い

全部込みで

月に16万円の返済している状態とする。

手取り25万円で16万円返済に回すと

9万円の手残りとなる。

十分暮らしていける

現実的な数字ではないでしようか?

比較的一般的な家庭の条件で出してみます。

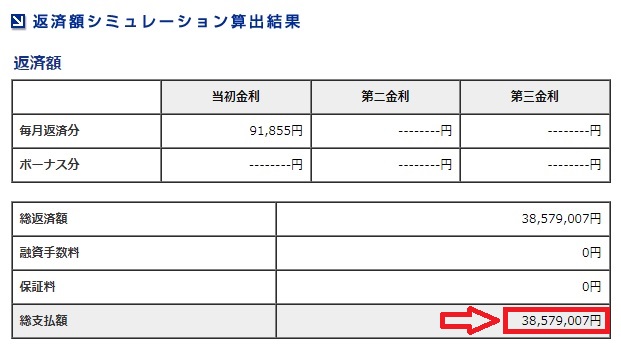

(1)住宅ローン

借入総額 3000万円

借入金利 1.5%(固定金利)

返済期間 35年

だとすると・・・

(出典:https://loan.mamoris.jp/repayment.asp)

返済総額は約3,860万円になるんですね。

借入総額が3,000万円に対して

返済総額が3860万円になるという事は

利息は860万円払うという事になります。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

ローンや保険の金利・手数料は、気付かないうちに一生涯で1,200万円以上もの大きな出費になります。

例えば年収500万円の一般的な家庭を想定すると、住宅ローン・生命保険・カーローン・教育ローン・リボ払いなどを利用した場合、返済により毎月16万円を支出し、30〜35年で1,200万円超の利息や手数料を払うことになります。

特に住宅ローン3,000万円を金利1.5%で35年借りると、利息だけで860万円。

保険の手数料は200万円超、カーローンや奨学金、リボ払いも合わせると数百万円になります。

しかし、住宅ローンを組まず、保険も必要最低限にし、安易にローンを使わなければ、これらの支出自体を抑えることができ、生涯で1,200万円以上節約できるのです。

資産形成の第一歩は「増やす」前に「金利・手数料を払わないこと」。借金や過剰な保険を見直すだけで、確実に人生の自由度と貯蓄力が高まります。

- https://www.familyls.jp/column/loan/housing-loan-calculation/

- https://mponline.sbi-moneyplaza.co.jp/housingloan/articles/20200903risokukeisan.html

- https://www.smbc.co.jp/kojin/jutaku_loan/column/kinri_calculation/

- https://www.gunmabank.co.jp/kojin/kariru/koza/koza2.html

- https://www.flat35.com/simulation/simu_01.html

- https://www.bk.mufg.jp/column/loan/0013.html

- https://www.eloan.co.jp/home/sim/payment/easy/

- https://www.idea-h.net/blog/first-home-loan-calculation-guide/

- https://www5d.biglobe.ne.jp/Jusl/Keisanki/JTSL/Loan.html

≪≪Chat-GPTくんによる英訳≫≫

Today’s topic is “The Power of Saving”

How to save more than 12 million yen in your lifetime

by cutting down on interest and fees.

—

Interest quietly eats away at your entire life

— Every time you take out a loan, a piece of your freedom disappears —

Here’s today’s consultation:

“If I keep taking out loans one after another to live my life,

how much interest and fees will I end up paying in total over my lifetime?”

The answer:

If someone with an average income takes out loans within a realistic range and lives that way,

they will end up paying over 12 million yen in interest and fees during their lifetime.

But if you avoid a housing loan, keep insurance to the bare minimum,

and don’t use loans for things like:

Cars

Student loans

Living expenses

then you can save more than 12 million yen.

In reality, the savings could be even greater.

Let’s take a closer look.

—

### Interest and fees you pay in a lifetime

The financial products that often carry high interest and fees are:

1. Housing loans

2. Life insurance / medical insurance

3. Car loans

4. Education loans

5. Revolving credit (revolving payments)

These five categories are the real cost drivers.

If you fully utilize all of them, in about 30 years you’ll pay this much in interest and fees:

Housing loan interest: about 8.6 million yen

Insurance commissions: over 2 million yen

Car loans: around 600,000 yen

Student loans: around 400,000 yen

Revolving credit: around 500,000 yen

That’s the rough breakdown.

—

Let’s look at the details

Simulation assumptions:

Gender: Male

Annual income: 5 million yen

Lifetime earnings: 250 million yen

Net income: 3.9 million yen/year (about 250,000 yen/month)

Bonuses: 2 months’ salary, twice a year

In this simulation, we assume:

Housing loan

Life/medical insurance

Car loan

Education loan

Revolving payments

Altogether, this results in loan/insurance payments of 160,000 yen per month.

With a net monthly income of 250,000 yen,

after paying 160,000 yen, about 90,000 yen remains.

That’s still a realistic figure for living expenses, right?

So let’s consider it as a relatively typical household scenario.

—

(1) Housing loan example

Loan amount: 30 million yen

Interest rate: 1.5% (fixed)

Loan term: 35 years

In this case…

(Source: [https://loan.mamoris.jp/repayment.asp](https://loan.mamoris.jp/repayment.asp))

The total repayment ends up being about 38.6 million yen.

In other words, borrowing 30 million yen means

you’ll pay an extra 8.6 million yen in interest alone.

Special Thanks OpenAI and Perplexity AI, Inc