管理人オススメコンテンツはこちら

「金利の重要性|キャッシュが命、投資のチャンスを逃すな!」

〜前回のつづき〜

●金利の感覚がない人は資産を失う~金利をなめると人生を損する~

今は住宅ローンの金利は

1%程度ですが

もしも

住宅ローン金利が

10%なのであれば

元本を早く返さないと

利息がドンドン膨らんでしまいます。

しかし

住宅ローンや奨学金というのは

低金利なんですよね。

1%以下がほとんどですよね?

なので

金利の相場感を身につけておく

というのが大切です。

どれぐらいの金利であれば

早く返す必要が有って

そうじゃなければ

早く返す必要は無いのか。

投資をする場合も一緒で

相場感を身につけておくというのが

すごく大事です。

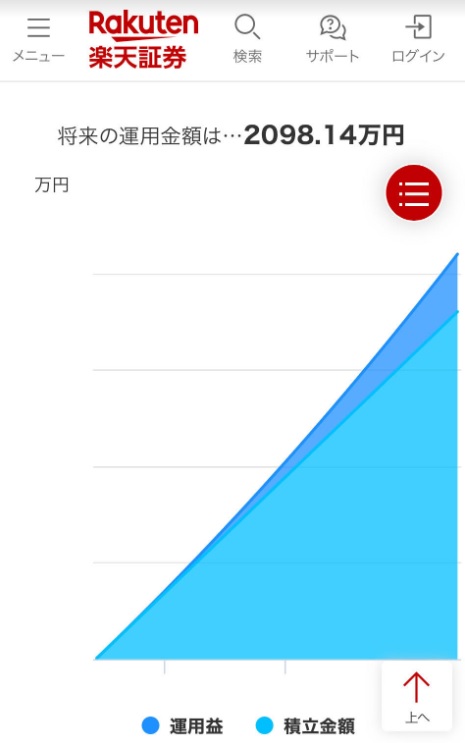

(ケース1)

仮に毎月5万円を

30年間積立投資したとすると

30年間で1800万円

積み立てる訳なんですけど

5万円×12ヶ月×30年間=1,800万円

30年後に5万円ずつ

毎月積み立てていって

30年後に年利が1%の場合だと

2,098万円になってるんですよね。

298万円増える。

2,098-1800=298万円

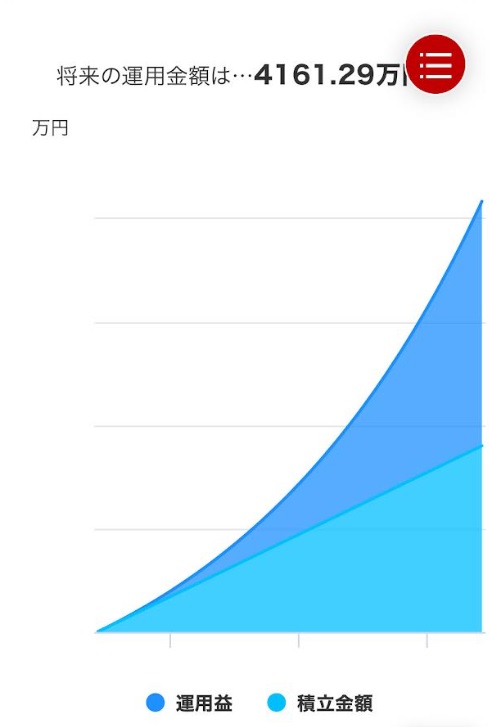

(ケース2)

30年間

年利5%で運用していったとすると

4,161万円になってて

2,361万円増えるんですよね。

4,161-1800=2,361万円

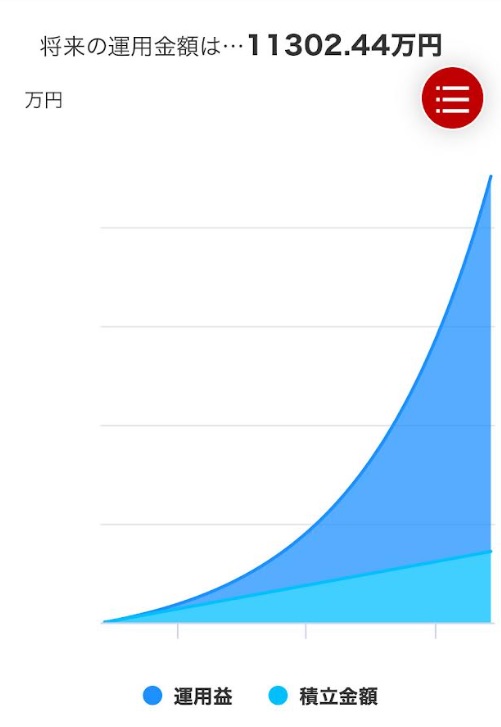

(ケース3)

もしも年利10%で

この30年間運用した場合

もともと

元本で積み立ててるのは

1,800万円なのに

1億1,302万円になる。

要は9,500万円くらい増える。

11,302-1,800=9,502万円

(出典:Wikipedia)

よく出てきますけど

投資の神様

ウォーレン・バフェットさん。

この人の平均利回りは

どれぐらいかと言うと

22%ぐらいなんですよね。

ゆえに

『投資の神様』と呼ばれている。

5万円積み立てていって

年利10%で1億円を超えるのに

22%の平均利回りで

お金を毎年運用していったら

一体いくらになるのか?

だから

世界一のお金持ちなんですよね。

●投資で味方に、借金で敵に~金利は刃にも盾にもなる~

何が言いたいかというと

金利というのは

ものすごく大事だという事です。

投資をしたら

これだけ増える訳です。

金利5%でも

結構増えるんですけど

10%で投資をしたら

これだけ増える訳ですよね?

借金をするという事は

真逆の事が起きる

という事ですね。

だから金利が高いものは

早く返した方がいいし

金利の低いものというのは

そんなに慌てて返そうとしなくていい。

急いで返してもそんなにメリットは無い

という事です。

●Cash is King~繰り上げ返済では王様になれない~

手元の現金が無いと

投資機会を逃してしまいます。

投資においてキャッシュは王様です。

例えば繰り上げ返済をして

手元の現金がゼロだったと

するじゃないですか。

という事で繰り上げ返済して

手元の現金が現在ゼロだったとする。

ずっと投資物件を探してて

そんな時タイミングよく

本当にいい不動産物件が出たら

手元に500万円があれば

小さい中古の戸建てを買って

運用する事も出来るし

もしくは500万円を頭金にして

銀行でお金を借りる事ができます。

3000万円借りるのか

4000万円借りるのか

それは別にして

そういう事が出来るんですよ。

でも手元に現金が無いと

買いたくても買えないんですよね。

何をどうしても買えないんですよ。

お金がないですからね。

銀行もフルローンとかでは

なかなか出してくれないので

繰り上げ返済した分だけ

「じゃあ私500万円だけ

繰り上げ返済したから

早く返した500万円だけ貸してよ!」

というのも当然無理なんですよ。

それはそれ

これはこれ

全く別の話。

銀行というのは

そういう考え方なので

そういう事は出来ないです。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

金利の感覚を持たないと資産を失うリスクがあります。

住宅ローンや奨学金は現在1%前後の低金利ですが、もし金利が10%であれば返済を急がないと利息が膨らみ損をします。

金利の相場感を身につけ、どの程度の金利なら早期返済が必要か判断することが大切です。

また、投資でも金利の違いは大きな差を生みます。

例えば毎月5万円を30年間積み立てる場合、年利1%と10%では最終的な資産額が大きく異なります。

金利は投資では味方、借金では敵になるため、高金利の借金は早く返し、低金利なら急ぐ必要はありません。

さらに、繰り上げ返済で手元の現金がなくなると、投資のチャンスを逃す可能性もあるため、現金を残しておくことも重要です。

Citations:

[1] https://mogecheck.jp/articles/show/51rzNy7XEJ5o4mQ6ZkVv

[2] https://www.sumai-surfin.com/columns/mansion-knowledge/mortgage1

[3] https://news.yahoo.co.jp/articles/eed7d83450493556528cb71d06ff60b957d11ccb

[4] https://www.mc-j.co.jp/rate/normal_202504.html

[5] https://diamond-fudosan.jp/articles/-/132585

[6] https://finance.recruit.co.jp/article/f001/

[7] https://www.sbishinseibank.co.jp/retail/housing/column/vol152.html

[8] https://finance.recruit.co.jp/article/rate-ranking/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous post~

【Those Who Lack Interest Rate Awareness Lose Wealth】

~Underestimating Interest Will Cost You in Life~

Mortgage rates today are around 1%.

But imagine if mortgage rates were 10%—

In that case, you’d need to repay the principal quickly, or interest would snowball rapidly.

Fortunately, mortgage loans and student loans are generally low-interest.

Most are below 1%.

That’s why it’s crucial to develop a sense of interest rate benchmarks.

You need to know:

What level of interest justifies paying off debt quickly, and

When it’s okay not to rush.

This applies to investing too—

Understanding market-level interest rates is absolutely essential.

—

【Case Studies: The Power of Compound Interest】

Case 1:

If you invest ¥50,000 per month for 30 years:

That’s ¥1.8 million total invested

(¥50,000 × 12 months × 30 years = ¥18,000,000)

At a 1% annual return, you’d end up with ¥20.98 million.

→ Profit: ¥2.98 million

Case 2:

At a 5% return, you’d have ¥41.61 million.

→ Profit: ¥23.61 million

Case 3:

At 10%, the total becomes ¥113.02 million.

→ Profit: ¥95.02 million

(Source: Wikipedia)

—

Warren Buffett, the “Oracle of Omaha”

The legendary investor Warren Buffett is often quoted in this context.

His average annual return is about 22%, which is why he’s called the “God of Investing.”

If you can exceed ¥100 million with 10% annual returns,

How much wealth could you build with 22% per year?

That’s why he’s one of the richest people in the world.

—

【Invest and Interest Becomes an Ally, Borrow and It Becomes a Foe

~~Interest Can Be a Blade or a Shield~~】

The core message:

Interest is incredibly powerful.

With investing, even 5% adds up.

But with 10%, the growth is tremendous.

Debt works in the exact opposite direction.

High-interest loans should be paid off quickly.

But low-interest loans don’t need to be rushed.

Paying them off quickly doesn’t offer much advantage.

—

【Cash is King~You Can’t Become Royal Through Early Repayment~】

If you don’t have cash on hand, you’ll miss investment opportunities.

In investing, cash is king.

For example, if you aggressively pay off your loan and are left with no cash:

> \[Speech bubble] “I just want to pay off my debt as fast as possible!”

Then a great investment property appears.

If you had ¥5 million,

You could buy a small second-hand home and rent it out,

Or use it as a down payment to borrow more from a bank.

Whether you borrow ¥30 million or ¥40 million isn’t the point—

The key is: with cash, you have options.

But with zero cash,

You can’t buy—no matter how good the deal is.

No bank will offer a full loan without collateral or down payment.

—

And no, you can’t say:

> \[Speech bubble]

> “Hey, I paid ¥5 million early.

> Can I just borrow that back now?”

That’s not how banks work.

What’s paid is paid.

What’s borrowed is borrowed.

It’s a completely separate matter.

Banks operate on strict logic—and they won’t give back what you’ve prepaid.

Special Thanks OpenAI and Perplexity AI, Inc