管理人オススメコンテンツはこちら

「非常に合理的な設計|安心の毎日を!収入保証保険の魅力とは?」

〜前回のつづき〜

●死ぬなら早めが“お得”? ~収入保証保険の真実~

収入保証保険の特徴は

3つ有ります。

(1)生命保険としての機能

基本的には

・死亡時

・高度障害時

にしか支払われません。

(2)保険金は月額支給

基本的には

月額〇〇万円という形で

分割して支給されます。

いわゆる

給料のような形で受け取れる。

日々の生活費の足しに

出来るんですよね。

だから

・遺族年金

・公的保証

・会社の福利厚生

と合わせると

生活をガッチリ

守る事が出来る。

この収入保証保険の中には

一括受け取りを選択できる

商品もありますが

理由は後述しますが

収入保証保険を

選ぶ意味がありません。

収入保証保険で

一括受け取りを選んでしまうと

受け取り総額も減ってしまうし

この収入保証保険を

選ぶ意味が無いので

それは注意してください。

(3)保険金額は段階的に減っていく

収入保証保険が割安な理由です。

例えば死亡した時

死亡後60歳まで

毎年180万円

月額15万円受け取れる

という契約の

収入保証保険に入ったとする。

もしも

30歳で亡くなってしまった場合

残り60歳まで30年間有るので

総額5,400万円受け取れる

という事ですよね。

180万円✕30年=5,400万円

そして

50歳で亡くなってしまった場合

残り10年間で

総額1,800万円の

受け取りになるんですね。

180万円✕10年間=1.800万円

つまり

どういう事かというと

厚い保証が必要な時期

つまり若い時期には

多くの保証で

歳を重ねて子供も育って

保証が不要になってくる時期には

少ない保証の保険なんですね。

年齢が上がって

死亡率が高まる頃には

保証額が少なくなる。

なので

保険会社としては負担が減るし

したがって

保険料を割安に設定出来る。

非常に合理的な設計なんですよね。

だからこれ自体はいい保険です。

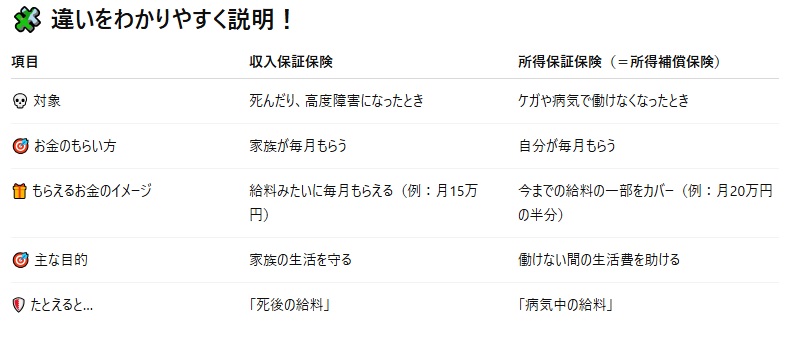

●名前は似てるが、使えなさは桁違い~見た目だけは兄弟。中身は…まるで別人~

似たようなものに

『所得保証保険』というものが

あります。

収入保証保険とは別物です。

こっちは

実用性がないので

注意してください。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

収入保証保険は、死亡または高度障害時にのみ保険金が支払われる生命保険で、主に月額で分割支給されるのが特徴です。

給料のように毎月受け取れるため、遺族年金や会社の福利厚生などと組み合わせることで、遺族の生活を安定して支えることができます。

保険金額は年齢や経過年数に応じて段階的に減少するため、若い時期には手厚い保障があり、年齢を重ねるごとに保障が減る設計となっており、その分保険料も割安です。

一括受け取りを選ぶと受取総額が減るため、月額支給型を選ぶのが基本です。

なお、似た名前の「所得保証保険」は全く別物で実用性が低いので注意が必要です。

[1] https://hokencospa.jp/categories/medical/columns/life-needed

[2] https://diamond.jp/articles/-/25546

[3] https://www.renosy.com/magazine/entries/4830

[4] https://kepco.jp/miruden/kurashimall/category_top/14

[5] https://www3.nhk.or.jp/news/special/news_seminar/jiji/jiji116/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Last Post~

【“Dying Early Pays More?” The Truth About Monthly Income Insurance】

There are three key features of Monthly Income Insurance (Shūnyū Hoshō Hoken).

—

(1) It Functions Like a Life Insurance Policy

Basically, it only pays out if:

You die, or

You suffer a severe disability.

—

(2) The Payout Comes Monthly

Instead of receiving a lump sum, beneficiaries get a fixed monthly amount, such as ¥150,000/month.

In other words, it’s structured like a monthly salary.

This helps cover everyday living expenses.

That’s why, when combined with:

Survivors’ pensions

Public benefits, and

Company welfare programs

…it can form a solid foundation for protecting your family’s lifestyle.

Some monthly income insurance policies do offer a lump-sum option, but—

Let’s be clear: That defeats the entire purpose of choosing this kind of insurance.

Choosing a lump sum lowers the total payout, and

frankly, you lose the benefit of the product.

So beware of that option.

—

(3) The Total Insurance Value Decreases Over Time

This is what keeps monthly income insurance affordable.

For example:

Say you buy a policy that pays ¥1.8 million per year (¥150,000/month) until you turn 60.

If you die at age 30, you have 30 years of payouts left—

¥1.8 million × 30 = ¥54 million in total.

But if you die at age 50,

you only receive 10 years of payouts:

¥1.8 million × 10 = ¥18 million.

So what does this mean?

When you’re young and your family depends on you most, the coverage is bigger.

As you get older and your kids grow up, the need for coverage shrinks, so does the payout.

By the time your risk of death is higher (older age),

the benefit amount is smaller—and that’s by design.

This reduces the insurer’s financial risk,

which allows them to offer lower premiums.

In short, it’s a very logical, well-structured insurance plan.

> A solid insurance product for the right purpose.

—

【Same Name, Totally Different Game-Looks like a sibling. Inside? Not even close-】

There’s another product called Disability Income Insurance (Shōtoku Hoshō Hoken).

It sounds similar, but it’s an entirely different thing.

And this one?

Frankly—not practical.

Don’t get fooled by the name.

Special Thanks OpenAI and Perplexity AI, Inc