「共済=バス、保険=タクシー|共済vs保険、あなたの選択は?」

〜前回のつづき〜

●共済はバス、保険はタクシー~あなたはどっちに乗る?~

商品の特徴を紹介します。

(1)共済の場合

1-a)掛金が一律

誰が入っても

・性別

・年齢

など関係なく

掛金は一律です。

1-b)パッケージ商品

医療保険+生命保険(死亡保障)の

パッケージ商品です。

例えるなら

食堂で言えば◯◯定食。

単品で頼む事は出来ない

という事です。

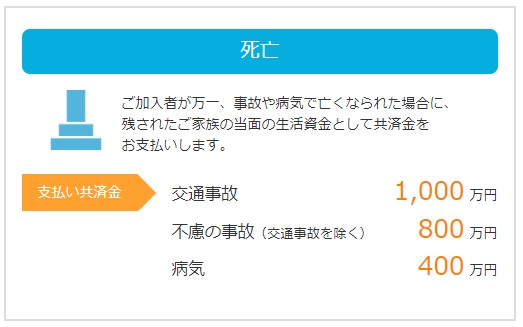

1-c)保障金額が少ない

1-d)基本は掛け捨て商品のみ

1-e)高齢時の保障が薄くなる

年齢が上がっていくと

保証が薄くなるんですよ。

(2)保険の場合

2-a)年齢や性別で保険料が変わる

2-b)種類が豊富

2-c)保険金額が柔軟に設定できる

2-d)貯蓄型はボッタクリが多い

中身は実質

ボッタクリの投資信託と

言ってますけど

貯蓄タイプが結構勧められやすい。

独特のめんどくささも有ります。

e)高齢時の保険料の支払いが高くなる

共済であれば

掛金が同じ代わりに

保証が薄くなる。

その代わり民間保険は

もらえる金額が一緒だとしても

保険料の支払いが

その分高くなっていきます。

どちらも一長一短あります。

共済=バス

保険=タクシー

なんてまとめられ方を

される事があります。

●シンプルで安い共済か、手厚く備える民間保険か?~共済の“割安”と民間の“安心”~

結局

民間保険と共済どっちがいいのか?

これは一長一短なんですよね。

都道府県民共済の

メリットデメリットですが

(1)メリット

a)掛金が安い

b) 商品内容が分かりやすい

パッケージになってて

民間の保険商品よりも

掛け捨てばかりなので分かりやすい

c)割戻金(わりもどしきん)がある

割戻金というのは

100人からお金を集めて

誰かが死亡したり

事故を起こしたりした時に

そこから

お金が支払われるというのが

保険の仕組みなんですけど

あまり今年支払いが無かった場合

だれも保険が必要無かったら

そのお金が一部戻ってくるんですよね。

保険には無いというか

共済の仕組みですよね。

これを割戻金と言います。

d)年齢や性別に関係なく掛金が一定

e)高齢者にとっては割安

(2)デメリット

a)保障額が少ない

(出典:https://www.zenkokukyosai.or.jp/product/life/total/example.html)

b)パッケージなので医療保険と生命保険を別々に契約出来ない

病気になった時の保障と

死亡保障が別に出来ないんですよ。

だから

「病気になった時の保険は

いりません。

生命保険=死亡保障の分だけ

必要です」

と言っても

契約出来ないという事です。

パッケージなので

必ずセットで買わないといけない

という事です。

c)高齢者になると保障金額が減る

高齢者にとって割安という事は

若者にとっては割高なんですよね。

d)倒産のリスクがある

民間の保険の場合は

90%ぐらいまでは

セーフティーネットがあって

もし保険会社が倒産したとしても

経営危機になった場合も

保障が受けられるんですけど

この共済の場合はそれが無いので

受けられないんですね。

かと言って

倒産するのかと言ったら

その可能性も低いと思いますし

そんなにデメリットにもならない

という人もいるかとおもいますが

一つそういう事があるという事です。

このようにそれぞれ

メリットデメリットがあります。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

共済と民間保険にはそれぞれ特徴とメリット・デメリットがあります。

共済は掛金が年齢や性別に関係なく一律で、医療保険と生命保険がセットになったパッケージ商品です。掛け捨てが基本で保障金額は控えめですが、割戻金があり、シンプルで割安な点が魅力です。ただし、高齢になると保障が減り、保障内容の細かい調整はできません。また、倒産時のセーフティーネットがない点も注意が必要です。

一方、民間保険は年齢や性別で保険料が変わり、保障内容や金額を自由に設定可能です。貯蓄型もありますが、手数料が高い場合が多く、高齢になると保険料が上がる傾向があります。倒産時の保障があるため安心感は高いです。

共済は「シンプルで安いバス」、民間保険は「自由度が高く手厚いタクシー」と例えられ、どちらを選ぶかは保障の手厚さとコストのバランスを考慮して判断すると良いでしょう。

Citations:

[1] https://www.rakuten-card.co.jp/minna-money/insurance/life_insurance/article_2112_00001/

[2] https://maneomaneko.tsite.jp/article/3215/index.html

[3] https://www.hokepon.com/column/prefectural_mutual_aid/

[4] https://hoken-room.jp/mutual-aid/7727

[5] https://money-sense.net/2997/

[6] https://reaho.net/magazine/hokenkiso/tominkyosai/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous discussion~

【Product Characteristics】

(1) In the Case of Kyosai (Cooperative Insurance)

1-a) Flat Premiums

Everyone pays the same premium regardless of:

Gender

Age

1-b) Packaged Product

Medical insurance and life insurance (death coverage) come as a package.

It’s like a set meal at a diner—you can’t order individual items.

1-c) Lower Coverage Amounts

1-d) Basically Term-Only Products

Most plans are “term insurance only,” meaning no refund or savings element.

1-e) Coverage Decreases with Age

As you get older, the amount of coverage becomes smaller.

—

(2) In the Case of Private Insurance

2-a) Premiums Vary by Age and Gender

2-b) Wide Variety of Options

2-c) Flexible Coverage Amounts

2-d) Savings-Type Products Often Have High Fees

Some savings-type insurance plans are essentially overpriced investment trusts.

These are often pushed by sales reps, but they come with unique complications.

2-e) Premiums Increase with Age

With Kyosai, the premiums stay the same but coverage decreases with age.

With private insurance, even if the payout stays the same, the premiums go up.

—

Both options have advantages and disadvantages.

It’s sometimes summarized like this:

> Kyosai = Bus

> Private Insurance = Taxi

—

【“Simple and Cheap or Flexible and Secure?”

\~ Kyosai’s “affordability” vs Private Insurance’s “reliability” \~】

So in the end…

Which is better: private insurance or Kyosai?

There’s no clear winner—it depends on your needs. Both have pros and cons.

—

■ Pros of Kyosai (Prefectural Residents’ Mutual Aid)

a) Low Premiums

b) Simple and Easy-to-Understand Package Products

Mostly term insurance, easy to grasp.

c) Warimodoshi-kin (Refunds)

If claims are low in a given year, members get part of their money back.

This is unique to Kyosai, not found in typical insurance.

d) Fixed Premiums Regardless of Age or Gender

e) More Affordable for Seniors

—

■ Cons of Kyosai

a) Low Coverage Amounts

b) No Customization—Medical and Life Insurance Are Bundled

You can’t separate illness and death coverage.

Even if you only want life insurance, you must buy the full set.

c) Coverage Shrinks with Age

While it’s cheaper for seniors, it’s costlier (per coverage) for younger people.

d) Risk of Insolvency

Unlike private insurers (which have a \~90% safety net system),

Kyosai has no such protection if it goes bankrupt.

That said, the actual risk of collapse is low.

Still, it’s something to keep in mind.

—

So again, both systems have their strengths and weaknesses.

Your choice should depend on your life stage, budget, and what kind of peace of mind you value most.

Special Thanks OpenAI and Perplexity AI, Inc