管理人オススメコンテンツはこちら

「治る訳ではない|がん保険は無駄な出費?知っておきたい真実とは!?」

〜前回のつづき〜

●がん保険は得なのか?損なのか? ~それは“がんの訪れ方”で決まる~

がん保険は得なのか損なのか?

掛け捨て保険であれば

自分ががんになるかを賭ける

『不幸のギャンブル』です。

保険に入って

すぐがんになれば得だし

高齢でがんになったら

払い込んだ分損する

という事になります。

ざっくり計算ですが一例を。

条件によって変わるんですけど

基本の考え方です。

例えば

30歳の人が毎月がん保険に

3千円払って入ったとします。

がんになったら

100万円もらえるとします。

では

27年以内にがんになったら

得なんですよね。

100万円÷(3千円×12ヶ月)

=27.77年

それ以上なら損する。

27年以上経ってから

がんになってしまうと

払い込んだ分を考えると損

という事になります。

もちろん実際は

入院の給付など条件によって

毎月いくらかけるかとか

年齢によって

保険料があがっていったりとか

色々有るので

色々複雑なんですけど

基本の考え方は

こういう事なんですね。

では

30歳の人が60歳になるまでに

がんになる確率はと言うと

前々回お話しした通り

7%なんですよね。

これをどう見るか?

高いと見るか

低いと見るか。

さらに毎月掛金は

払い続けるので

50歳でがんになったからといって

お得ではないんですよね。

要は27年以内に

がんになったら得なんですが

では

25年目にがんになった場合

どうなのかと言うと

得は得だけど

ほんの少しだけです。

ちょっとだけです。

あまり得しないという事ですね。

さらに実際には

適用外のがんも有ります。

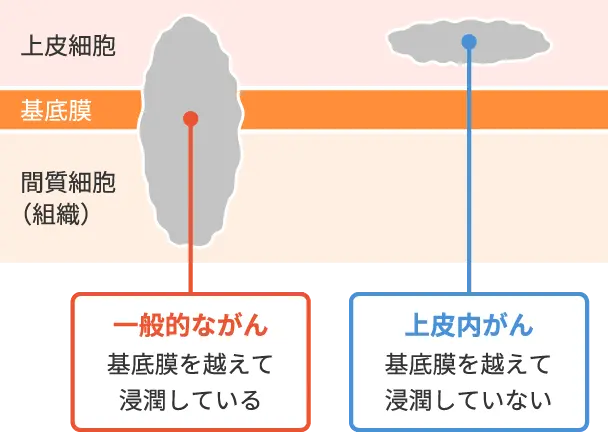

(出典:https://www.hokende.com/life-insurance/cancer/basic_info/select_in_situ)

『上皮内(じょうひない)がん』と言って

ステージ0と言われる初期のがんですけど

この辺は

保障の対象外と言われる事も

実際多いんですよね。

実際約款で保障の内容を

よく読んでみていただきたい。

●がんの治療費は保険じゃなくて、あなたの資産でカバーする時代。

色んなお話しをしましたが

その上で私は

がん保険は不要だと考えます。

がん保険だけじゃなく

ほとんどの保険は不要だと

私は思っています。

なぜかと言うと

がん保険に入るよりも

生活防衛資金を貯めたり

その余った分を投資した方が

コストパフォーマンスがいいからです。

がん保険に入ってたからと言って

がんが治る訳ではないんです。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

がん保険は「がんになるタイミング」で得か損かが決まります。

例えば30歳で月3,000円の保険料を払い、がんになったら100万円受け取れる場合、約27年以内にがんになれば得ですが、それ以降だと払い込んだ保険料の方が多くなり損になります。

30歳から60歳までにがんになる確率は約7%と低く、実際には初期の上皮内がんなど保障対象外のケースも多いため、保険のメリットは限定的です。

筆者は、がん保険に入るよりも生活防衛資金を貯め、余剰資金を投資に回す方がコストパフォーマンスが良いと考えています。

がん保険は治療費を直接減らすものではなく、万一の備えとしての役割に過ぎないため、加入は自身の資産状況やリスク許容度を踏まえて慎重に判断すべきです。

Citations:

[1] https://www.hokende.com/life-insurance/cancer

[2] https://sc.salivatech.co.jp/magazine/cancer-insurance/

[3] https://konohoken.com/cancer/relax/

[4] https://hoken.kakaku.com/gca/

[5] https://www.navinavi-hoken.com/articles/2025-fp-cancer-ranking

[6] https://www.randcins.jp/hoken/cancer-insurance/market_price/

[7] https://www.nanairolife.co.jp/hoken/cancer-insurance/

[8] https://www.zurichlife.co.jp/product/category_gan/column_list/column20

[9] https://www.fukuishimbun.co.jp/articles/-/1426670

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Previous Post~

【Is cancer insurance a good deal or a waste of money? — It all depends on how cancer comes.】

When it comes to cancer insurance, is it worth it or not?

If it’s a term insurance plan, you’re essentially betting on whether or not you’ll get cancer.

It’s a “gamble on misfortune.”

If you get cancer soon after signing up, you’re ahead.

But if you get it in old age, you may have paid in more than you’ll ever get back.

Here’s a rough example (the actual outcome may vary, of course):

Let’s say a 30-year-old pays ¥3,000 per month for cancer insurance.

If they get cancer, they receive a lump sum of ¥1,000,000.

So:

1,000,000 ÷ (3,000 × 12) = 27.77 years

That means:

If you get cancer within 27 years, you’re getting a “good deal.”

If you get cancer after that, you’ve paid more than it’s worth.

Of course, in reality, things are more complex:

There are hospitalization benefits, premium increases with age, different policy structures, and so on.

But this is the core idea.

Now, what’s the chance that a 30-year-old will get cancer by the age of 60?

As mentioned before — it’s 7%.

How do you interpret that?

Is it high, or low?

And remember, you keep paying the monthly premium, regardless.

So even if you get cancer at 50, it doesn’t mean you came out ahead.

If you get cancer in the 25th year, you technically “win” — but just barely.

Not by much.

So in most cases, you don’t really profit.

Also, not all types of cancer are covered.

For example, carcinoma in situ (Stage 0 cancer) is often excluded from coverage.

This is more common than you’d think —

So it’s essential to read the policy terms carefully.

—

【We live in a time where cancer treatment is no longer covered by insurance — it’s covered by your assets.】

After covering all of this, here’s my conclusion:

I believe cancer insurance is unnecessary.

In fact, I think most insurance is unnecessary.

Why?

Because instead of paying for cancer insurance, you’re better off:

Building a solid emergency fund, and

Investing the surplus.

It’s simply a better return on your money.

And let’s be clear:

Buying cancer insurance doesn’t cure cancer.

Special Thanks OpenAI and Perplexity AI, Inc