管理人オススメコンテンツはこちら

「銀行が貸してくれないから|その高利回り本当に安全?裏に潜む地雷とは」

〜前回のつづき〜

●ソーシャルレンディングのヤバいポイント(つづき)

ヤバいポイント(2):投資先のリスクもめちゃくちゃ高い

貸し出し先のリスクが

めちゃくちゃ高いんですよ。

仮に不正をやってなかったとしても

貸し出し先のリスクがめちゃくちゃ高い。

このソーシャルレンディングの

投資対象になっている中小企業

お金を最終的に貸す貸出先の企業というのは

なぜこんな高金利で個人投資家から

お金を借りないといけないのか?

銀行が超低金利で今は

お金を貸してくれる時代ですよ。

ちょっといい企業であれば1%未満とか

すごく低金利でお金を貸してくれる訳ですよ。

中小企業でも十分1%台で

お金を借りる事ができるような

時代なのに

なぜ7〜8%とかそんな金利で

お金を借りないといけないのか?

答えは簡単です。

銀行が貸してくれないからです。

なぜ融資のプロである銀行が

お金を貸せないような投資先に

銀行よりもお金に余裕の無い

個人投資家が貸せると思うのか?

という事なんですね。

個人投資家には

融資先を調査するような

専門性も無い訳ですしね。

なのでこういう状況なんです。

世の中にはお金を借りる企業を

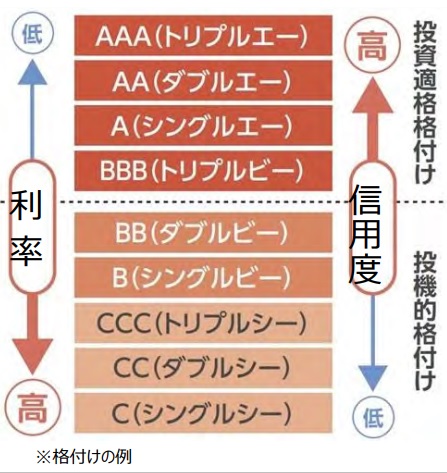

格付けしてる会社が有るんですね。

(出典:https://www.shiruporuto.jp/public/document/container/daigaku_kogi/pdf/kogi009.pdf)

格付けの例はこんな感じで

AAAが一番上なんですけど

BBBまでが一応投資的確と言われてて

ギリギリこの辺までだったら

お金を貸して投資出来るよね

投資対象になり得るよねという話になってて

BBB未満というのは『投機的格付け』

つまりギャンブル性が高くて

プロ向けという扱いなんですね。

例えば

株式会社日本格付研究所(JCR)の

ホームページによると

・独立行政法人日本学生支援機構

・東京地下鉄株式会社

・NTTデータ

こういう会社なんかは

AAAなんですね。

・カプコン

・ソフトバンク

・グリー

のような有名企業ですよね。

こういう有名企業でさえ

ギリギリBBBなんですね。

大体感覚掴めますか?

こんな有名な企業でも

このぐらいの格付けなんですよ。

BBBでさえ統計上は

1年以内に0.5%はデフォルトする。

借金が返せない状態になるんですね。

だから200社有ったら1社ぐらいは

借金が返せないような状態になる。

これがシングルBであれば

1年以内に20%はデフォルトする。

すなわち

借金が返せない状態になっちゃうという

そんな感じの格付けの状態なんですね。

ソーシャルレンディングの投資先というのは

銀行からお金を借りられないような

零細事業者ですよ。

貸し倒れすなわち

お金が返ってこないという事が

起きない訳が無いんですよ。

だから明らかに

初心者向けの投資じゃないんですね。

なのでこの2つの理由から

このソーシャルレンディングは

かなりヤバいんだという事です。

これがわからない状態で

利回りにばっかり目を奪われて

お金を預けてる人ってかなり多いですよね?

だから気をつけましょう。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

ソーシャルレンディングの大きなリスクは、投資先となる企業の信用力が非常に低い点にあります。

銀行が超低金利で融資する時代にもかかわらず、ソーシャルレンディングを利用する企業は、銀行からお金を借りられない、つまりリスクが高いと判断された事業者が多いのです。

個人投資家は専門的な審査能力を持たず、貸し倒れの危険性を正確に見抜くことが困難です。

実際、信用格付けで「投資適格」とされるBBB格でも0.5%が1年以内にデフォルトし、さらに低い格付けでは20%もの高確率で返済不能になります。

ソーシャルレンディングの投資先はこうしたリスクの高い企業が多いため、利回りの高さだけに惹かれて投資するのは非常に危険です。

リスクを十分に理解し、慎重な判断が求められます。

Citations:

[1] https://www.bankers.co.jp/news/detail.html?page=risk-social-lending2

[2] https://kumo-funding.com/qa/sl2.html

[3] https://www.bluebox.co.jp/colum/realestate-investment/crowdfunding/sociallending-beginner/

[4] https://ja.komoju.com/blog/fintech/social-lending/

[5] https://www.extend-ma.co.jp/financing-next/

[6] https://klikandpay.co.jp/invest/social-lending-risk/

[7] https://assist-all.co.jp/finance/social-lending-not-recommend/

[8] https://www.bluebox.co.jp/colum/realestate-investment/crowdfunding/social-lending-ranking/

[9] https://my-best.com/24628

[10] https://www.fsa.go.jp/ordinary/social-lending/index.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous section ~

【The Risky Points of Social Lending (continued)】

Risky Point (2): The investment targets are extremely risky

The companies receiving the loans in social lending are extremely high-risk.

Even if there’s no fraud involved, the risk level of these borrowers is still very high.

These are the small and medium-sized enterprises (SMEs) that are the investment targets in social lending.

Why do these companies, the ones ultimately borrowing the money, have to borrow from individual investors at such high interest rates?

We live in a time when banks are offering loans at ultra-low interest rates.

A reasonably good company can borrow money at less than 1% interest.

Even many SMEs can secure financing in the 1% range nowadays.

So why do some companies have to borrow at 7–8% interest?

The answer is simple:

Because banks won’t lend to them.

So then, why would individual investors, who generally have less capital than banks, lend money to companies that even professional banks refuse to finance?

Individual investors lack the expertise to properly evaluate lending risk.

That’s the reality here.

There are companies in the world that assign credit ratings to businesses.

Credit ratings are ranked like this:

AAA is the highest,

BBB is still considered “investment grade”, meaning it’s just barely acceptable for investment.

Anything below BBB is classified as “speculative grade,” meaning it’s highly risky and intended for professionals.

For example, according to the website of Japan Credit Rating Agency (JCR):

Japan Student Services Organization (JASSO)

Tokyo Metro Co., Ltd.

NTT Data Corporation

These are AAA-rated companies.

Then you have well-known companies like:

Capcom

SoftBank

GREE

Even these famous companies are barely rated at BBB.

Do you get the picture?

Even these well-known companies only have about that level of creditworthiness.

Statistically speaking, even with a BBB rating, there’s a 0.5% chance of default within a year.

That means the company becomes unable to repay its debt.

In a pool of 200 such companies, about one is likely to default.

If the company is rated single B, the one-year default rate jumps to 20%.

In other words, the chance of being unable to repay debt becomes dramatically higher at that level.

The typical investment targets in social lending are very small businesses that can’t even borrow from banks.

Loan defaults — meaning you don’t get your money back — are virtually guaranteed to happen.

So clearly, this is not an investment suitable for beginners.

For these two reasons, social lending is extremely risky.

Many people invest their money just focusing on the attractive returns, without understanding the risks.

So be careful.

Special Thanks OpenAI and Perplexity AI, Inc