管理人オススメコンテンツはこちら

「生活のレベルを上げてはいけない|年収アップの罠!稼ぐほど減る手取りの真実」

〜前回のつづき〜

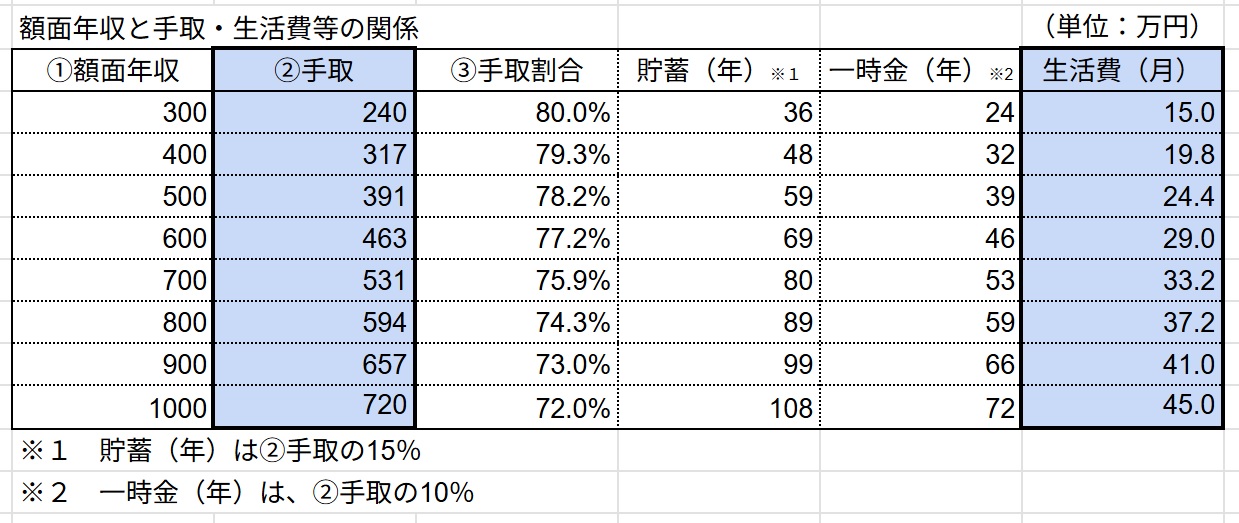

●年収・手取り・生活費の関係からわかった事5つ

年収300万円〜1千万円の

手取り&生活費をまとめてみると

↓こんな感じです。

ここからわかる事について

お話ししていきます。

・額面

・年収

・生活費(月間)

の関係からわかった事ですが

その(1)100万円稼ぐたびに約1%ずつ手取り率が悪化

累進課税制度の影響で

日本というのは稼げば稼ぐほど

税金で持っていかれるんですね。

年収300万円の時は

手取率が80%有って

60万円が社会保険料と税金です。

これでも高いんですけどね。

週に5日働くうち1日は

税金で消えてるという事ですよ。

年収1千万円になると

手取率が72%まで悪化する。

これが累進課税ですね。

なんと280万円

社会保険料と税金に払ってる事に

なるんですよ。

週5日働くうち1.4日は

税金の為に働いている

という事になるんですね。

3.5日分しか

自分のものにならないという事ですね。

その(2)貯蓄率を固定すると全然貯まらない

一般に適正な理想の貯蓄率というのは

15〜20%程度と言われています。

年収300万円の時の貯蓄率15%は

結構頑張ってると思います。

月15万円で生活しながら

年間36万円貯金するとなると

結構頑張ってるという事になるんですけど

一方で年収1千万円の時の

貯蓄率15%というのは

大分物足りない感じなんですよね。

年間108万円しか貯められてない。

年収500万円ぐらいの家計でも

年間100万円貯めてる家庭も結構有る。

結局大事なのは

稼いだら稼いだ分だけ

生活水準を上げてるという生活をすると

結局こうなっちゃう

という事なんですよ。

だから

もし貯蓄がしたいのであれば

固定すべきは貯蓄率じゃなくて

生活費の金額なんですね。

いくら収入が上がろうと

生活のレベルを上げてはいけない

という事です。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

年収と手取り、生活費の関係をまとめると、まず累進課税制度の影響で年収が上がるほど手取り率は下がります。例えば、年収300万円の場合は手取り率が約80%ですが、年収1,000万円になると約72%まで下がり、税金や社会保険料の負担が大きくなります。

次に、理想的な貯蓄率を15~20%とした場合でも、年収が増えるにつれて生活水準を上げてしまうと、貯蓄額は思ったほど増えません。年収1,000万円でも貯蓄率15%だと年間108万円しか貯まらず、年収500万円の家庭と大差がないこともあります。

結局、収入が増えても生活費を増やさず一定に保つことが、貯蓄を効率的に増やすためのポイントだと言えます。

Citations:

[1] https://tenshoku.mynavi.jp/knowhow/money/16/

[2] https://www.musashi-corporation.com/wealthhack/annual-income-net-income

[3] https://www.orixbank.co.jp/column/article/175/

[4] https://talentsquare.co.jp/career/annual-income-300-man-yen/

[5] https://mynavi-agent.jp/dainishinsotsu/canvas/2024/08/post-1335.html

[6] https://studyfire.jp/?c=simulation%2Fincome_table

[7] https://biz.moneyforward.com/payroll/basic/50743/

[8] https://www.renosy.com/magazine/entries/5299

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous post~

【5 Insights from the Relationship Between Annual Income, Take-Home Pay, and Living Expenses】

After summarizing the take-home pay and living expenses for annual incomes ranging from 3 million to 10 million yen, here’s what we found:

Let’s talk about what we can learn from the relationship between:

Gross income

Annual income

Monthly living expenses

—

(1) For every additional 1 million yen earned, the take-home pay rate decreases by about 1%

Due to Japan’s progressive tax system, the more you earn, the more you lose to taxes and social insurance.

For example, at an annual income of 3 million yen, the take-home pay rate is around 80%, meaning about 600,000 yen goes to taxes and social insurance.

Even that is quite a lot.

Basically, one out of every five working days in a week goes entirely to taxes.

When your annual income reaches 10 million yen, the take-home rate drops to about 72%.

That’s the effect of the progressive tax system.

You’re paying about 2.8 million yen in taxes and social insurance.

That means you’re working 1.4 days a week just for taxes.

In other words, only 3.5 out of 5 workdays are actually earning you money.

—

(2) If you fix your savings rate, you won’t actually save much

Generally, the ideal savings rate is said to be around 15–20%.

At an income of 3 million yen, saving 15% is already a strong effort.

If you live on 150,000 yen per month and still save 360,000 yen a year, that’s a significant achievement.

However, if you earn 10 million yen a year and only save 15%, it feels quite underwhelming.

That’s only 1.08 million yen in annual savings.

Even households with a 5 million yen income can often save 1 million yen a year.

In the end, what really matters is this:

If you raise your standard of living every time your income increases, you’ll end up not saving much at all.

So, if you really want to save money, what you should fix is not the savings rate—

But the amount of your living expenses.

No matter how much your income increases, you shouldn’t raise your standard of living.

Special Thanks OpenAI and Perplexity AI, Inc