管理人オススメコンテンツはこちら

「ただの手数料で消えてる|高額な手数料に要注意!賢い生命保険の選び方」

〜前回のつづき〜

●内訳を詳しく見てみよう(つづき)

(2)生命保険・医療保険

保険料には

a)純保険料

b)付加保険料

という内訳が有るんですね。

a)純保険料

保険金の支払いに充てるための保険料の事です。

b)付加保険料

保険会社の運営経費

・人件費

・オフィス代

・宣伝費

などに充てられる

保険会社の手数料の事です。

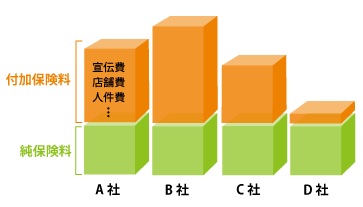

保険料の内訳のイメージは

どんな感じになってるかというと

(出典:https://www.f-l-p.co.jp/knowledge/5301)

付加保険料というのが

上のオレンジの部分

純保険料が下の緑の部分です。

この付加保険料と純保険料の比率は

どれぐらいかというと

会社や保険の種類によって違います。

だから各保険会社によって

割合は当然違うという事です。

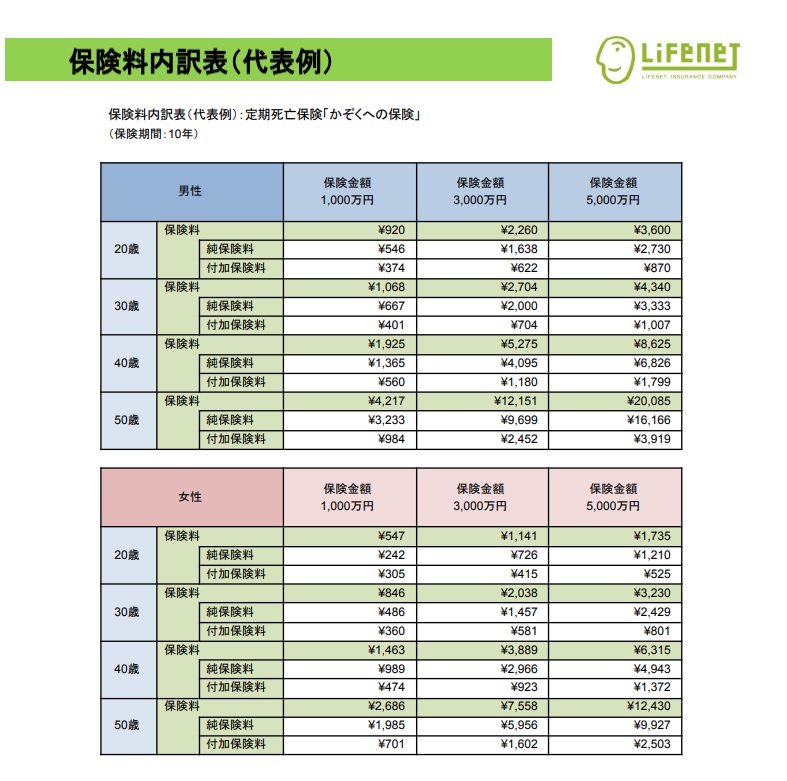

この内訳を公表しているというのが

(出典:https://www.lifenet-seimei.co.jp/shared/pdf/insurance_table_202404.pdf)

2024年4月の時点ですけど

ライフネット生命だけだったんです。

という事は

他の保険会社は内訳を出してないんですよね。

保険会社は内訳を知られたくないんですよね。

どのぐらい自分達の

・オフィス代

・人件費

その他もろもろ掛かっているか?

というのを知られたくない訳ですね。

なぜ知られたくないんでしょうねぇ・・・?

●保険は守り、投資は攻め~混ぜた瞬間にあなたがカモになる~

なぜ保険の手数料が高いのか?

a)純保険料

b)付加保険料

の比率を7:3とすると

あなたが支払ったうちの30%は

ただの手数料で消えてるという事です。

だからあなたが

月2万円の保険料を支払ったとすると

月6千円は

手数料で取られてるという事です。

30年でいくら取られるかというと

30年✕12ヶ月✕6千円

= 216万円

ということになります。

貯蓄性のある保険にしても

手数料を差っ引かれた分が

投資に回ったりするので

これまた利率が悪いんですね。

なんて言いますけど

安全な資産で回すにしても

同じ対象のものに投資するにしても

利回りが悪いんですよね。

だから

なぜ高いのかというと

ここの手数料を

ガッツリ取られてるからですよ。

だから

・保険は保険

・投資は投資

混ぜるなキケン!

なんです。

ずっと言い続けてるのは

ここですよね。

数字は仮ですが

わざわざ3割も

手数料を取られながら

投資をする必要ないですよね?

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

生命保険・医療保険の保険料は、主に「純保険料」と「付加保険料」という2つの要素で構成されています。

純保険料は、契約者が万が一のときの保険金支払いに充てられる部分で、予定死亡率や予定利率を基に算出されるため会社間の差はほとんどありません。

一方、付加保険料は保険会社の経営に必要な人件費・宣伝費・オフィス維持など運営経費で、会社ごとや商品種類によって大きく異なります。

たとえば、ライフネット生命ではこの内訳を公開しており、付加保険料の比率は全体の3〜4割になることもあります。

他の多くの保険会社は比率を公表しておらず、保険料の差の原因ともなっています。

- https://hoken-room.jp/word/7

- https://www.f-l-p.co.jp/knowledge/5301

- https://soudanguide.sonpo.or.jp/basic/2_1.html

- https://www.nissen-life.co.jp/willnavi/learn_insurance/learn_knowledge/knowledges/knowledge11.html

- https://www.meijiyasuda.co.jp/find2/light/knowledge/list/11.html

- https://www.giroj.or.jp/ratemaking/

- https://www.f-l-p.co.jp/knowledge/1760

- https://hoken-navi.docomo.ne.jp/dmg-ins/car/chishiki/hokenryo-02.html

- https://www.rakuten-life.co.jp/learn/article/fee/

- https://www.f-l-p.co.jp/knowledge/1760

- https://www.meijiyasuda.co.jp/find2/light/knowledge/list/11.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous post~

【Let’s take a closer look at the breakdown (continued)】

(2) Life Insurance & Medical Insurance

Insurance premiums are made up of two components:

a) Pure Premium

b) Loading Premium

—

a) Pure Premium

This is the portion of the premium that is actually allocated to pay insurance claims.

b) Loading Premium

This covers the insurance company’s operating costs, such as:

Employee salaries

Office expenses

Advertising costs

In other words, it’s the fee charged by the insurance company.

—

So what does the breakdown of insurance premiums typically look like?

(Source: [https://www.f-l-p.co.jp/knowledge/5301](https://www.f-l-p.co.jp/knowledge/5301))

The orange part above represents the loading premium

The green part below represents the pure premium

The ratio of loading to pure premiums varies depending on the company and the type of insurance.

So naturally, each insurance company has a different split.

—

Now, which companies actually disclose this breakdown?

(Source: [https://www.lifenet-seimei.co.jp/shared/pdf/insurance\_table\_202404.pdf](https://www.lifenet-seimei.co.jp/shared/pdf/insurance_table_202404.pdf))

As of April 2024, the only company publishing it was Lifenet Insurance.

Which means:

Other insurance companies don’t disclose their breakdown.

Why?

Because insurance companies don’t want you to know.

They don’t want you to see how much of your premium goes to:

Their office costs

Their staff salaries

…and everything else.

Why wouldn’t they want you to know? Hmm… 🤔

—

【Insurance is defense. Investment is offense.-Mix them, and you become the prey.】

—

So, why are insurance fees so high?

If we assume the ratio between:

a) Pure Premium

b) Loading Premium

is 7:3,

that means 30% of what you pay simply vanishes as fees.

—

For example:

If you’re paying 20,000 yen per month in insurance premiums,

6,000 yen of that is just fees.

Over 30 years, that adds up to:

30 years × 12 months × 6,000 yen = 2.16 million yen

—

Even with “savings-type” insurance,

those fees get deducted before the money is invested.

Which is why the returns are so poor.

—

> “We’re investing it safely.”

>

> “We’re putting it into stable assets.”

That’s what they say.

But even with the same safe assets,

the returns are worse.

—

So why are the fees so high?

Because they’re taking a huge chunk as commission.

—

That’s why:

Insurance should stay insurance

Investment should stay investment

Never mix them. Dangerous!

This is the point I’ve been emphasizing all along.

—

The numbers here are just an example,

but let’s be real—

why would you choose to invest after letting 30% of your money get eaten by fees?

Special Thanks OpenAI and Perplexity AI, Inc