管理人オススメコンテンツはこちら

「所得代替率は減っていく|減る年金、どうする?対策を考えよう」

〜前回のつづき〜

●“安心”を国に委ねる時代は終わった~年金制度の限界、見えてますか?~

所得代替率は減っていくんですよ。

例えば

どういう事かというと

(出典:https://www.nikkei.com/article/DGXZQOUA025JS0S4A700C2000000/)

国は色んなケースを

想定してるんですけど

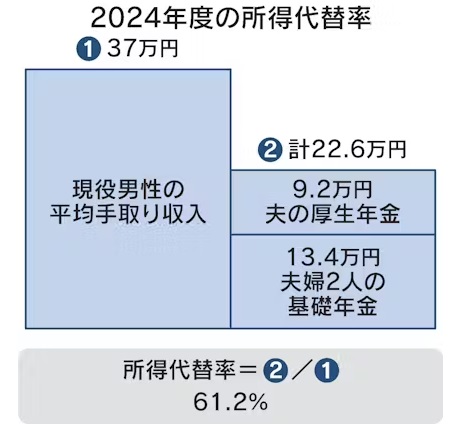

令和年の所得代替率は

61.2%なんですよ。

という事は

現役の時に

37万円の収入が有った人は

年金で22万6千円もらえる

という事になります。

国は

この所得代替率という考え方を

重視していて

年金給付については

『ゼロか100か』なんて話は

してないんですよね。

論点は割合補填であると。

国は

色んなケースを想定していて

・物価上昇率

・賃金上昇率

・運用利回り

・出生率

・寿命

など

色んな指標をベースにして

今後どれぐらい

所得代替率をキープ出来るか?

というのを

検証してるんですよね。

なので

年金制度が破綻して

1円も貰えなくなる

という事は無い。

無いんだけど

この所得代替率は減っていく

という事がわかってるんですよ。

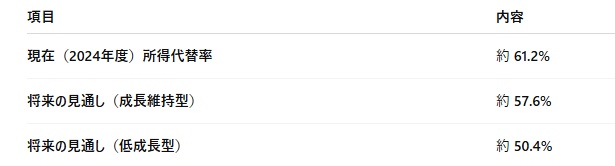

概ね40〜50%の

所得代替率になるのではないか

という所です。

だから

もらえる年金が減るというか

現役時の所得に比べたら

所得代替率というのは

下がっていくというのは

確実だという事です。

これは妻子ありの

一般的なケースで

という事です。

●年金はくれる。でも、守ってはくれない~足りない未来は、今しか埋められない~

年金制度に対する誤解のひとつに

『現役時代の収入をそのまま保証してくれるもの』

という思い込みがあります。

しかしそもそも年金は

現役時の収入を

100%補償する制度ではない。

厚生労働省が示している

所得代替率は

将来的に40〜50%程度にまで

下がるとされています。

つまり

どんなに現役時代の給料が

高かろうと低かろうと

年金で受け取れる金額は

その半分以下にとどまる

可能性が高いのです。

この現実を前にして

選択肢は2つしかありません。

(1)足りない分を自分で備えておくこと

(2)老後の生活水準を現役時代より下げること

あるいは

この2つを組み合わせるしかない

ということです。

つまり

自分には年金の問題なんて

関係ないと思っている人も

実際には何らかの形で

この問題に向き合わなければならない

立場にあります。

今の収入と同じ水準の生活を

年金だけで維持できると

考えているのであれば

それは

非常に危うい幻想です。

収入も下がり

支出も変わる老後の現実に対して

何の準備もなく臨むことは

制度設計の本質を

見誤っている

と言えるでしょう。

安心を

国に委ねる時代は終わった。

これからは

制度を正しく理解し

足りない分をどう補うかを

真剣に考える時代です。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

年金制度の所得代替率は今後、現役時代の収入の40〜50%程度まで低下すると見込まれています。

たとえば、現役時に月37万円の収入があっても、将来の年金は約22万円程度にとどまる可能性が高いのです。

国は年金財政の持続性をさまざまな条件で検証しており、年金給付がゼロになることはありませんが、現役時収入を完全に補償するものではないことが制度設計の本質です。

したがって、安心を国に委ねる時代は終わり、自分自身で不足分を備えるか、生活水準を下げるか、あるいは両方の対応が必要です。

これからは年金だけに頼らず、老後の資金計画を真剣に考えることが求められています。

-

- https://virtual-area.net/?p=5335

- https://www.roushikyo.or.jp/?p=we-page-menu-1-2&category=19325&key=21769&type=content&subkey=346089

- https://www.mizuho-rt.co.jp/business/consulting/articles/2024-k0043/index.html

- https://www.shaho-net.co.jp/nenkin_guide/98.html

- https://www.nikkei.com/article/DGXZQOUA025JS0S4A700C2000000/

≪≪Chat-GPTくんによる英訳≫≫

〜Continuation from the previous post〜

【The Era of Relying on the Government for Peace of Mind Is Over— Can You See the Limits of the Pension System? —】

The income replacement ratio is declining.

What does that really mean?

([Source: https://virtual-area.net/?p=5335](https://virtual-area.net/?p=5335))

The government has run simulations based on various future scenarios.

As of the Reiwa era, the income replacement ratio sits at 61.2%.

In other words, someone earning ¥370,000 per month while working

would receive about ¥226,000 per month in pension after retirement.

The government places strong emphasis on this “replacement ratio” concept.

They’re not talking in extremes like “you’ll get everything” or “you’ll get nothing.”

The real issue is how much of your income the pension system can replace.

They consider factors such as:

Inflation rate

Wage growth

Investment returns

Birth rate

Life expectancy

Based on these variables, they continuously evaluate how much of the replacement ratio can be sustained.

So no — the pension system won’t collapse to the point where you get nothing.

But yes — the replacement ratio is steadily shrinking.

It’s projected to fall to around 40–50% in the coming years.

That means you won’t necessarily receive less in absolute terms,

but compared to your working income, the portion replaced by pensions will definitely shrink.

And note:

These projections are based on a standard model household with a spouse and children.

—

【They’ll Give You a Pension — But They Won’t Protect You— The Future Gap Can Only Be Filled Today —】

One common misunderstanding about the pension system is the belief that

it guarantees your full working income after retirement.

But the truth is, pensions were never designed to replace 100% of your salary.

According to the Ministry of Health, Labour and Welfare,

the future income replacement ratio is expected to drop to 40–50%.

That means whether your working income was high or low,

your pension payout will likely be less than half of that amount.

Given this reality, you only have two options:

1. Prepare in advance to cover the shortfall, or

2. Lower your standard of living in retirement.

Realistically, you’ll probably need to do both.

So if you think the pension issue doesn’t apply to you — think again.

Anyone who plans to retire will face this challenge in some form.

If you believe you can maintain your current lifestyle with only your pension,

you’re buying into a dangerous illusion.

In retirement, income drops — and expenses change.

Facing that future with no preparation means you’re misunderstanding

what the pension system was ever meant to do.

—

The age of depending on the government for your future is over.

Now is the time to understand the system — and seriously plan how you’ll fill the gap.

Special Thanks OpenAI and Perplexity AI, Inc