管理人オススメコンテンツはこちら

「盲信したらダメ|“知らぬが仏、知らずに地獄” 保険商品はなぜ複雑なのか?」

〜前回のつづき〜

●保険会社の役割とは?

理由(1)

商品選びが難しい(つづき)

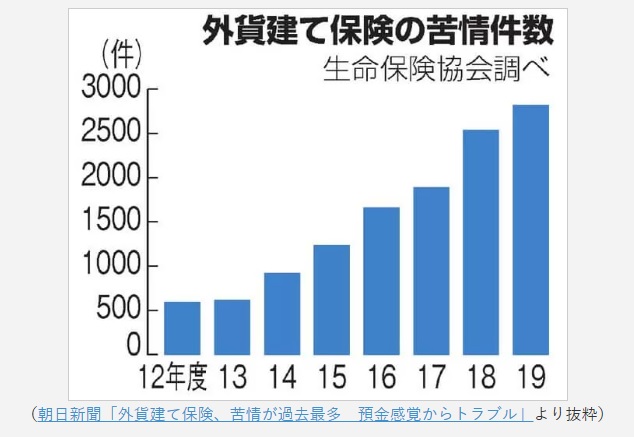

外貨建て保険・年金の新契約に関する

トラブルは前年度比12.3%増で

(5年前の約3.3倍)

苦情発生率は

普通の保険に比べて2倍以上

2019年度の

『外貨建て保険・年金』の

苦情件数は2,822件

という事で

(出典:リベラルアーツ大学)

こんな感じになってますけどね。

そして苦情内容の80%近くが

『説明不十分』なんですよ。

十分な説明を受けられずに

誤解したまま契約してる人が

たくさんいるという事です。

❎元本割れの可能性が有るという事を知らない

❎為替変動のリスクを良くわかってない

❎中途解約時の取扱い

どれぐらいお金が減っちゃうのか

❎各種の手数料

・契約初期費用

・維持手数料

・為替手数料

など

❎解約時の税金

❎特約の有無と内容

そういったものを

良く理解せずに

契約してしまってる。

『物事を複雑にすればするほど儲かる』

という言葉が

投資の世界には有ります。

「難しくて良くわからないけど

きっとお得なんだろう!

もう任せちゃおう!」

とお客さんに思わせたら

保険会社の勝ちなんですね。

だから

盲信したらダメなんですよ。

考える事をやめちゃ

ダメなんです。

まさに

こう思わせる為の商品が

本当に溢れてるんですね。

保険会社の

・A社

・B社

・C社

が有ったとして

例えば

死亡保証が1千万円のみで

「もしも

亡くなってしまった場合に

1千万円出ますよ」

というだけの

超シンプルな保険を

作ったとしたら

同じ保障内容で

同じ1千万円

出るだけなんだから

あなたは単純に

1番保険料が安い保険を選んで

加入すると思いませんか?

保障内容が全く一緒で

もし亡くなった時に

1千万円出るという

超シンプルな保険。

では掛け金が

・A社が月々2千円

・B社が月々千円

・C社が月々5百円

という事であれば

非常に選びやすいですよね?

同じ保障内容だったら

C社でいいよとなると

思うんですけど

保険会社というのは

比較を簡単にされないように

・微妙に

・ちょっとずつ

他社と違う保険を開発して

わざと複雑にしてるんですね。

複雑にしてるというところが

またポイントなんですね。

各社の保険の内容というのを

完璧に把握するのは

もはやプロでも難しいんですよ。

だから

保険のプロだと言ってる人達でも

他社の保険について

完璧に理解してる人というのは

まぁなかなかいないですね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

保険会社の商品は一見すると魅力的に見えますが、実際には非常に複雑で理解しにくい構造になっています。

特に外貨建て保険や年金ではトラブルが急増しており、2019年度には約2,800件もの苦情が寄せられ、その8割が「説明不足」に起因しています。

多くの人が、元本割れや為替変動リスク、中途解約の返戻金減少、各種手数料、税金、特約の内容などを十分理解しないまま契約してしまうのです。

本来、死亡保障1,000万円などシンプルな内容であれば、各社の保険料を比較し安いものを選ぶだけで済みます。

しかし実際の保険は、各社が条件を少しずつ変えて複雑化し、単純比較できないように設計されています。

そのためプロでさえ他社の商品を完璧に把握するのは困難です。

つまり、消費者は「よく分からないから任せよう」と盲信してはいけません。複雑さの裏にあるリスクを理解し、自ら考える姿勢が不可欠なのです。

- https://moneiro.jp/media/article/foreign-currency

- https://www.kokusen.go.jp/soudan_topics/data/seiho.html

- https://www.behavior.co.jp/blog/foreign-currency-insurance-2025

- https://www.taiju-life.co.jp/corporate/news/info2.htm

- https://www.sonylife.co.jp/media/manavi/4/

- https://www.seiho.or.jp/member/complaint/

- https://www.jili.or.jp/research/report/9849.html

- https://www.sonylife.co.jp/company/cs/data.html

≪≪Chat-GPTくんによる英訳≫≫

〜Continuation from last time〜

【What is the role of insurance companies?】

Reason (1)

Choosing a product is difficult (continued)

Troubles related to new contracts of foreign-currency-denominated insurance and pensions increased by 12.3% compared to the previous year

(about 3.3 times higher than five years ago)

The complaint rate is more than twice that of ordinary insurance.

In fiscal year 2019, the number of complaints about “foreign-currency-denominated insurance and pensions” was 2,822 cases.

(Source: Liberal Arts University)

That’s the current situation.

And nearly 80% of the complaints were due to “insufficient explanation.”

This means many people are entering contracts without receiving adequate explanations, leading to misunderstandings.

❎ They don’t know there’s a possibility of capital loss.

❎ They don’t fully understand the risk of currency fluctuations.

❎ They aren’t aware of how much money they might lose when canceling mid-term.

❎ Various fees:

Initial contract fees

Maintenance fees

Currency exchange fees

❎ Taxes upon cancellation

❎ The existence and details of riders (optional provisions)

People are signing contracts without properly understanding these points.

There is a saying in the investment world:

“The more complicated you make things, the more money you can make.”

If customers start thinking,

“It’s complicated and I don’t really understand it, but it must be a good deal! I’ll just leave it to them!”

—then the insurance company wins.

That’s why you must not blindly trust.

You must not stop thinking.

And in fact, there are countless products out there designed specifically to make you think this way.

Suppose there are three insurance companies:

Company A

Company B

Company C

For example, let’s say they all offer a super-simple life insurance policy that only provides a 10 million yen death benefit.

“If you pass away, your family will receive 10 million yen.”

That’s it—nothing more.

Since the coverage is exactly the same (a 10 million yen payout upon death), wouldn’t you simply choose the company with the lowest premium?

Let’s say the premiums are:

Company A: ¥2,000 per month

Company B: ¥1,000 per month

Company C: ¥500 per month

That would make it extremely easy to decide, right?

If the coverage is identical, you’d naturally think, “Company C is fine.”

But insurance companies don’t want to make it that easy to compare.

So they:

Subtly,

Little by little,

develop policies that differ from other companies, making things more complicated.

And the fact that they make things complicated—this is another key point.

At this level, it becomes difficult even for professionals to fully grasp the details of each company’s products.

That’s why, even among so-called “insurance professionals,” it’s quite rare to find someone who perfectly understands other companies’ policies.

Special Thanks OpenAI and Perplexity AI, Inc