管理人オススメコンテンツはこちら

「地獄の業火から永遠に出してもらえない|世界の宗教が“金利”を恐れた本当の理由とは」

〜前回のつづき〜

●利息を取ったら地獄に落ちる(つづき)

例えば

イスラム教で

利息が禁止されているという話は

有名ですよね。

イスラム教の聖典

『コーラン』には

こんな強い言葉が

書かれています。

「利息を取る者はあの世で地獄の業火から永遠に出してもらえないだろう」

(出典:吉村文成 利息を禁止した宗教の智恵 : おカネと資本についての一考察)

かなり恐ろしい表現ですよね。

聖典にここまで

強く書かれるということは

それだけ

『利息を取る』という行為が

罪深いものと考えられていた

ということです。

つまり

利息というものは

・神様の意思に反するもの

・倫理的に問題のあるもの

として扱われていたわけですね。

しかもそれが

宗教の中心的な教えである

聖典に書かれているのです。

次にユダヤ教です。

ユダヤ教は民族宗教なので

・同胞(ユダヤ人)

・外国人(異教徒)

でルールが異なります。

聖典には

次のように書かれています。

「外国人には利子を付けて貸してもいいが

同胞には利子を付けて貸してはならない」

(出典:吉村文成 利息を禁止した宗教の智恵 : おカネと資本についての一考察)

この考え方を

簡単にまとめると

こうなります。

・利息の力で仲間が繁栄するのはOK

・利息の力で仲間が苦しむのは絶対NG

つまり

『利息』という仕組みの力を

昔からよく

理解していたということなんですね。

ユダヤ人はこの利息の力を

非常に上手く使う民族だとも

言われています。

それからキリスト教。

実はキリスト教でも

16世紀の宗教改革までは

利息を取ることは

原則として禁止されていました。

そして現代でも宗派によっては

・高すぎる利息

・複利による利息

などを

制限しているところもあります。

ここまでをまとめると

・イスラム教

・ユダヤ教

・キリスト教

この三つの宗教では

利息というものが

・禁止されたり

・厳しく制限されたり

してきた歴史があります。

意外と知られていない

事実かもしれませんね。

ちなみに仏教では

利息そのものは

禁止されていません。

むしろ『金貸し』は

正しい職業の一つと

考えられてきました。

仏教で

禁じられている職業は主に

・武器や酒や毒などの売買

・盗賊

・死刑執行人

・漁師

・裁判官

など

殺生につながる可能性のある職業

です。

そのため

命を奪うことに関係しない金貸しは

問題ないと考えられていたわけです。

実際に歴史を見てみると、

・寺院がお金を貸す

・お寺が金融の役割を担う

といったことも

行われていました。

さらに明治時代には

寺院関係者が生命保険会社を

設立した例もあります。

つまり

・金利

・手数料

といった金融の仕組みを

むしろ積極的に活用していた

側面もあるのです。

ここで

重要な事実があります。

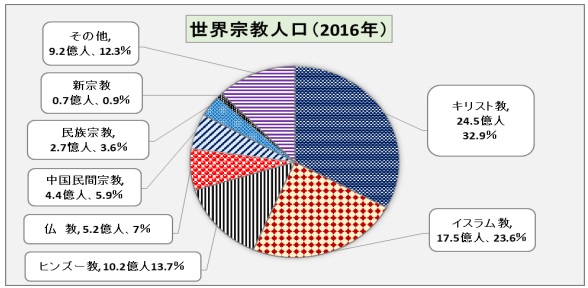

世界の人口は約74億人ですが

そのうち実に 42億人以上 が

・利息を禁止

・もしくは制限

している宗教を

信じています。

なぜなら

世界の宗教人口ランキングを見ると

(出典:https://www.tci.ac.jp/wp-content/uploads/2015/08/JMR_report_2017.pdf)

1位:キリスト教

2位:イスラム教

だからです。

この二つを合わせると

世界の人口の半分以上になります。

つまり

『利息』という仕組みは

世界的に見ても

非常にセンシティブな

テーマなんですね。

この事実は決して

軽く見てはいけない

ポイントだと思います。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

[PR]

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

イスラム教では利息を取ることが神に背く罪とされ、聖典コーランには「利息を取る者は地獄に落ちる」と記されています。ユダヤ教も利息を制限し、「同胞には利息をつけてはならない」と定め、仲間同士での経済的搾取を禁じています。キリスト教も16世紀の宗教改革までは利息取得を原則禁止し、現在も一部の宗派では高利や複利を制限しています。

これに対し、仏教では利息は禁止されず、金貸しは「殺生に関係しない職業」として認められ、寺院が金融や保険の役割を担った歴史もあります。

世界人口の半数以上を占めるキリスト教徒とイスラム教徒が利息を禁止または制限する教えを持つことから、利息は世界的に見ても非常にセンシティブなテーマといえるのです。

Citations:

[1]https://president.jp/articles/-/15032?page=1

[2]https://gentosha-go.com/articles/-/1514

[3]https://note.com/ikirudakesa/n/nb3a797529ed2

[4]https://chinosiokonan.com/archives/9451

[5]https://note.com/ia_wake/n/n2fe89e9ab61d

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous post~

If You Charge Interest, You Go to Hell (continued)

For example, it’s well known that charging interest is prohibited in Islam.

In the Islamic holy book, the Qur’an, there is a very strong statement about it:

> “Those who take interest will never be released from the fires of hell in the afterlife.”

> (Source: Fuminari Yoshimura, The Wisdom of Religions that Prohibited Interest: A Study on Money and Capital)

That’s quite a frightening expression.

The fact that such strong words appear in a sacred text shows just how seriously the act of “taking interest” was viewed.

In other words, charging interest was considered something deeply sinful.

Interest was treated as something that was:

Against the will of God

Ethically problematic

And this wasn’t just a casual opinion—it was written in the sacred scriptures that form the core teachings of the religion.

—

The View in Judaism

Next, let’s look at Judaism.

Judaism is an ethnic religion, so the rules differ depending on whether the other person is:

A fellow Jew (one of the same people), or

A foreigner (a non-believer)

In the scriptures, it says:

> “You may charge interest to foreigners, but you must not charge interest to your fellow people.”

> (Source: Fuminari Yoshimura, The Wisdom of Religions that Prohibited Interest: A Study on Money and Capital)

Simply put, the idea behind this is:

It’s acceptable if the power of interest helps your community prosper.

It’s absolutely unacceptable if interest causes suffering among your own people.

In other words, people already understood the power of the system of interest long ago.

It is often said that the Jewish people have historically been very skillful at using the power of interest.

—

Christianity and Interest

What about Christianity?

In fact, within Christianity as well, charging interest was generally prohibited until the Protestant Reformation in the 16th century.

Even today, depending on the denomination, there are still restrictions such as:

Excessively high interest rates

Compound interest

—

A Common Theme in the Three Religions

To summarize:

Islam

Judaism

Christianity

All three of these religions have histories in which interest was either:

Prohibited, or

Strictly limited.

This may be a fact that many people are not aware of.

—

What About Buddhism?

Interestingly, in Buddhism, interest itself is not prohibited.

In fact, money lending has traditionally been considered one of the legitimate professions.

In Buddhism, the occupations that are prohibited are mainly those connected to harming life, such as:

Selling weapons, alcohol, or poison

Theft or banditry

Executioners

Fishermen

Judges

These are considered “occupations that may lead to taking life.”

Because of that, lending money—since it does not directly involve taking life—was not seen as a problem.

Looking at history, we can see examples where:

Temples lent money to the public

Buddhist institutions played financial roles in society

Furthermore, during the Meiji era in Japan, there were even cases where people connected with temples established life insurance companies.

In other words, financial mechanisms such as:

Interest

Fees

were, in some cases, actively utilized.

—

More Than Half the World’s Population Follows Religions That Restrict Interest

Here is an important fact.

The world’s population is about 7.4 billion people, and more than 4.2 billion of them follow religions that:

Prohibit interest, or

Restrict it in some way.

(Source: [https://www.tci.ac.jp/wp-content/uploads/2015/08/JMR_report_2017.pdf](https://www.tci.ac.jp/wp-content/uploads/2015/08/JMR_report_2017.pdf))

Why?

Because if we look at the global ranking of religions by number of followers:

1st: Christianity

2nd: Islam

When you combine these two, they account for more than half of the world’s population.

In other words, the system of “interest” is, globally speaking, a very sensitive topic.

This is a fact that should not be taken lightly.

Special Thanks OpenAI and Perplexity AI, Inc