.jpg)

管理人オススメコンテンツはこちら

「52兆円の収入|公的年金の未来を守るための条件」

〜前回のつづき〜

●あなたの安心を国任せにしない覚悟はありますか?~制度は続くが余裕は続かない~(つづき)

公的年金が破綻する3つの条件(続き)

(3)積立金

GPIF(年金積立金管理運用独立行政法人)

が運用している積立金から

高齢者に支払いされています。

年金は運用もされています。

●年金、まだ積んでるだけで安心してる?~積んでるのは安心じゃない、不安の先送りだ~

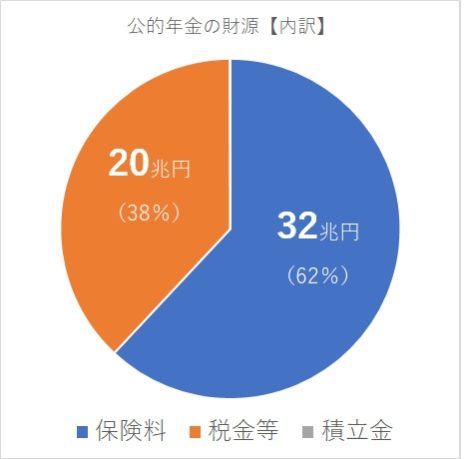

具体的に数字で見てみましょう。

(出典:https://kobito-kabu.com/nenkin-hatan/公的年金の財源/)

これが平成29年度の

公的年金の財源の円グラフです。

制度全体で

52兆円の収入が有るんですね。

公的年金の財源なんですけど

公的年金制度全体で

52兆円の収入がある。

積立金は

人口がもっと減ってきたら

取り崩される。

今は保険料と税金で

賄えているという事です。

まだ出番が無い。

現状は保険料と税金のところで

今のところ公的年金というのは

まかなわれています。

上記の52兆円というのが

高齢者に対する年金給付として

使われている訳です。

・税金

・保険料

という所ですね。

●年金未納? サラリーマンには幻想です~安心しろ、年金はほぼ強制徴収だ~

前回お話しした通り

年金がもらえなくなる3つの条件は

(1)今現在働いてる現役世代が誰も年金保険料を納めない

(2)誰も税金自体を納めない

(3)積立金が完全に枯渇

でした。

本当にこんな事が起こるのか

考察してみたいと思います。

(1)今現在働いてる現役世代が誰も年金保険料を納めない

これは非現実的だと思います。

国民年金には

3種類の加入者がいます。

・1号被保険者

・2号被保険者

・3号被保険者

これだけ聞くと

言葉が難しいので

イメージ的には

1号:自営業者

2号:会社員や公務員

3号:会社員や公務員の妻

それぞれイメージ的に

はこんな感じです。

それぞれの人数は

どんな感じかと言うと

(出典:https://www.gov-online.go.jp/useful/article/201309/5.html)

人数はそれぞれ上記の通りです。

とかたまにニュースで

話してたりするんですけど

これは1号被保険者の話です。

だからこれは

自営業者に限った話なんですよね。

年金制度全体で見た

未納率というのは

2%ぐらいです。

なぜなら

サラリーマンや公務員が多いから

です。

サラリーマンや公務員というのは

給与から天引きなんですよね。

だからそもそも

未納の問題は起きない。

給料から先に天引きされるので

未納になりようがない

ということですね。

という事は

ほとんどの人は

必ず年金保険料は

強制的に納めてる

という事です。

国民全員が

フリーランス・自営業者になったら

話はまた別です。

だから結論としていえば

年金保険料を誰も納めなくなるなんて事は

あり得ません。

現状32兆円もの

徴収に成功してます。

一番納めてるのは

・会社員

・公務員

なので

全員が自営業者になって

支払いをしないという事にならない限りは

全員強制的に徴収されてる。

だから

(1)今現在働いてる現役世代が誰も年金保険料を納めない

というのはあり得ません。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

公的年金の積立金は、年金積立金管理運用独立行政法人(GPIF)が運用しており、現時点では主に現役世代の保険料と税金で年金給付が賄われています。

制度全体では年間52兆円の収入があり、積立金は人口減少に伴う不足時に取り崩される仕組みですが、今はまだ使われていません。

保険料の未納は自営業者の一部に限られ、会社員や公務員は給与から天引きされているためほぼ全員が納めています。

このため、現役世代が全員保険料を納めなくなることは現実的ではなく、年金制度の破綻は積立金の枯渇や保険料の全未納、税金の全非納付など極めて異例の状況が重ならなければ起こりにくいと言えます。

したがって、「積んでいるだけだから安心」というわけではなく、将来の環境変化に備えた見直しが必要ですが、公的年金は今も多くの人の保険料によって支えられています。

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from Last Time~~

【Are You Prepared to Stop Relying on the Government for Peace of Mind?

– The System Will Survive, but the Surplus Won’t – (continued)】

—

The 3 Conditions for Public Pension Collapse (continued)

—

(3) Pension Reserve Fund

The reserve fund is managed and invested by the GPIF (Government Pension Investment Fund)

🔗 [https://www.gpif.go.jp](https://www.gpif.go.jp)

It’s from this fund that payments to the elderly are made.

Yes, pensions are also invested.

【Still feeling safe just because it’s piling up?

> What you’re stacking isn’t security — it’s postponed uncertainty.】

—

Let’s take a look at some numbers:

📊 (Source: [https://kobito-kabu.com/nenkin-hatan/公的年金の財源/](https://kobito-kabu.com/nenkin-hatan/公的年金の財源/))

This is a pie chart showing the revenue sources of Japan’s public pension system for fiscal year 2017 (Heisei 29).

The system as a whole brought in a total of ¥52 trillion.

This revenue — ¥52 trillion — makes up the entire income of the public pension system.

The reserve fund is intended to be drawn down when the population declines further.

Right now, the system is mostly sustained by insurance premiums and taxes.

In other words, the reserve fund hasn’t really been used yet.

Currently, pension benefits for the elderly are mostly covered by:

Taxes

Insurance premiums

—

【Unpaid pensions? That’s a myth — at least if you get a paycheck.

> Relax — pension contributions are practically mandatory.】

—

As mentioned last time, here are the 3 conditions under which pensions would stop being paid out:

1. No working-age people pay pension premiums

2. No one pays taxes

3. The reserve fund is completely depleted

Let’s examine whether these conditions could ever realistically occur.

—

(1) No working-age people pay pension premiums

This is highly unrealistic.

Japan’s national pension system consists of three categories of insured persons:

Category 1: Self-employed, freelancers, students, etc.

Category 2: Company employees and civil servants

Category 3: Spouses of Category 2 members (typically full-time homemakers)

If those terms sound complicated, think of it like this:

Category 1: Self-employed

Category 2: Office workers and public servants

Category 3: Their spouses

Each group has a different way of paying into the system.

📊 (Source: [https://www.gov-online.go.jp/useful/article/201309/5.html](https://www.gov-online.go.jp/useful/article/201309/5.html))*

The population distribution is available at the link above.

—

You may occasionally hear on the news something like:

“The pension non-payment rate has hit 40%!”

But that figure only refers to Category 1 — the self-employed.

So yes, that 40% refers only to freelancers and small business owners.

In reality, when you look at the entire pension system, the non-payment rate is around 2%.

Why?

Because the majority of people are salaried workers or civil servants.

And for them, pension contributions are deducted directly from their paychecks.

So in effect, non-payment isn’t even possible — it’s taken out before you see your money.

Which means:

> Most people are paying into the pension system automatically and mandatorily.

Unless every citizen suddenly becomes self-employed, this situation won’t change.

—

Conclusion:

The idea that “no one pays into the pension system” is not just unlikely —

> It’s practically impossible.

Currently, the government collects over ¥32 trillion annually in pension premiums.

Who pays the most?

Company employees

Civil servants

Unless the entire population switches to freelance work and opts out of payments,

> Pension contributions will continue to be forcibly collected.

So once again,

> Condition (1) — that no one pays pension premiums — simply won’t happen.

Special Thanks OpenAI and Perplexity AI, Inc