「およそ2億円|貯めるだけじゃない、増やす力があなたを救う」

今日は【増やす力】

最速でお金持ちになるにはどうすればいいか?

についてお話しします。

●稼いで、回して、増やす~億を超える資産への最短ルート~

お金持ちになるには

給与か事業で稼いだお金を

投資にドンドンまわす。

自分で出来る

お金持ちへの上がり方は

これしか無いです。

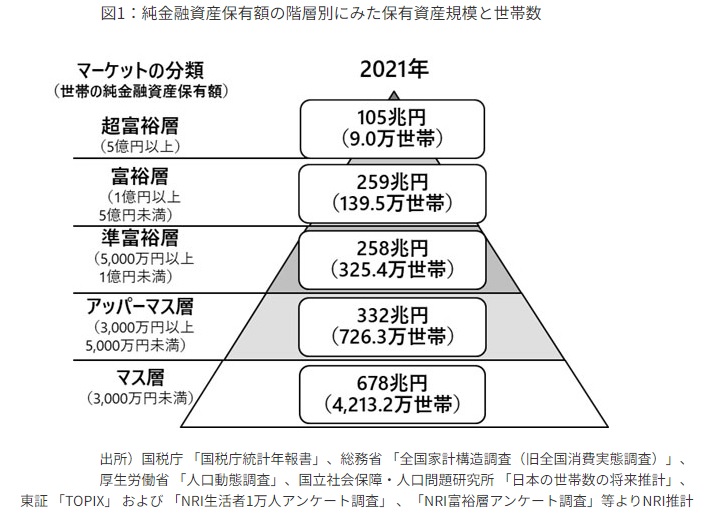

(出典:https://www.nri.com/jp/news/newsrelease/files/900037282.pdf)

お金持ちとは野村総研が

純資産1億円以上ある世帯を

富裕層と定義しています。

●1億円貯める道は普通の貯金じゃ遠すぎる~時間がないなら早く結果を出す方法を選ぶべき~

では1億円貯めるには

どうしたらいいのか?

一般的な年収で普通に働いてたら

ほとんどの人が会社員をされてて

給料をもらうという方が多いと思います。

そのような会社員で働いてて

会社員がダメという話ではなくて

一般的な年収で普通に働いてたら

やはり1億円貯めるというのは難しい。

普通に考えてそうじゃないですか?

毎月10万円貯金したとしても

毎月10万円って結構な額ですよね?

毎月10万円貯金したとしても

1年で120万円

という事は40年間働いて

4800万円なんですよね。

毎月ずっと10万円貯金し続けても

40年間ずっと貯金し続けて4800万円。

毎月20万円貯金し続けて

やっと40年で9600万円。

毎月ずっと貯金し続けるって

平均の所得から考えたら

難しいですよね?

途中で子供が生まれたり

教育資金だとか

色々有るじゃないですか。

そういうのも含めて

40年間ずっと

20万円貯金し続けるって

難しいですよね?

仮に

40年貯めて1億円貯まったとしても

貯まる頃には

人生の時間が

もうあまり無いんですよね。

もう老後になってしまってる

という事ですよね。

なので

その頃貯めてもどうかなという所で

早く貯めたいのであれば

普通に貯めてたら難しい。

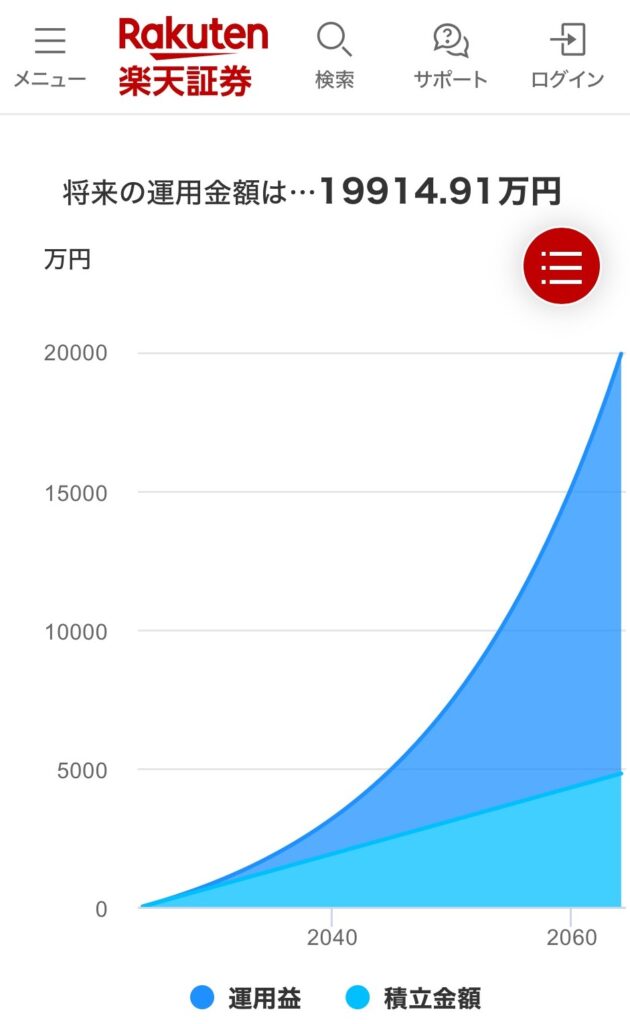

●毎月10万円の貯金で4倍の未来が手に入る~6%の力で1億9千万円の差をつけろ~

では投資に回したらどうなるのか?

毎月10万円貯金しながら

年利6%で40年間運用したとすると

先程のパターンだと

40年間10万円ずつ貯金しても

4800万円でしたよね?

これが毎月10万円貯金しながら

年利6%で40年間運用したとすると・・・

1億9千万円になるんです!

毎月同じ事をしていて

すごい差ですよね。

4倍差が出る

という事なんですけど

1億9千万円になる。

税金は考慮してないんですけど

およそ2億円になるという事ですね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

Citations:

[1] https://www.nri.com/jp/news/newsrelease/files/900037282.pdf

[2] https://www.rakuten-card.co.jp/minna-money/feature/article_2204_00013/

[3] https://peach-setsuyaku.com/rich-fastest/

[4] https://www.rakuten-card.co.jp/minna-money/topic/article_1810_00006/

[5] https://www.gentosha.jp/article/22547/?srsltid=AfmBOoq-5kfLaDUkfbQQK6qhBRaTzT3g-sHVM0tf8a56V9_0bFeEs-Se

≪≪Chat-GPTくんによる英訳≫≫

Today’s topic: The Power of Growing Wealth

How can you become rich the fastest?

【Earn, Reinvest, and Grow — The Shortest Path to Over 100 Million Yen】

To become wealthy, you need to take the money you earn from your salary or business and reinvest it aggressively.

The only way to build wealth on your own is through this method.

(Reference: https://www.nri.com/jp/news/newsrelease/files/900037282.pdf)

Wealthy individuals, as defined by Nomura Research Institute, are households with a net worth of over 100 million yen.

【The Road to Saving 100 Million Yen Is Too Long with Regular Savings — If Time Is Short, Choose a Faster Path to Results】

So, how can you save 100 million yen?

For most people, working with an average salary as an employee is the norm. However, working as an employee isn’t the problem.

But when you work with a typical salary, saving 100 million yen is still very difficult.

Think about it — even if you saved 100,000 yen every month, that’s a pretty large amount, right?

If you save 100,000 yen every month, that’s 1.2 million yen a year.

Over 40 years, that would amount to 48 million yen.

If you keep saving 100,000 yen every month for 40 years, you’ll only have 48 million yen.

If you save 200,000 yen a month, you’ll have 96 million yen in 40 years.

Saving every month, even at a high rate, is difficult with an average income, right?

Along the way, you’ll have expenses like children’s education or other financial commitments.

Considering those factors, saving 200,000 yen every month for 40 years is also quite challenging.

Even if you manage to save 100 million yen after 40 years, by the time you reach that amount, you’ll be close to retirement age.

By then, you’ll have very little time left in your working life.

So, even if you manage to save up that amount by then, it may not be enough.

If you want to accumulate wealth faster, relying on traditional savings alone is not enough.

【Save 100,000 Yen a Month for a 4x Better Future — Use the Power of 6% to Create a 190 Million Yen Difference】

What happens if you start investing instead?

If you save 100,000 yen every month and invest it at an annual interest rate of 6% over 40 years, here’s the result:

In the previous example, saving 100,000 yen each month for 40 years would only result in 48 million yen.

However, if you save the same amount but invest it at a 6% return for 40 years…

You’d have 190 million yen!

The difference is staggering, isn’t it?

Even though you’re doing the same thing every month, the difference is four times greater.

This means 190 million yen.

Though taxes aren’t considered in this example, it could approach around 200 million yen.

Special Thanks OpenAI and Perplexity AI, Inc