管理人オススメコンテンツはこちら

「闇が深い|“安心”の仮面を被った金融詐欺の温床」

〜前回のつづき〜

●ソーシャルレンディングのヤバいポイント(つづき)

嘘をついてファンドを募集して

↓

投資家から集めた資金を親会社に貸しちゃって

↓

資産運用したふりをして自転車操業する

という不正やりたい放題ですよね。

2017年7月に

2回目の業務停止処分を

受けてるんですよ。

2019年12月現在

みんなのクレジットの

公式ホームページは

こうなっちゃったんですよ。

↓

投資家から

45億円もの大金を集めてた企業が

これですよ。

ちなみにこの

『みんなのクレジット』という

ソーシャルレンディングなんですけど

口座を開設させると

紹介料1万円とかそれ以上とか

もらえたんですよ。

だから2017年当時

・ブロガー

・アフィリエイター

・インフルエンサー

なんかは

アフィリ報酬1万円もらえるので

他人に紹介しまくってたんですよ。

闇が深いですよね。

7〜8%という利回りが有れば

インフルエンサーから勧めらると

みんな開設するし

口座を開設する分には

お金はかからないから

ある意味紹介しやすいんですよね。

だけど潰れてしまった。

今も急にこの

ソーシャルレンディングというのを

勧めまくっている

・ブロガー

・Youtuber

・インフルエンサー

なんかがいると思うんですけど

そういったメディアが

増えてきてるのでご注意を。

このソーシャルレンディングというのは

定期的に問題になってますからね。

この『みんなのクレジット』だけじゃなくて

他の会社も不正しまくってるんですけど

あまり詳しく説明すると

長くなりすぎてしまうので簡単に。

不正の内容は

どこも似たような感じですね。

(出典:https://www.maneo.jp/)

『maneo(マネオ)』という

ソーシャルレンディング会社が

有ったんですけど

1600億円以上集めた

ソーシャルレンディングの

最大手なんですね。

ファンド募集の際に

虚偽表示をしてて

2018年7月に業務改善命令されて

社長は退任するわ

ファンド募集するわの大騒ぎで

今も募集停止中なんですよ。

業界の最大手でも

このレベルですよ。

(出典:https://www.lucky-bank.jp/)

他にも

『ラッキーバンク』という所が有って

雑誌なんかにも良く載ってたんですよ。

150億円も集めた

大手のソーシャルレンディング業者で

ファンド募集の際に

重大な誤解を表示させる表記をしており

2018年3月に行政処分を受ける。

2019年3月に

金融商品取引業の登録取消しを受けて

免許取消しとなりました。

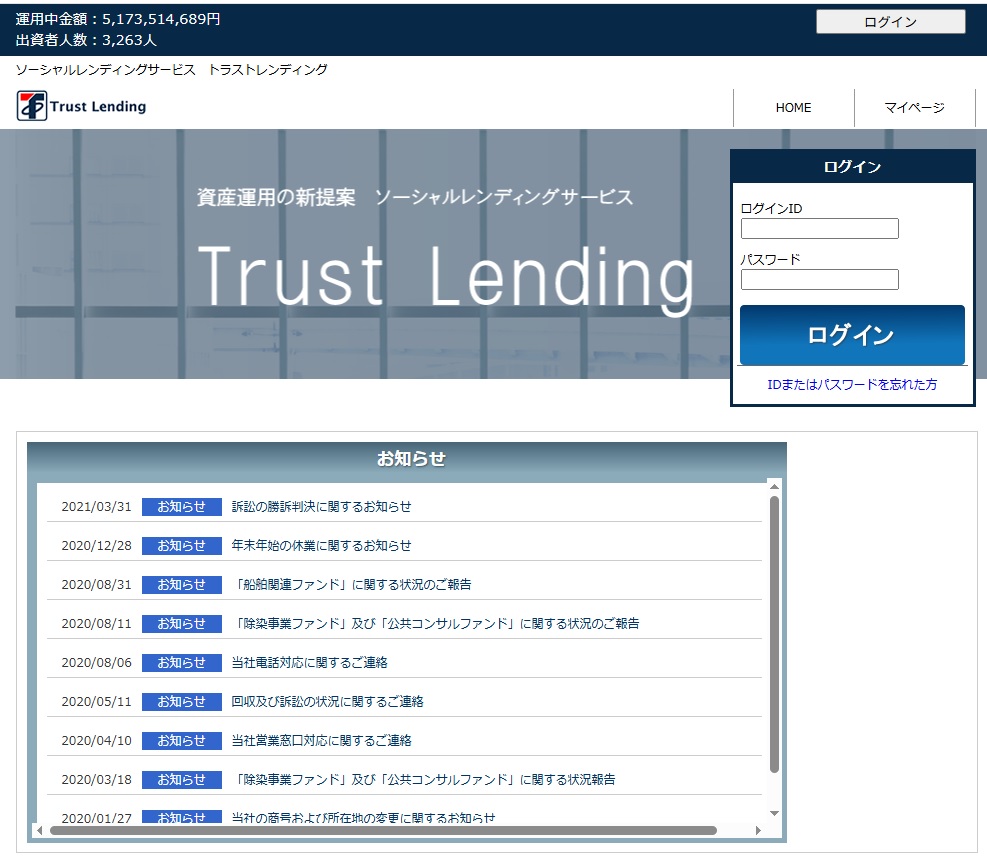

(出典:https://www.trust-lending.net/)

それから

『トラストレンディング』ですね。

83億円を集めた

中堅ソーシャルレンディング業者で

これも一緒ですね。

ファンド募集の際に虚偽表示をして

2018年12月に業務停止命令

2019年3月に同じく

免許取消しになってます。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

ソーシャルレンディング業界では、投資家から集めた資金を本来の目的以外に流用したり、虚偽の情報でファンドを募集するなどの不正が多発しています。

例えば「みんなのクレジット」では、集めた資金を親会社に貸し付けて自転車操業を行い、最終的に業務停止や事業停止に追い込まれました。

また、最大手の「maneo」や「ラッキーバンク」、「トラストレンディング」なども、虚偽表示や不適切な運用で行政処分や免許取消しを受けています。

高い利回りや紹介報酬につられ、インフルエンサーやブロガーによる勧誘も盛んでしたが、結果的に多くの投資家が損失を被りました。

今も同様の勧誘が続いているため、十分な注意が必要です。

Citations:

[1] https://www.crowdfundingchannel.jp/article-investment-fudosan-sl-incident-history/

[2] https://gokuraku.io/library/minnano-credit/

[3] https://gokuraku.io/library/luckybank-incident/

[4] https://gokuraku.io/library/trustlending-incident/

[5] https://assist-all.co.jp/finance/social-lending-not-recommend/

[6] https://gokuraku.io/library/crowdfunding-administrative-action/

[7] https://riskmanagement.media/articles/367

[8] https://www.tsr-net.co.jp/data/detail/1188845_1527.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from Last Time~

【The Alarming Aspects of Social Lending (continued)】

They lied to attract investors to their funds

↓

Then lent the collected money to their parent company

↓

Pretended to manage assets, but in reality just kept the operation afloat like a Ponzi scheme

It’s blatant and unchecked fraud.

In July 2017,

they received a second business suspension order.

As of December 2019,

the official website of Minna no Credit

ended up like this:

↓

A company that raised 4.5 billion yen (approx. \$40 million)

from investors… and this is what it came to.

By the way, this company,

Minna no Credit, was a social lending platform.

They offered over 10,000 yen (\$90+) in referral fees

just for getting someone to open an account.

So back in 2017,

you had:

Bloggers

Affiliates

Influencers

promoting it like crazy

because they could earn those referral fees.

It’s pretty dark when you think about it.

With advertised returns of 7–8%,

people easily signed up when recommended by influencers.

And since there was no cost to open an account,

it made it even easier to promote.

But in the end, the company collapsed.

Even now, there are still:

Bloggers

YouTubers

Influencers

suddenly pushing social lending.

With more of these types of media popping up,

you should really be cautious.

This social lending industry

keeps running into scandals on a regular basis.

It’s not just Minna no Credit—

other companies have been heavily involved in misconduct too.

Let’s keep it brief to avoid getting too long,

but the kind of fraud is very similar across the board.

(Source: [https://www.maneo.jp/](https://www.maneo.jp/))

There was a company called maneo,

another social lending platform.

They raised over 160 billion yen (approx. \$1.5 billion)—

the largest in the industry.

But they used false representations when soliciting funds

and received a business improvement order in July 2018.

The CEO resigned,

and there was a huge commotion about fund solicitation.

Even now, they are still not accepting new funds.

Even the biggest player in the market

was at this level of trouble.

Another one was Lucky Bank,

which used to be featured frequently in magazines.

They raised 15 billion yen (approx. \$135 million),

but made seriously misleading statements when raising funds.

They were administratively sanctioned in March 2018,

and had their financial license revoked in March 2019.

And then there’s Trust Lending.

They raised 8.3 billion yen (approx. \$75 million),

a mid-sized social lending company—

but again, the same pattern.

They made false representations during fund solicitation,

received a business suspension order in December 2018,

and had their license revoked in March 2019.

Special Thanks OpenAI and Perplexity AI, Inc