管理人オススメコンテンツはこちら

「本当に人生が変わります|保険とマイホームは罠!? 本当に得する節税はこれだ!」

〜前回のつづき〜

●まとめ

まず今回のお話しで大事なのは

節税の重要性を知るという事です。

サラリーマンでも出来る

本当に効果の有る節税ベスト6 は

こちらです。

↓

定年までにトータルで

2,000万円近くの控除が受けられます。

生涯賃金 2.5億円と言われている内

20%に当たる5千万円

0.5億円は社会保険や税金なんですね。

今日は

強引なシミュレーションも

したんですけど

趣旨としてはとにかく

節税の重要性というのを

知って欲しいんですよ。

税の負担というのは

非常に重たいです。

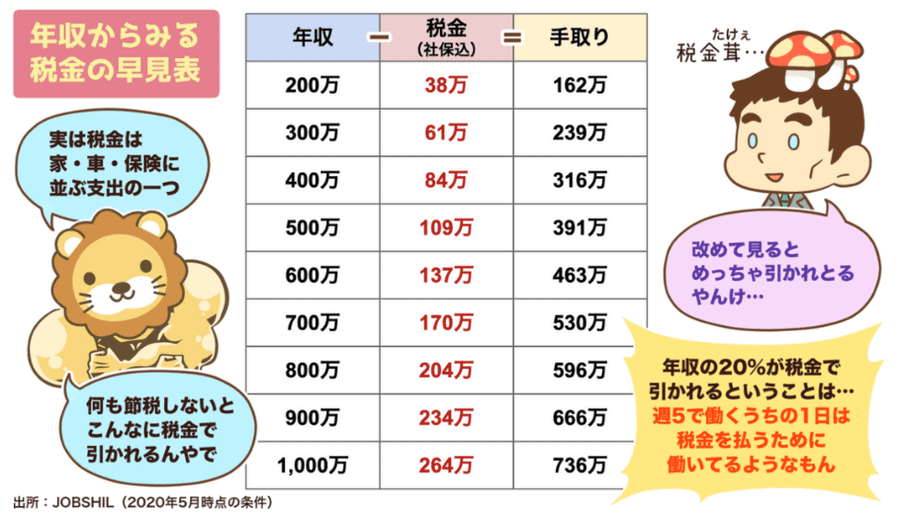

(出典:リベラルアーツ大学)

年収300万円の人だったら

税金が61万円ぐらい取られている。

こういう表が有るんですけど

自分の年収を当てはめてみて下さい。

ここで税金は赤色の字の

大体これぐらいの金額を取られている

という事を押さえる事が出来たら

これだけ手取りが上がる訳ですよ。

なのでここを抑える方法を

覚えていきましょう。

・保険料控除

・住宅ローン控除

というのは

・ぼったくり保険

・資産価値の低いマイホーム

こういったものが有るから

使い方が多少難しいんですよ。

かなり使いこなせる人じゃないと

非常に難しい。

わざわざ節税のために

入る価値の有る保険って

基本的にありません。

住宅ローンも

いい家に出会えるのであれば

いいんですけど

なかなか見つけられないので

そういう意味では

難しいんですね。

・iDeCo

・NISA

・ふるさと納税

というのは

これは基本的には

誰にでもおすすめ出来る。

ただこれだけだったら

パワー不足なんです。

やはり青色申告が最強なんですね。

・NISA

・ふるさと納税

・青色申告

この3つをやるだけで

98点ぐらいは取れてると思うので

やはり青色申告をやって欲しいです。

青色申告だけで

大体90点ぐらいの価値が有ると

個人的には思っています。

なので青色申告を

頑張って欲しいです。

興味があれば

是非チャレンジして欲しいですね。

本当に人生が変わります。

節税の知識を身につけて

今よりも一歩自由を

目指していきましょう!

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

今回の話の要点は「節税の重要性を知ること」です。

サラリーマンでも実践できる効果的な節税方法として、青色申告、ふるさと納税、NISA、iDeCo、住宅ローン控除、保険料控除の6つが挙げられます。特に青色申告は節税効果が非常に高く、これだけでも大きなメリットがあります。一方、保険料控除や住宅ローン控除は商品や物件選びが難しく、誰にでもおすすめできるわけではありません。iDeCoやNISA、ふるさと納税は比較的取り組みやすく、基本的には多くの人におすすめです。

生涯賃金の約20%が税金や社会保険料で消えるため、節税を意識することで手取りが大きく変わります。節税の知識を身につけ、自由な生活を目指しましょう。

Citations:

[1] https://liv-plus.jp/column/6tax-saving-for-salariedworkers/

[2] https://nature-inter.com/lounge/8196

[3] https://www.cpa-learning.com/column/keiri/tax-advantage/

[4] https://president.jp/articles/-/433?page=1

[5] https://www.musashi-corporation.com/wealthhack/tax-measures

[6] https://www.ht-tax.or.jp/kigyou-guide/annual-income-tax

[7] https://www.orixbank.co.jp/column/article/116/

[8] https://o-uccino.com/front/articles/61353

[9] https://jobtalk.jp/jobshil/295

[10] https://nature-inter.com/lounge/8494

[11] https://www.rakuten-card.co.jp/minna-money/feature/article_2110_00003/

[12] https://www.ht-tax.or.jp/kigyou-guide/save_taxes_by_establishing_a_company

[13] https://detail.chiebukuro.yahoo.co.jp/qa/question_detail/q14314002729

[14] https://financial-field.com/pension/entry-180449

[15] https://ameblo.jp/settetsu/entry-12342474784.html

[16] https://www.smbc-card.com/nyukai/magazine/tips/life-earnings.jsp

≪≪Chat-GPTくんによる英訳≫≫

~Continuing from the previous part~

【Summary】

The key takeaway from today’s discussion is understanding the importance of tax-saving strategies.

Even salaried workers can benefit from six truly effective tax-saving methods, which are as follows:

↓

You can receive tax deductions totaling nearly 20 million yen by retirement.

Out of a typical lifetime income of 250 million yen, around 20%—which is 50 million yen—is lost to taxes and social insurance.

Today, we went through a bit of a forced simulation,

but the main point I want to emphasize is just how crucial tax-saving is.

The tax burden is extremely heavy.

(Source: Liberal Arts University)

For example, someone earning 3 million yen per year pays around 670,000 yen in taxes.

There are charts showing this—try plugging in your own income to see for yourself.

Once you understand how much of your income is taken as taxes (typically marked in red),

you’ll see how much your take-home pay could increase with the right strategies.

So, let’s learn how to reduce this burden.

Examples:

Insurance Premium Deductions

Mortgage Loan Deductions

However, these are tricky because of:

Overpriced insurance plans

Homes with low asset value

Unless you’re highly knowledgeable, these are difficult to take full advantage of.

Honestly, insurance products solely for tax-saving purposes usually aren’t worth it.

As for mortgage loans, they can be great if you find a truly good home,

but that’s not always easy—so it can be difficult in practice.

Recommended options:

iDeCo (individual-type defined contribution pension plan)

NISA (Nippon Individual Savings Account)

Furusato Nozei (hometown tax donation program)

These are generally suitable for almost anyone.

But relying on just these alone isn’t powerful enough.

Ultimately, the blue tax return (a.k.a. “blue return” or “blue form” filing) is the strongest method.

Just by doing these three:

NISA

Furusato Nozei

Blue Return Filing

You’re already scoring about 98 out of 100 in tax-saving efforts.

In fact, I personally believe blue return filing alone is worth about 90 points.

That’s why I really want you to give blue return filing a try.

If you’re interested, please challenge yourself to take this step.

It can truly change your life.

Let’s gain tax-saving knowledge and take one step closer to financial freedom!

Special Thanks OpenAI and Perplexity AI, Inc