「保険貧乏になっている人が非常に多い|安心・快適な生活のために!通信費&保険の見直し大作戦」

〜前回のつづき〜

●保険ってホントに“安心料”か?~意味のない安心が、あなたを貧乏にする~

では実際には

何を見直したらいいのでしょう?

(1)通信費

(出典:リベラルアーツ大学)

大手3キャリア

・docomo

・au

・Softbank

を使ってる人が多いと思います。

これを

格安SIMというものに変えるだけで

月々大体5千円ぐらいは

安くなります。

5千円安くなるということは

税金等を考えたら

実際は給料にしたら

7千円ぐらい稼がないといけない。

それぐらい効果が有る

という事です。

一番最初に

一回だけやっておけば

ずっと効果が有る。

金額にするとすごく大きいので

やってみてはいかがでしょうか?

私自身はau回線を使った

UQモバイルを使っています。

繋がりやすさは

やはりさすがau回線といった所で

非常に満足しています。

格安SIMだと

昼時にネットが遅くなる

という事が言われていますが

特に不自由を感じた事はありません。

乗り換えも

auショップに行って

SIMを変えるだけなので

非常に簡単です。

通信費が5千円下がるということは

確実に会社の給料が

7千円上がるのと同じ事ですからね。

人によっては

1万円ぐらい安くなった

という人もいます。

またスマホ以外にも

家のネット回線も安くできる。

自宅のネット回線を

・安く

・早く

する事が出来る。

私はマネーフォワード光を使っています。

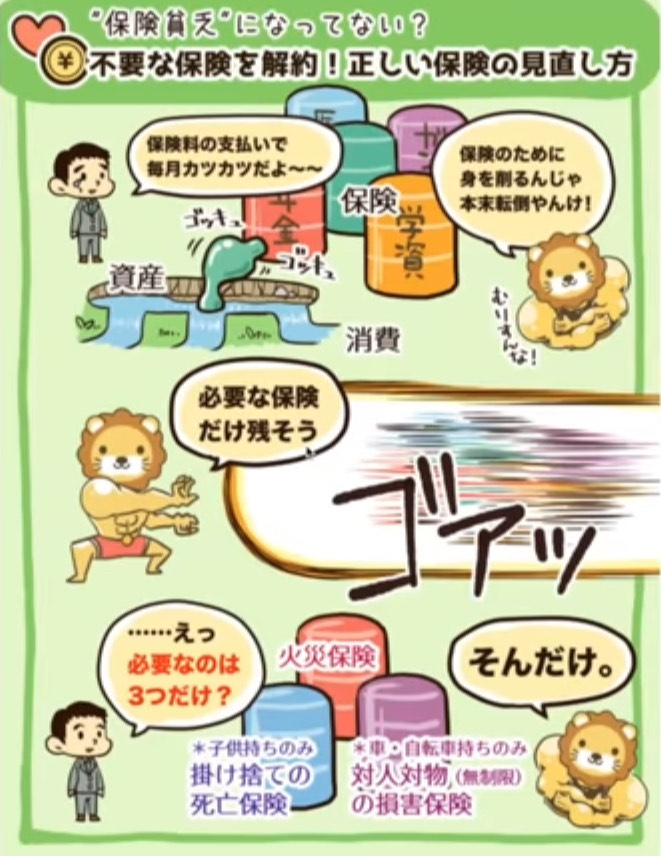

(2)保険

(出典:リベラルアーツ大学)

この日本においては

保険貧乏になっている人が

非常に多いんですよ。

世界で一番保険に入る国民性なので。

本当によくわからず

「まわりがみんな入ってるから」

という理由で入ってる人が多いんですね。

だから保険貧乏になってしまったら

いったい何のために保険に入るのか

意味が無いという事ですね。

必要な保険というのは

ずっとお話ししているように

2-a)掛け捨ての死亡保険(小さい子供がいる場合)

一体誰のために残すのか?

というのを考えてみましょう。

2-b)対人対物の損害保険(自動車・バイク・自転車)

2-c)火災保険

これだけかけておけば十分です。

他のものはいりません。

・学資保険

・ガン保険

などはいらないという事です。

さらに

・死亡保険

・損害保険

・火災保険

どれにしても

定期的に内容を見直しましょう。

必要な保険にしても

まずはいらないものを

解約するんだけど

必要な保険についても

内容の見直しは必要です。

会社を変更したり

内容を見直すだけで

すごく安くなったりします。

例えば

自動車保険であれば

車両保険は基本的に不要なので

外す事によって楽になりますよね。

月々の固定費が下がります。

●不要な保険に人生を削られないで~正しい知識で賢く守る家計~

保険は必要最低限に見直す

というのも重要です。

積立や貯蓄性のある保険はいらない

という事です。

・学資保険

・養老保険

・個人年金

・外貨預金

・ペット保険

この辺は

入るメリットはありません。

もったいないという事です。

・保険は保険

・投資は投資

混ぜるなキケン!です。

ちゃんと分けて考えましょう

という事ですね。

保険の内容を

ちゃんと理解して

投資というものと

保険というものの

それぞれの内容を

ちゃんと理解していたら

各種雑多な保険は

必要ないんですよ。

だから

ちゃんと理解していきましょう

という事です。

保険については今までのお話しを

参考にして頂けたらと思います。

・医療保険について

↓

・生命保険について

↓

#7 【いらない保険】本当に必要な生命保険はこれだけ!~1~

・ペット保険について

↓

・自動車保険について

↓

・各種保険について

↓

・学資保険について

↓

・地震保険について

↓

・個人年金について

↓

・積立保険について

↓

・払済保険について

↓

#72 払い済み保険てお得?〜保険を解約する時の考え方〜1~

・養老保険について

↓

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

保険や通信費の見直しは、家計改善に大きな効果があります。

まず通信費は、大手キャリア(docomo、au、Softbank)から格安SIMに乗り換えるだけで月約5,000円節約でき、税金を考慮すると実質7,000円以上の収入増と同じ効果があります。乗り換えも簡単で、通信品質も十分満足できる場合が多いです。

次に保険ですが、日本は保険加入率が高く、不要な保険に加入して「保険貧乏」になっている人が多いです。必要なのは、掛け捨ての死亡保険(子どもがいる場合)、対人対物の損害保険、火災保険だけで、学資保険やガン保険、養老保険、個人年金、ペット保険などは不要です。保険は投資と混同せず、必要最低限に絞り、定期的に内容を見直すことが重要です。

これらを実践することで、無駄な支出を減らし、家計を賢く守ることができます。

Citations:

[1] https://kakaku.com/mobile_data/sim/ranking.asp

[2] https://pixela.co.jp/mobiledash/cheap-sim-optical-line-set/

[3] https://www.uqwimax.jp/mobile/gimon/sim_averageprice/

[4] https://my-best.com/26457

[5] https://www.ms-tetsujin.com/ms_report_detail.shtml?1096603-0=

[6] https://www.e-mansion.co.jp/bbs/thread/15339/res/1-500/

[7] https://kakaku.com/mobile_data/sim/

[8] https://www.iijmio.jp/gigaplan/

[9] https://www.linemo.jp/plan/

[10] https://redrb.heteml.net/satohtetsuo/index3.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous post~

【Is insurance really a “peace-of-mind fee”?—False security could be making you poor—】

So what exactly should you review in your finances?

—

(1) Communication Costs

(Source: Liberal Arts University)

Many people in Japan still use one of the big three mobile carriers:

– docomo

– au

– SoftBank

But by switching to a low-cost SIM, you can save around ¥5,000 per month.

Saving ¥5,000 monthly is equivalent to earning about ¥7,000 pre-tax, so the impact is significant.

This is a one-time change that keeps saving you money forever—a no-brainer!

I personally use UQ Mobile, which runs on au’s network, and I’ve been very satisfied with the connectivity.

Some say low-cost SIMs slow down during lunchtime hours, but I’ve never had any real issues.

Switching was easy—just visited an au shop and changed the SIM card. That’s it.

For some people, the savings are even greater—up to ¥10,000 per month.

Also, don’t forget about your home internet. It can often be made cheaper and faster.

I personally use Money Forward Hikari, and it’s working great.

—

(2) Insurance

(Source: Liberal Arts University)

In Japan, many people are insurance-poor.

That’s because Japan has the highest insurance penetration rate in the world.

Most people don’t really understand what they’re buying—they just join because “everyone else is doing it.”

But if insurance puts a strain on your finances, then what’s the point?

The only insurance you really need is:

2-a) Term life insurance

(If you have small children who rely on your income)

Ask yourself: Who exactly am I leaving this money for?

2-b) Liability insurance

(For car, motorbike, or bicycle accidents)

2-c) Fire insurance

(For protecting your home)

These three types are enough for most people. You don’t need:

– Education insurance

– Cancer insurance

– Or most other plans.

Even for the necessary types of insurance, it’s important to review the policy details regularly.

Sometimes just changing providers or revising your plan can drastically lower your premiums.

For example:

Most people don’t really need car damage insurance on their auto policy. Dropping it can reduce your fixed monthly costs.

—

【Don’t let unnecessary insurance drain your life—Protect your household with the right knowledge—】

It’s essential to keep insurance to a minimum.

You don’t need savings-type or investment-linked insurance.

That includes:

– Education insurance

– Endowment insurance

– Private pension insurance

– Foreign currency savings products

– Pet insurance

These offer little to no real benefit.

In short: It’s a waste of money.

—

Key Principle:

– Insurance is insurance

– Investment is investment

Mixing the two is dangerous!

Understand the difference, and don’t combine them.

If you take the time to learn what insurance truly is, and understand what investing is all about too,

you’ll realize that most of the insurance products out there are unnecessary.

Let’s learn and make smarter decisions together.

—

For more detailed breakdowns, check out the following topics:

– #6-1: Do You Really Need Medical Insurance?

– #7: The Only Life Insurance You Actually Need

– #7-2: Why Pet Insurance Isn’t Worth It

– #10-1: How to Save on Car Insurance

– #11: Insurance Summary

– #60: Why Education Insurance Is Unnecessary

– #63: Is Earthquake Insurance Necessary?

– #67: Why You Don’t Need a Private Pension

– #68: Can Savings-Type Insurance Really Yield High Returns?

– #72: Understanding “Paid-Up” Insurance — When to Cancel

– #86: Why Endowment Insurance Isn’t Recommended

Special Thanks OpenAI and Perplexity AI, Inc