管理人オススメコンテンツはこちら

「ルールが変わってきてる|資産増やす人は知っている!日本の金融リアル」

〜前回のつづき〜

●世論調査のデータで見る『世間一般』と『家計エリート』の違い(つづき)

(2)金融資産の内訳

・貯金 40〜50%

・保険 10〜20%

・有価証券 30〜40%

こんなイメージです。

貯金とか保険が大好きな日本人の傾向が

しっかり出てるのではないでしょうか?

今までのお話しの中で触れてきましたけど

保険で貯金というのは

もったいないなぁと思ういますが

今のところ

こんな感じのデータになっています。

貯金が全く無い世帯というのは

全体の3〜5%で

ちなみに

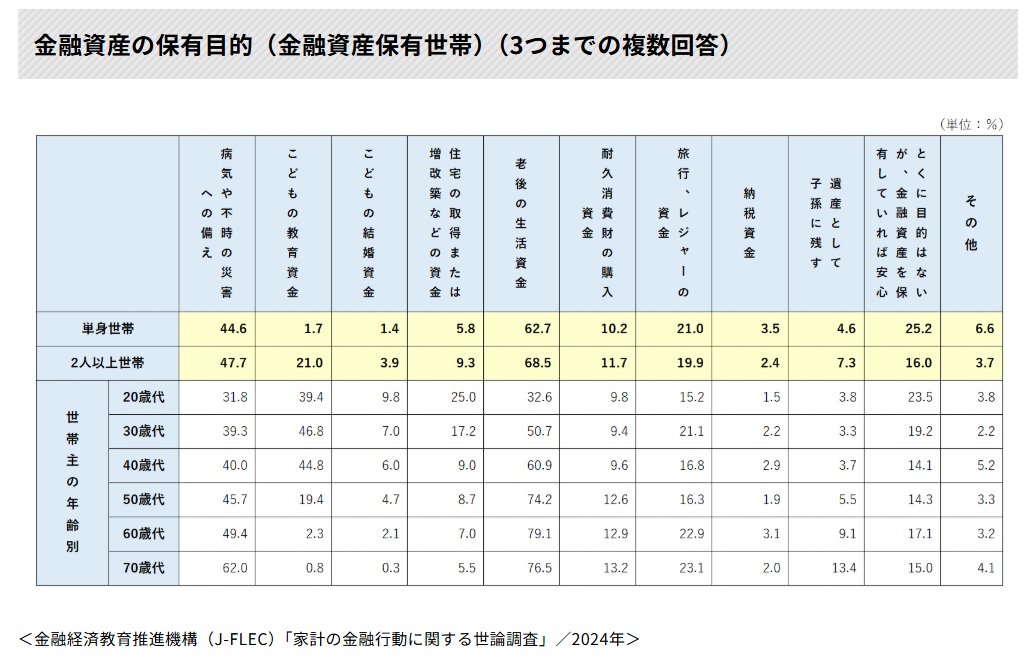

単身世帯の金融資産の保有目的は

こんな感じ。

(出典:https://www.jili.or.jp/lifeplan/houseeconomy/852.html)

「事業を起こすために

金融資産を保有してるんです!」

みたいな人はほぼいないですね。

みんな不安を抱えて

リスクに備えるために

金融資産を貯めている

というような

そんな感じの状況です。

なので

結論としては

・単身世帯の場合

貯金が941万円を超えてたら

家計エリートですね。

・2人以上の世帯の場合

貯金が1,307万円を超えていたら

家計エリートです。

(2)金融資産の増減状況

昨年と比較して

金融資産は増えたのか減ったのか

という事です。

単身世帯の場合は

.jpg)

(出典:https://www.shiruporuto.jp/public/document/container/yoron/tanshin/2023/pdf/yoront23.pdf)

・増えた:39.6%

・減った:19.9%

・変わらない:40.5%

2人以上の世帯の場合は

.jpg)

(出典:https://www.shiruporuto.jp/public/document/container/yoron/futari2021-/2023/pdf/yoronf23.pdf)

・増えた:37.0%

・減った:20.9%

・変わらない:42.1%

去年と比較して

金融資産を増やす事が出来たという世帯は

2〜3割しかいないんですよね。

収入が減って

資産を取り崩してる人というのが

結構多いのではないでしょうか?

厳しい経済事情ですね。

株主は儲かってるんですけどね。

どういう事かというと

ルールが変わってきてるんですよ。

だからここのルールを

しっかり理解していかないといけないという

いつも話してる話ですね。

家計エリートは去年と比較して

金融資産を増やす事が出来た

という事になりますかね。

だから去年と比べて

金融資産を増やせたという人だけでも

上位2〜3割に入るという事ですね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

日本人の金融資産の内訳は、貯金が40〜50%、保険が10〜20%、有価証券が30〜40%と、貯金や保険を重視する傾向が強く表れています。

貯金が全くない世帯は3〜5%程度で、多くの人が将来の不安やリスクに備えて資産を保有しています。

単身世帯で貯金が941万円以上、2人以上の世帯で1,307万円以上あれば「家計エリート」とされますが、昨年と比べて金融資産を増やせた世帯は2〜3割しかありません。

収入減で資産を取り崩す世帯も多く、経済的に厳しい状況が続いています。

資産を増やせた人は全体の上位2〜3割に入り、家計管理や投資の重要性が高まっています。

Citations:

[1] https://gentosha-go.com/articles/-/54950

[2] https://www.orixbank.co.jp/column/article/310/

[3] https://japanknowledge.com/contents/nipponica/sample_koumoku.html?entryid=665

[4] https://toyokeizai.net/articles/-/725973

[5] https://www.nira.or.jp/paper/article/2024/wp10.html

[6] https://maneql.co.jp/blog/2019/08/21/global-elite/

≪≪Chat-GPTくんによる英訳≫≫

~Continuing from the previous discussion~

【The Difference Between the “General Public” and the “Household Elites” According to Survey Data (continued)】

(2) Breakdown of Financial Assets

– Savings: 40–50%

– Insurance: 10–20%

– Securities: 30–40%

This is the general picture.

You can clearly see the typical Japanese tendency to prefer savings and insurance.

As we’ve touched on before, I personally think saving money through insurance is a bit of a waste…

But for now, this is what the data looks like.

Households with absolutely no savings account for only about 3–5% of the total.

By the way, here’s the purpose of financial asset ownership for single-person households:

(Source: https://www.jili.or.jp/lifeplan/houseeconomy/852.html)

Very few people say,

“I’m saving up financial assets to start a business!”

Most people are anxious and are saving financial assets to prepare for risks.

That’s the current situation.

So, in conclusion:

For single-person households:

If you have over 9.41 million yen in savings, you’re considered a household elite.

-For households with two or more people:

If you have over 13.07 million yen in savings, you’re also in the household elite category.

—

(2) Change in Financial Assets

This section shows whether financial assets increased or decreased compared to the previous year.

For single-person households:

(Source: https://www.shiruporuto.jp/public/document/container/yoron/tanshin/2023/pdf/yoront23.pdf)

– Increased: 39.6%

– Decreased: 19.9%

– No change: 40.5%

For households with two or more people:

(Source: https://www.shiruporuto.jp/public/document/container/yoron/futari2021-/2023/pdf/yoronf23.pdf)

– Increased: 37.0%

– Decreased: 20.9%

– No change: 42.1%

Only about 20–30% of households were able to grow their financial assets compared to last year.

Quite a few people may be drawing down their assets due to decreased income.

It’s a tough economic environment.

Although shareholders seem to be doing well…

What that suggests is:

The rules are changing.

And as I always say, we need to understand these new rules properly.

In short, those who increased their financial assets compared to last year can be considered household elites.

So just being able to grow your financial assets from the previous year puts you in the top 20–30% of households.

Special Thanks OpenAI and Perplexity AI, Inc