管理人オススメコンテンツはこちら

「自分のお金を使わずに儲ける方法|成功する投資家の借金活用術」

〜前回のつづき〜

●「借金=悪」って、誰が決めた?~本当の金持ちは“借りて”増やす~

お金持ちというのは

借金を上手に使うんですよ。

・いい借金

・悪い借金

があって

借金=悪い事

というイメージじゃないですか?

もちろん

良くない借金というのも

有るんですよ。

でも

いい借金の例というのが

不動産投資なんですよね。

金利とかの考え方の話なんですけど

例えば

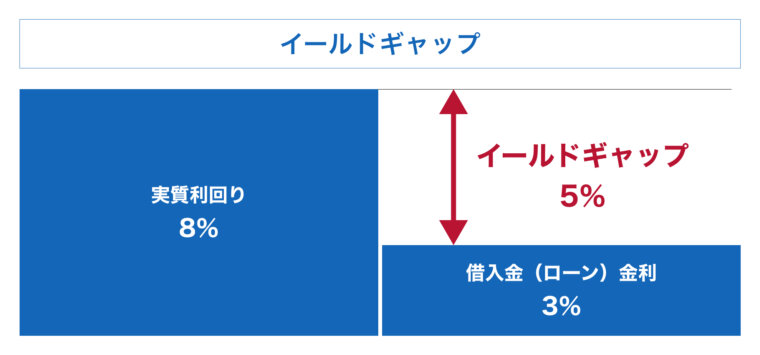

1億円を金利1%で借りて

不動産投資で8%で運用する。

そうすると

8-1=7%

1億円の7%が

利ざやになるんですよね。

自分のお金ではなく

他人から借りたお金で物件を買って

1%で借りて8%で運用する。

そうすると

毎年1億円の7%が

利ざやになる訳ですよね?

そうすると

1億円の7%=700万円が

毎年手に入るんですよね。

すごいですよね?

これを

(出典:https://www.hajime-kensetsu.co.jp/asset/staffblog/leverage/)

『イールドギャップ』といいます。

金利の利ざやの事なんですけど

自分のお金を使わずに

儲ける方法ですよね。

実際には

毎月の元本の返済があったりとか

キャッシュフローの計算があったり

もう少し複雑なんですけど

こういう

いい借金の使い方というのも

有るんですよ。

借金=ダメという事ではなくて

こういういい借金もあるという事も

覚えておいて欲しい。

ただしぼったくり物件とかを

これで間違えて買っちゃうと

特に

ワンルームマンション投資なんかだと

再起不能になってしまうので

ご注意下さい。

これで買う物件が

ロクでもない物件だったりとか

投資先を間違えてたら

真逆の事が起きちゃうので

これは気をつけてください。

考え方の基本の話です。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

お金持ちは借金を上手に活用しています。借金には「いい借金」と「悪い借金」があり、必ずしも借金=悪いことではありません。

例えば、不動産投資では、低い金利(例:1%)でお金を借りて、高い利回り(例:8%)で運用することで、その差額(イールドギャップ)が利益となります。

つまり、自分のお金を使わずに、他人から借りたお金で資産を増やすことができるのです。

ただし、毎月の元本返済やキャッシュフローの計算など、実際はもう少し複雑ですし、物件選びや投資先を間違えると大きな損失につながるリスクもあります。

特にワンルームマンション投資などは注意が必要です。

借金にも賢い使い方があることを知り、リスクを理解した上で活用することが大切です。

[1] https://www.musashi-corporation.com/wealthhack/yield-gap

[2] https://www.you-me-machidukuri.co.jp/blog/realestate-investment-yieldgap/

[3] https://rita-hudousan.com/info/page_479.html

[4] https://sumaity.com/realestate_investment/press/881/

[5] https://r-entrance.net/infosearch/1/180

[6] https://yamatozaitaku.com/column/realestate-investment/20210122/

[7] https://shikin.yayoi-kk.co.jp/study/borrowing/fudosankatsuyo-05.html

[8] https://home4u-owners.jp/contents/construction-apartment-3-2-9808

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous post~

【”Who said debt is bad? — The truly wealthy borrow to build wealth.”】

Wealthy people know how to use debt wisely.

There are two types of debt:

Good debt

Bad debt

But most people tend to think:

Debt = Something bad, right?

Of course, there is such a thing as bad debt.

But a good example of good debt is real estate investment.

Let’s talk about interest rates and how this works.

Say you borrow 100 million yen at an interest rate of 1%,

and invest it in real estate with an 8% return.

That gives you a spread of:

8% – 1% = 7%

So 7% of 100 million yen becomes your profit.

In other words, you’re using borrowed money — not your own —

to buy property at a 1% interest rate and earn 8%.

That 7% difference is your annual gain.

So, 7% of 100 million yen = 7 million yen per year.

You earn that every year.

Pretty amazing, right?

This concept is called the “Yield Gap.”

(Source: [Hajime Kensetsu Blog](https://www.hajime-kensetsu.co.jp/asset/staffblog/leverage/))

It refers to the profit margin created by the gap between borrowing cost and return on investment —

a way to make money without using your own capital.

Of course, in reality, things can get more complex.

You’ll need to deal with things like monthly principal repayments and cash flow management.

But the point is:

there are smart ways to use debt to your advantage.

So don’t just think “debt = bad.”

Understand that good debt exists, and learn how to use it.

However…

If you buy a bad property using this strategy —

especially something like a tiny one-room apartment as an investment —

you could end up financially ruined.

If the property is a rip-off,

or if you invest in the wrong asset,

the outcome could be the complete opposite of what you intended.

So be very careful.

This is a fundamental mindset when it comes to building wealth.

Special Thanks OpenAI and Perplexity AI, Inc