管理人オススメコンテンツはこちら

「木を見て森を見ず|パート主婦のための賢い働き方おしえます」

今日は【貯める力】

パートや主婦が扶養範囲内で働くとき年収はいくらがお得?

というお話をします。

●“税”か“社保”かで運命が変わる~“扶養の盾”を使って、家族経営の節税戦略~

今日の質問は2件!

1人目

「パートさんが

配偶者扶養に入りながら

働ける限度額が

変更になったようです。

103万円、130万円の壁など

どのぐらい稼げば

最も扶養の範囲を

活かせるのでしょうか?」

2人目

「夫は会社員で

副業は実質私一人でやるのですが

扶養を抜けて稼ぐより

扶養範囲内でパートをしながら

夫の収入として

増やしていく方が

節税効果が高いと思うのですが

この方法は

通用するのでしょうか?」

とのこと。

実はこの話題は

以前もお話ししています。

・税金

・社会保険

・扶養

はややこしいんですよね。

なので復習も兼ねてお話しします。

『扶養の範囲内で』

という視点であれば

130万円ですね。

扶養には大きく2種類有ります。

・税金上の扶養

・社会保険上の扶養

だから一言で扶養と言っても

どっちの事を言ってるか

というのを前提にしないと

話が大きく変わってくるんですよね。

だから

違いと仕組みを

良く理解すること。

税金だけを考えて

稼ぎを抑えるというのは

(出典:https://shop.gyosei.jp/online/archives/cat01/0000002735)

『木を見て森を見ず』

になってしまいます。

世帯全体で

収入アップと安定をはかる事が

大切です。

●税か社保か、それが問題だ~知らずに働くと“手取り迷子”~

税金と社会保険について

おさらいしましょう。

全体図をつかんでないと

今どこの話をしているのか

わからなくなっちゃうので

一旦

・社会保険

・税金

についての

全体図を見ておきたいと思います。

税金と言っても

色々あります。

給与・所得に関係する

税金というのは

・所得税

・住民税

この2つです。

【所得税について】

(出典:https://gentosha-go.com/articles/-/49713)

所得税というのは

課税所得に対して

5〜45%税金がかかる。

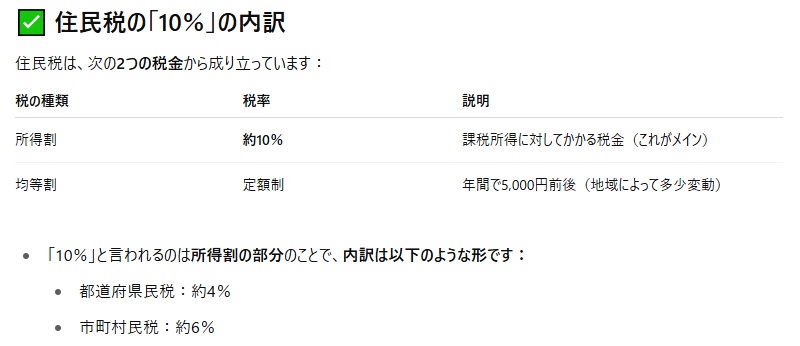

【住民税について】

住民税というのは

課税所得に対して

10%税金がかかる。

後でまた出てくるので

覚えておいてください。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

パートや主婦が「扶養範囲内」で働く場合、年収の基準には「税金上の扶養」と「社会保険上の扶養」の2種類があり、それぞれ注意が必要です。

税金面では年収103万円以下で所得税がかからず、配偶者控除が受けられます。

一方、社会保険の扶養は年収130万円以下が基準で、これを超えると自分で健康保険や年金の保険料を支払う必要が出てきます。

配偶者特別控除は150万円まで満額受けられますが、130万円を超えると社会保険料の負担が増え、手取りが減る場合があります。

したがって、最も「扶養の範囲」を活かしたい場合は、年収130万円以内に抑えるのが一般的に有利です。

世帯全体で手取りや安定を考え、制度の違いを理解した上で働き方を選ぶことが大切です。

[1] https://part.shufu-job.jp/news/knowledge/13061/

[2] https://www.lemon8-app.com/@emumotomichia/7391960681819570693?region=jp

[3] https://www.aeonbank.co.jp/column/tax/nenshuunokabe/130manen/

[4] https://townwork.net/magazine/knowhow/taxes/62818/

[5] https://www.bk.mufg.jp/column/others/b0072.html

[6] https://moneiro.jp/media/article/tax130

≪≪Chat-GPTくんによる英訳≫≫

💰 Today’s Topic: The Power to Save

How Much Can Part-Time Workers or Housewives Earn While Staying Within the Spouse’s Dependent Range to Maximize Benefits?

—

🎯 “Tax or Social Insurance—A Game-Changer for Your Future.

Use the ‘Shield of Dependency’ for a Smarter Family Tax Strategy.”

—

📬 We received two great questions today:

Question 1:

> “I heard the income limit for part-time workers who want to stay under their spouse’s tax and social insurance coverage has changed.

> There used to be thresholds like ¥1.03 million and ¥1.3 million…

> What’s the optimal income level to maximize the benefits of staying a dependent?”

—

Question 2:

> “My husband is a company employee, but I’m the one doing the side business.

> Would it be better for me to earn beyond the dependent range and pay taxes myself,

> or to work part-time within the dependent limit and channel the income under my husband’s name?

> Would the latter give us better tax benefits?

> Is that even allowed?”

—

Actually, we’ve touched on this topic before:

Episode 51: How to Increase a Company Employee’s Take-Home Pay Through Deductions

Episode 52: How to Increase Take-Home Pay—Part 2-1

—

🧩 Taxes, Social Insurance, and “Dependents” Are Confusing

So let’s take a moment to review and get a clear overview.

If your focus is purely on “staying within the dependent range”,

then ¥1.3 million is the key threshold.

But remember:

There are two types of “dependent” status:

1. For tax purposes

2. For social insurance purposes

So when someone says “dependent,”

you first need to ask: Which one are we talking about?

Because the outcome is completely different depending on that.

—

🧠 Understanding the Distinctions Is Crucial

If you only focus on tax savings and limit your income accordingly,

you might fall into the trap of:

> “Not seeing the forest for the trees.”

> (Source: [https://shop.gyosei.jp/online/archives/cat01/0000002735](https://shop.gyosei.jp/online/archives/cat01/0000002735))

What really matters is maximizing household income and long-term stability.

—

🎭 “Tax or Social Insurance — That Is the Question.

Work Without Knowing, and You’ll Lose Track of Your Take-Home Pay.”

—

🧾 Let’s Review Taxes and Social Insurance

If you don’t understand the big picture,

it’s easy to get lost in the details and forget what part of the system you’re even talking about.

So let’s go back to the fundamentals:

Social Insurance & Taxes — The Big Picture

When we talk about income-related taxes, there are two main types:

1. Income Tax

2. Resident Tax*(also called Municipal Tax)

—

【About Income Tax】

(Source: [https://gentosha-go.com/articles/-/49713](https://gentosha-go.com/articles/-/49713))

Income tax is **progressive**, meaning:

The more you earn,

The higher your tax rate,

Ranging from 5% to 45% of your taxable income.

—

【About Resident Tax】

Resident tax is flat, generally:

10% of your taxable income,

Plus a fixed amount (capitation tax) of around ¥5,000–¥6,000, depending on your local government.

Keep these figures in mind—they’ll come up again later.

Special Thanks OpenAI and Perplexity AI, Inc