「搾取されつづけます|賢く生きるための保険講座」

これまで

保険についてお話ししてきました。

頭の整理をする意味で

まとめをしていきます。

色んな保険を勉強してきて

頭の中がパニックに

なってるかもしれないので

総まとめです。

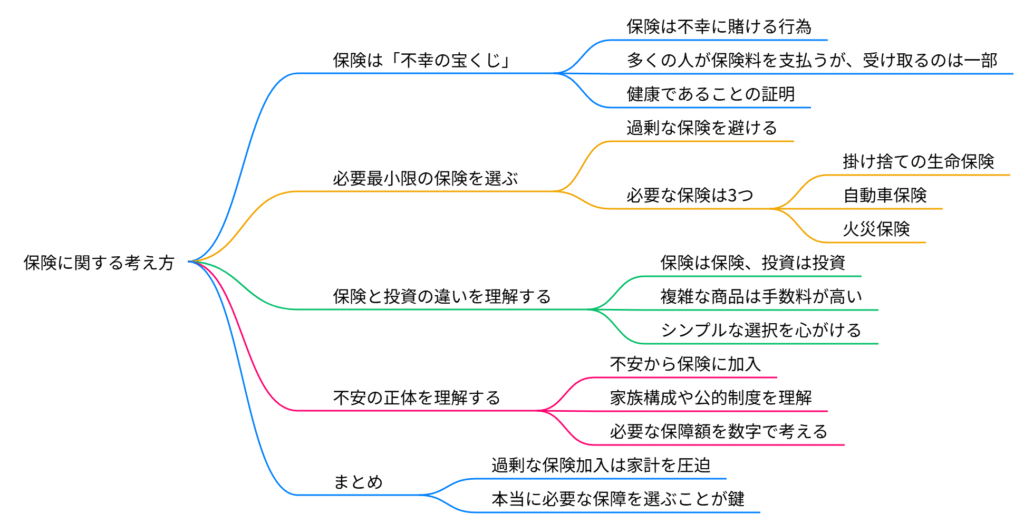

●保険は“備え”じゃない~不幸に賭ける大人のギャンブルだ~

保険とは何か?

人生で高い買い物

トップ3に入る金食い虫です。

そして他人の不幸が

おこるかどうかにベットする

不幸の宝くじです。

万が一不幸があった時に

お金が貰える宝くじシステムです。

あくまでも

お金がもらえるだけ。

なるべく

最低限しか入らないのが

世界の常識です。

日本人は

8割以上加入していますが

不要な人がいっぱいいます。

なるべく最低限しか入らない

というのが本来の形です。

●不安の正体は、無知と曖昧~“なんとなく不安”は、高くつく~

不安の正体を知りましょう。

本当に自分がいくら必要か

数字で考える。

・独身であれば本当に何千万もいるのか?

・一体誰に残すんだ?

・本当に必要なのか?

・病気になった時いくらいるのか?

・なんとなく不安だから

・これぐらいいりそうだから

これでは

いくらあっても足りません。

ちゃんと制度のことを知り

奥さん・子供がいるのかどうかで

変わってきます。

何となく不安じゃ

搾取されつづけます。

ちゃんと数字で

物事を考えられる様になりましょう。

●節約は最速の昇給~稼ぐより、まず“漏れ”を止めろ!~

保険に限らずですが

保険を通じて学んできたのが

固定費に敏感になるということです。

1万円支出を減らすということは

1万円所得が上がったのと

同じことです。

給料を1万円上げるのは

そう簡単な事ではありません。

1万円支出を減らす方が

自分1人で完結するので

給料を上げることより

はるかに簡単ですよね?

生活の質を

一気に落とさなくても

下げることができます。

この1万円を給料に換算した場合

税金等の為1万3千円程度

昇給させなければなりません。

給料が上がったとしても

1万円まるまるは

手元に来ません。

手取りになる際には

税金が引かれてしまいます。

大体の所得層の人が

3割程度源泉徴収されます。

1万円支出を減らすということは

1万3千円昇給したのと同じぐらい

価値があります。

だから保険に限らず何にでも固定費には

敏感になっていただきたい。

これから何度も出てきます。

●“ラクにまとめる”ほど、複雑で高くつく~バラして考える。これが、お金に強くなる第一歩~

・保険は保険

・投資は投資

・貯蓄は貯蓄

一緒にしない。

混ぜるな危険!

保険は

掛け捨ての保険に入ればいいし

最低限の役割を

果たしてくれればいいんです。

投資をしたいんだったら

投資商品をちゃんと買う。

保険会社を通じて

投資商品を買う必要はないです。

貯蓄は貯蓄。

貯金したいのであれば

貯金すればいいんです。

一緒にしない。

複雑な投資商品や保険商品は

不要です。

シンプルな商品でいい。

わかりやすいもので十分。

みんなこれを

まとめて考えるのが

面倒くさいんです。

だから

考えるのが面倒だから

まとめて簡単な商品にしちゃう。

中身は複雑な商品で

やりたい様にやられてしまう。

証券会社や保険会社の

養分にされてしまいます。

バカ高い手数料を払って

回り道をしなければならない。

こんなに

馬鹿馬鹿しいことはない。

ちゃんと

それぞれ別に考えるというのが

大事です。

●死んだ後より生きてる今を大切に~安心料で人生を削っていませんか?~

無駄な保険が

豊かな生活を邪魔するんですよ。

不要な保険が多すぎる。

積み立ての生命保険や

医療保険、養老、学資・・・

不要な積み立ての保険が

一杯ありすぎる。

こんな保険は入らなくていい。

あなたの人生を豊かにするのは

保険ではありません。

死んだ後の事や

病気になった時の事を

考えるのは大事。

ただそれより

生きている間の豊かさを

ちゃんと考えて下さい。

あなたの人生を豊かにするのは

保険じゃなくて

大切な家族や友人との時間ですよね?

その時間を削って

保険代を支払うために長く働いて

目の前の生活が苦しいのは

本末転倒です。

こんな馬鹿な話はありません。

何かおかしくないですか?

だから

あなたの人生を豊かにするのは

保険ではありません。

ちゃんと最低限にしておきましょう。

毎月のお金のストレスを減らして

健康的な生活を送りましょう。

●必要最小限の保険で、豊かな毎日を~保険の見直しで、家計も人生も軽やかに~

本当に必要な保険は

たったの3つです。

(1)掛け捨ての生命保険(家庭持ちのみ)

掛け捨ての生命保険は

家族(特に子ども)がいる人だけで

十分です。

独身や

すでに経済的に自立した

配偶者しかいない場合には

基本的に不要です。

(2)対人対物無制限の損害保険(車を持っている人のみ)

対人・対物無制限の自動車保険は

車を運転する人限定ですが

事故による

高額な賠償リスクに備えるために

必須です。

ただし

過剰な補償やオプションは避けて

必要最小限の補償にとどめましょう。

(3)火災保険

火災保険は

・住宅を持っている人

・借りている人

に加入が求められる

ケースが多いですが

生活基盤を守るために

必須の保険です。

以上(1)~(3)の

この3つ。

これら全部払っても

月々1万円行かないはずです。

逆に言えば

それ以上払っている場合は

何かムダな保険に入っている

可能性が高いということ。

保険にお金を吸い取られ

毎月の生活が圧迫されていては

本末転倒です。

大切なのは

必要最小限に保険を絞ること。

保険に縛られず

本当に豊かな人生を手に入れるために

一度見直してみてください。

保険が

家計を圧迫している状態を脱脚して

豊かな人生を送りましょう。

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

保険は「万が一」に備えるものと思われがちですが、実際は人生でトップクラスの高額な出費であり、「不幸の宝くじ」のような側面があります。

本当に必要な保険は、家庭持ち向けの掛け捨て生命保険、車を持つ人のための対人対物無制限自動車保険、そして住宅所有や賃貸者向けの火災保険の3つだけで十分です。

なんとなくの不安や無知から過剰に加入すると、今の生活が圧迫されてしまいます。

保険・投資・貯蓄は混ぜず、シンプルに分けて考えましょう。

無駄な保険を見直し、必要最小限に絞ることで、家計も心も軽くなり、本当に大切な家族や自分の時間を守ることができます。

[1] https://www.jili.or.jp/research/report/zenkokujittai.html

[2] https://www.navinavi-hoken.com/articles/life-subscription

[3] https://www.jili.or.jp/research/report/9849.html

[4] https://www.fnn.jp/articles/-/849831

[5] https://ins.minkabu.jp/columns/insurance-enrollment-rate-230720

[6] https://okane-kenko.jp/article/insurance/life/htc-life/life-insurance-participation-rate

[7] https://www.navinavi-hoken.com/articles/medical-subscription

[8] https://www.sonpo.or.jp/report/statistics/syumoku/index.html

≪≪Chat-GPTくんによる英訳≫≫

We’ve talked a lot about insurance.

Now, let’s organize our thoughts and wrap things up.

After learning about so many different types of insurance, you might feel overwhelmed and confused—so here’s a final summary.

—

【Insurance isn’t “preparation”—it’s an adult gamble on misfortune.】

What is insurance?

It’s one of the top three most expensive purchases you’ll make in your lifetime.

And essentially, it’s a lottery that bets on whether misfortune will happen to someone.

If bad luck strikes, you get paid. That’s it. You just get money.

That’s why, globally, it’s common sense to carry only the bare minimum coverage.

Yet in Japan, over 80% of people are insured—many of them unnecessarily.

The ideal approach? Keep it to the absolute minimum.

—

【Fear comes from ignorance and vagueness—“Just in case” will cost you dearly.】

Let’s identify the real source of our anxiety.

You need to figure out how much you actually need—with numbers, not feelings.

Do you really need millions just because you’re single?

Who are you leaving that money to?

Is it really necessary?

How much do you need if you get sick?

Are you just vaguely worried?

Are you guessing based on gut feeling?

This kind of thinking will never be enough—no matter how much you prepare.

You need to learn how the system works. Whether you have a spouse or kids makes a big difference.

If you live in “vague fear,” you’ll be exploited.

Let’s learn to think in numbers.

—

【Saving is the fastest raise—Patch the leaks before earning more.】

This lesson isn’t just about insurance—it’s about becoming sensitive to fixed costs.

Reducing your expenses by ¥10,000 is the same as increasing your income by ¥10,000.

But getting a ¥10,000 raise? Not so easy.

Cutting ¥10,000 in expenses is something you can do on your own, without anyone’s permission. That’s way easier than trying to increase your salary.

You don’t have to sacrifice your lifestyle to do this.

To earn that same ¥10,000 after taxes, you’d need a raise of about ¥13,000.

Because when your salary goes up, taxes take a chunk.

Most people lose around 30% of their raise to withholding taxes.

So cutting ¥10,000 in expenses = almost a ¥13,000 raise in value.

That’s why you should always be very cautious about fixed costs, especially insurance.

This point will come up again and again.

—

【The more you simplify, the more it costs—Separate your finances.】

Insurance is insurance

Investment is investment

Savings is savings

Don’t mix them.

Warning: Do not combine!

If it’s insurance you need, get simple term insurance. That’s enough.

If you want to invest, buy proper investment products.

You don’t need to buy investment products through insurance companies.

If you want to save, just save.

Don’t mix them.

Complicated financial products—combo plans of insurance + savings + investment—are totally unnecessary.

Simple, easy-to-understand products are enough.

People lump everything together because thinking separately feels like a hassle.

But when you choose something “simple,” you often end up with a complex and overpriced product instead.

You become a cash cow for securities and insurance companies.

You’ll pay absurd fees and waste years of your financial life.

That’s just stupid.

Always separate and think about each goal individually.

—

【Prioritize your life, not your death—Is “peace of mind” costing you your future?】

Unnecessary insurance is holding back your happiness.

There’s way too much useless insurance out there:

Savings-type life insurance

Medical plans

Endowment policies

Education insurance

Most of them are unnecessary.

These are not what make your life better.

Of course, it’s important to consider death and illness. But more important than that is how to live well right now.

It’s not insurance that enriches your life—it’s time with your family and friends.

If you’re working longer hours just to pay insurance premiums and sacrificing the joy of today…

That’s completely backwards.

Isn’t that crazy?

Let’s be clear: Insurance doesn’t make your life better.

Keep it to a minimum.

Reduce monthly financial stress and aim for a healthier lifestyle.

—

【A richer life with just the essentials—Lighten your household budget with a policy review.】

There are really only three types of insurance you need:

(1) Term life insurance (for those with dependents)

Only necessary if you have a family—especially children.

If you’re single or your spouse is financially independent, you probably don’t need it.

(2) Liability auto insurance (unlimited coverage) for drivers

If you drive, this is essential to cover massive liability in case of accidents.

But avoid unnecessary extras—keep it minimal.

(3) Fire insurance

Whether you own or rent, this protects your living space and is often required.

That’s it. Just these three.

Even combined, they shouldn’t cost you more than ¥10,000/month.

If you’re paying more, you’re probably wasting money.

Let’s stop bleeding cash on insurance and focus on living fully.

The key is minimal insurance, maximum life.

Review your coverage, free up your finances, and live a truly rich life.

Special Thanks OpenAI and Perplexity AI, Inc