管理人オススメコンテンツはこちら

「平均というのはある種の幻|未来は予測不能、老後資金も同じ」

〜前回のつづき〜

●老後資金を計算出来ない理由

老後資金は

以下の計算式で求められるんですね。

(1)年間生活費✕(2)老後の年数

この2つの要素で

計算されるという事ですね。

(1)と(2)どちらも

そう簡単には計算出来ないんですね。

(1)年間生活費

これがそもそも

簡単に計算出来ないんですよ。

老後いくらぐらい必要だと考えるか

というアンケートを取った

調査結果が有るんですけど

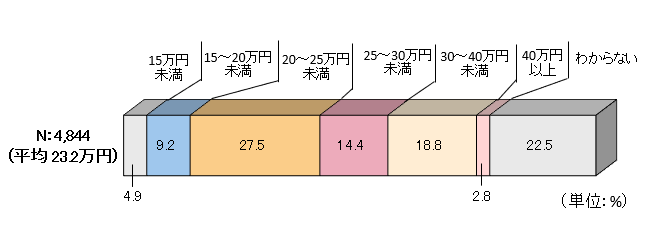

夫婦2人の老後最低日常生活は

こんな感じでした。

(出典:https://www.jili.or.jp/lifeplan/lifesecurity/1141.html)

月額平均で23.2万円必要だったという

アンケート結果だったんですね。

更にこの

夫婦2人の場合23.2万円というのは

最低日常生活費なので

ゆとりの有る老後生活費だったら

こんな感じになったんですね。

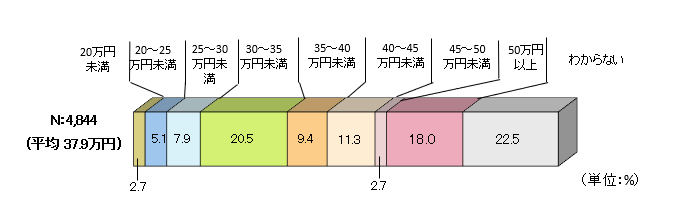

(出典:https://www.jili.or.jp/lifeplan/lifesecurity/1141.html)

夫婦2人で

豊かで余裕の有る老後生活費は

37.9万円必要だったと

そういうふうに

アンケートで答えてる方が多かった。

最低限の生活費にしろ

ゆとりの有る生活費にしろ

『わからない』と答えている層が

20%以上もいるというのは

興味深いんですね。

これを見て

「よし、ゆとり有る老後を目指すぞ!」

と年間生活費を

36.1万円✕12ヶ月=433.2万円

で計算しようと

こう考えた人は

ちょっと待って欲しいんですよ。

とにかく年間生活費が

433.1万円いるから

あとは

亡くなるまでの期間分という事で

貯めようとしてる人は

ちょっと待って欲しいんですよね。

私に言わせると

この433.1万円という数字が

大分怪しいんですよね。

なぜなら

予測が難しい生活費変動ポイントが

複数有るからですね。

・物価の変動

・生活スタイルの変化

・健康状態の変化

・時の経過による生活環境の変化

など沢山有るんですね。

例えば

一世帯あたりの通信費は

平成元年の場合は

6,200円だったのが

平成30年には

13,000円を超えてて

2倍強になってるんですね。

30年前の平成元年の時点で

こういう状況を

予想出来てましたか?

という話なんですね。

他にも

昔と大きく支出内容が異なってるという費用

は沢山有る訳なんですよね。

さらにこの

430万円という数字には

こういう問題も有るんですね。

自分個人が必要な金額は

果たして平均値と同じなのか?

・身長160cmのAさん

・身長180cmのBさん

2人しかいない世界を考えてみた場合

この世界の2人の平均身長は

170cmなんですよね。

でも170cmの人は

実際には存在してないんですよね。

だから平均というのは

ある種の幻とも言える。

家計支出についても

同じ話で平均の人なんて

実際には存在してないんですよね。

平均に合わせに行くという行為に

はたしてどれほど意味が有るのか?

これが疑問な訳ですよ。

これがまずは

(1)年間生活費についてです。

非常に計算が難しいんですよ。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

老後資金は「年間生活費×老後年数」で計算できるとされていますが、実際にはどちらも簡単に算出できません。

たとえば夫婦2人の場合、最低限の日常生活費は月23.2万円、ゆとりある生活には月37.9万円必要という調査結果があるものの、これはあくまで平均値であり個人差が大きいのです。

「必要額が分からない」と答える人も20%以上おり、多くの人にとって具体的な生活費の把握自体が困難です。

さらに今後の物価変動や生活スタイル、健康状態、社会環境の変化といった不確定要素が多く、将来の支出予測は難しくなります。

平均値は目安にはなりますが、実際の生活にぴったり当てはまるわけではありません。

老後資金の計算には、自身の状況や価値観を反映した柔軟な考え方が必要です。

-

- https://www.jili.or.jp/lifeplan/lifesecurity/1141.html

- https://www.jili.or.jp/research/report/chousa10th.html

- https://www.hokugin.co.jp/blog/028.html

- https://hoken-all.co.jp/article-5463/

- https://www.jili.or.jp/lifeplan/lifesecurity/1130.html

- https://www.jili.or.jp/lifeplan/lifesecurity/1133.html

- https://www.bk.mufg.jp/column/shisan_unyo/0056.html

- https://www.aizawasec-univ.jp/article/711474061348533b0f931c569adaa327f4b3c0f5.html

- https://www.fp.au-financial.com/media/shisan/article-128.html

- https://www.orixbank.co.jp/column/article/201/

- https://www.meijiyasuda.co.jp/find2/light/knowledge/list/39.html

- https://www.bk.mufg.jp/column/events/secondlife/0005.html

- https://www.jili.or.jp/research/chousa/8946.html

- https://www.manulife.co.jp/ja/individual/about/insight/column/article/column107.html

- https://www.smbc.co.jp/kojin/money-viva/money-jiten/0044/

- https://okane-recipe.saisoncard.co.jp/column/bm-0003/

- https://www.nantobank.co.jp/kojin/column/002/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous part~

### Why Retirement Funds Cannot Be Accurately Calculated

Retirement funds can be expressed with the following formula:

(1) Annual Living Expenses × (2) Number of Retirement Years

These two elements determine the total, but neither (1) nor (2) can be calculated easily.

—

(1) Annual Living Expenses

This is not at all easy to estimate.

There was a survey conducted asking how much people think they would need for retirement.

For a couple, the minimum daily living expenses in retirement looked like this:

(Source: [https://www.jili.or.jp/lifeplan/lifesecurity/1141.html](https://www.jili.or.jp/lifeplan/lifesecurity/1141.html))

The survey found that on average, couples needed 232,000 yen per month.

But this 232,000 yen per month is only for minimum daily living costs.

When it comes to a more comfortable retirement, the numbers looked like this:

(Source: [https://www.jili.or.jp/lifeplan/lifesecurity/1141.html](https://www.jili.or.jp/lifeplan/lifesecurity/1141.html))

For a couple, a comfortable and fulfilling retirement was said to require 379,000 yen per month.

Many respondents gave this answer in the survey.

Interestingly, whether talking about minimum or comfortable living expenses, more than 20% of respondents answered “I don’t know.”

—

Seeing these results, some people might think:

“Alright, let’s aim for a comfortable retirement!”

And then calculate:

361,000 yen × 12 months = 4,332,000 yen per year.

But to those people, I’d say: “Wait a moment.”

If you just assume you’ll need 4.33 million yen every year and try to save for the number of years you expect to live, I’d again say: “Hold on.”

Why? Because to me, that 4.33 million yen figure is highly questionable.

—

Why It’s Questionable

There are multiple factors that make future expenses hard to predict, such as:

Fluctuations in prices (inflation/deflation)

Changes in lifestyle

Changes in health condition

Changes in living environment over time

For example, the average household communication cost was:

6,200 yen in 1989 (Heisei 1)

Over 13,000 yen in 2018 (Heisei 30)

It more than doubled in 30 years.

Could anyone back in 1989 have predicted this? That’s the point.

There are many other expenses that have changed drastically over the years as well.

—

The Problem with “Averages”

This 4.3 million yen figure also has another issue.

Is the amount you personally need really the same as the average?

Imagine a world with only two people:

Person A, height 160 cm

Person B, height 180 cm

The average height in this world would be 170 cm.

But in reality, no one is 170 cm.

So in that sense, an “average” is almost an illusion.

The same applies to household spending.

There is no such thing as an “average household.”

So how meaningful is it to plan your finances strictly based on averages?

That is the question.

—

And this is the first challenge: (1) Annual Living Expenses.

They are extremely difficult to calculate.

Special Thanks OpenAI and Perplexity AI, Inc