「解散して終わり|あなたの資産を守る!毎月分配型の落とし穴」

〜前回のつづき〜

●美味しい分配金は、実は毒入り~分配金欲しさに、資産はジリ貧~

(出典:https://www.rakuten-sec.co.jp/web/fund/detail/?ID=JP90C000B5A8)

分配金の仕組み上

特別分配金で出してたら

基準価格というのが

下がり続けるんですよ。

100万円預かろうが

1,000万円預かろうが

基本的には下がっていきますよね?

利益を出せてないのに

分配金を支払うということは

それだけここも価値が下がる。

「分配金込みだったら上がってるじゃないか!」

「このぐらいでいけてるじゃないか!」

「悪くない!トントンじゃないか!」

と言うかもしれない。

これは2023年から

2024年夏までなので

メチャクチャ

いい相場環境の時だったんです。

誰が買っても

買ってさえいれば

上がっていた時だというのに

全く上がってない。

要は

こんなわざわざ難しくて

手数料も取られて

回りくどい商品を買わなくても

ブラジルに

直接投資したいんだったら

もっといい商品

安くて安全な商品を

直接買えばいいでしょ

という話です。

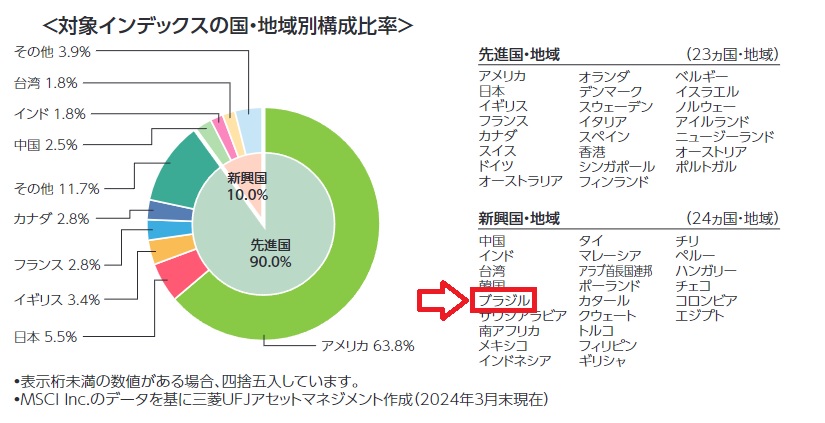

例えば

eMAXIS Slim 全世界株式

(オール・カントリー)。

(出典:https://www.am.mufg.jp/viewer.html?file=%2Fpdf%2Fkoumokuromi%2F253425%2F253425_20240725.pdf&_gl=1*1a4fkk8*_gcl_au*ODI0OTg5MDg4LjE3MjE4NzIxMjU.*_ga*MTk3MTAzMTE0My4xNzIxODcyMTI1*_ga_3ZNV996Y9H*MTcyMzE2OTMxMC4yLjEuMTcyMzE2OTM1OC4xMi4wLjA.&_fsi=NwehdWwZ#page=2)

これには

ブラジルも含まれています。

よく訳の分からない商品にされて

手数料払って買うような商品ではない

ということです。

そっちを買ってたら

1.5倍とか2倍とか

投資先にもよりますが

要はもっと増えてた

という事です。

余分な手数料で

取られてしまって

本来

もっと増えてたはずのものが

全く増えてないという事です。

こういう商品というのは

確実に下がりつづけます。

最終的に解散して終わりになる。

毎月分配型というのは

本当に全く意味の無い商品ばかりです。

結論は

買わないでください!!

それ以外にもいっぱい

色んな商品が有りますが

毎月分配型であれば

基本的に一緒です。

商品の中身を変えてるだけで

債券がどうとか

三カ国ナントカとか色々

・ブラジル儲かりそうとか

・トルコがどうとか

・高金利通貨とか

色んな事言いますけど

全部一緒です。

●まとめ

◆世の中には

合法ボッタクリ投資商品というのが

ゴマンとある

→それが売れ続けている事実

お年寄りや退職金や投資したことのない人を狙って

窓口を通じてすごく営業をかけてくるので注意!

◆銀行や証券会社の窓口で売ってる商品というのは

ボッタクリばっかり

→いい商品が窓口で売られる事はないから近づくな!

私たちにとっていい商品とは

仲介業者からすると手数料が安い商品なので

儲からない。

いい商品を売って欲しいと思うが

なかなかそうはならない。

自分の身は自分で守るしかない。

◆毎月分配型はクズ商品ばかり

→手数料が高い

売る側の都合しか考えない複雑な商品設計

◆自分は何に投資をしているのか

というのを理解して投資する

→わからないものに投資しない

他にも代表的な商品があって

心当たりがあるかもしれません。

引き続き色んな商品について

お話ししていきます。

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

毎月分配型ファンドは、一見魅力的に見える分配金の多くが元本を取り崩す「特別分配金」であり、利益を生まないまま資産価値(基準価格)が下がり続ける仕組みです。

2023年〜2024年夏という良好な相場でもリターンはほぼゼロで、手数料が高く資産成長を阻害します。

例えばeMAXIS Slim全世界株式のような低コストで優良な商品であれば、同期間に1.5〜2倍の成長も期待できました。

銀行や証券会社の窓口商品には手数料重視の「合法ボッタクリ商品」が多く、特に投資初心者や高齢者が狙われやすいのが現状です。

投資では自分が何に投資しているかを理解し、不透明で複雑な商品は避けるべきです。

結論として、毎月分配型は基本的に買わず、知識を持って商品を選ぶことが資産を守る鍵です。

- https://money-sense.net/13811/

- https://www.invest-concierge.com/posts/monthly-distribution-investment-trust-have-some-problem-and-demerit

- https://www.orixbank.co.jp/column/article/014/

- https://info.monex.co.jp/fund/guide/distribution.html

- https://www.daiwa.jp/doc/160310/

- https://www.nomura-am.co.jp/sodateru/stepup/dividend/dividend04.html

- https://www.resonabank.co.jp/kojin/column/toshin/column_0020.html

- https://fpbank.co.jp/column/monthly-distributed-trust

- https://www.smbc.co.jp/kojin/toushin/gimon/purchase08/

- https://www.nikkei.com/article/DGXZQOUB236II0T20C23A1000000/

- https://www.rakuten-sec.co.jp/web/fund/detail/?ID=JP90C000B5A8

- https://medaka.5ch.net/test/read.cgi/market/1672247179

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from last time~

【Delicious Distributions Are Actually Poisonous – Chasing Distribution Payments Leads to Asset Erosion】

Because of how distribution payments work,

if a fund pays out special distributions,

the net asset value (NAV)

keeps declining.

Whether it’s managing 1 million yen

or 10 million yen,

basically, it keeps going down, right?

Paying distributions

when there are no profits

means the fund’s value itself drops.

Some might say:

“Including the distributions, the price is up!”

“It’s doing okay at this level!”

“It’s not bad! It’s breaking even!”

But this is from 2023 to summer 2024—

a period with an incredibly

strong market environment.

Anyone who bought,

anyone who simply held,

would have seen growth,

yet this fund didn’t rise at all.

In other words,

you don’t need to buy these complicated,

high-fee, roundabout products.

If you want to invest directly in Brazil,

there are better products—

cheaper and safer products you can buy directly.

For example,

eMAXIS Slim All Country (All-World Stock Fund).

Brazil is included in this fund.

So, you don’t have to buy

some confusing product

and pay extra fees.

If you had bought that,

depending on the investment,

your assets could have grown 1.5 to 2 times.

But due to extra fees,

what should have grown more

did not grow at all.

Products like this

will certainly continue to decline.

Eventually, they will be liquidated and closed.

Monthly distribution-type funds

are mostly useless products.

Conclusion:

Don’t buy them!!

There are many other products,

but if it’s monthly distribution-type,

it’s basically the same.

Only the contents are changed,

like bonds, or some “three-country something,”

or talk about “Brazil looks profitable,”

“Turkey is this or that,”

“high-interest currencies,”

whatever they say—

it’s all the same.

—

【Summary】

There are countless legal “rip-off” investment products out there.

The fact is they keep selling—targeting elderly people, retirement funds, and those inexperienced with investing—pushing heavily through bank and brokerage counters, so beware!

Products sold at bank or brokerage counters are mostly rip-offs.

Good products are never sold at counters, so stay away!

Good products have low fees, meaning brokers don’t earn much commission.

Although we want good products to be sold, it rarely happens.

You have to protect yourself.

Monthly distribution-type funds are trash products—

high fees, complicated structures designed only for sellers’ benefit.

Understand what you are investing in—

don’t invest in things you don’t understand.

There are other typical products you may know about.

I will continue to talk about various products.

Special Thanks OpenAI and Perplexity AI, Inc