「修理代が払えない人のもの|車を持つなら知っておきたい、保険の真実」

〜前回のつづき〜

●身の丈で買えば、保険なんていらない~“安心”という名の出費で、いくら失ってる?~

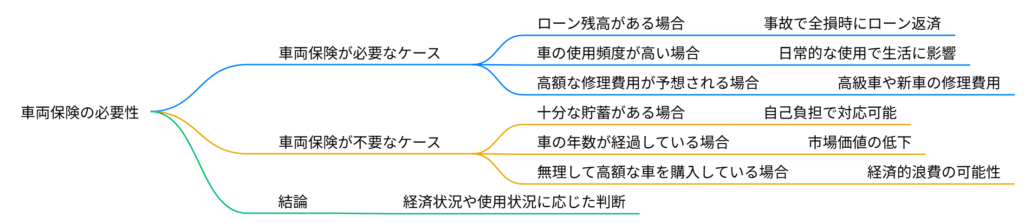

車両保険は不要です。

そもそも車両保険というのは

修理代が払えない人のものです。

そもそも修理代が払えないのに

無理をして車を買っては

ダメです。

例えば

300万円の車を買うとして

修理代も手元に無いという状況下で

ローンを組んで車を買っては

ダメです。

車両保険に入るよりも

大事なことは

最低限の修理費用を

貯めた状態にしておいて

もしも何かあっても

ちょっとぶつけて修理が必要でも

自分で支払える

最低限の分だけ持っておく。

貯めておいた方が

本来はいいんです。

医療保険と一緒です。

医療保険に入るよりは

最低限の治療費・入院費を

貯めておく方が大事です。

無理して買うから

毎月の不要な保険に

入らなければならない。

そもそも無理して

いっぱいいっぱいで買っては

ダメです。

●保険は破産を防ぐもの~壊れた欲を守るものじゃない~

消費と浪費は違います。

自分の車が壊れてしまったら

どうするんだ!」

軽い修理なら

保険を使わないので

普通に直してしまえばいい。

完全に壊れるような

事故を起こしてしまったら

それはもう

安い車に買い替えるチャンスです。

(新車である程度いい車に乗る

という前提だと話がおかしくなります。)

そもそも保険は

『いざ!』という時のために

入るものです。

ではその

『いざ!』という時は

どういう時か。

物事が起きた時に

破産してしまう事を避けるために

保険は入るものです。

・相手を死亡させてしまった

・賠償金がとんでもない

・火事を起こしてしまった

・自分自身が死んでしまった時の子供の将来の為

自分や家族が

経済的に困窮しない様に

万が一の時に備えて入る

これが保険です。

車両保険というのは

いざという時に

破産してしまわない様に

入る保険ではありません。

浪費を維持するための保険です。

ローンを組んで浪費して

そのカバーの為に

毎月高い保険料を支払う。

・浪費

・保険

・投資

全部別物です。

『混ぜるな危険!』です。

いい車の新車に乗るという

浪費を維持する為に

保険に入るというのは

ナンセンスです。

車は生活必需品という方も

いらっしゃる。

ここまでは『消費』です。

「田舎なので交通手段として

どうしても車を

使わなければならないんだ!」

これは確かに必要だと思います。

これは『消費』。

仕方ない。

でも移動手段以上の車というのは

『浪費』です。

生活に必要だということであれば

数十万円の中古車でいいはずです。

でもそこと感情をくっつけて

・どうしてもいい車に乗りたい

・最低このぐらいの車に乗りたい

とローンを組んで買ってしまう。

またの機会にもお話ししますが

車のローンは非常に高い。

だから本来ローンを組まずに

現金一括で買ってしまう方がいいです。

だから

数十万円の中古車でいいはずです。

これであれば

余分な車両保険も付けなくていい。

壊れても

新しいのを買うなり修理するなり

考えればいい。

大前提として

新車でいい車に乗るという

浪費のカバーとして

車両保険に入るから

おかしな事になる。

(またこれはまたの機会にお話しします。)

●まとめ

◆自動車保険

=自賠責保険

&

任意保険

&

車両保険

◆等級

・無事故だと等級が上がり保険料が安くなる

・事故を起こすと3等級ダウンする

◆必要な保険

・対人対物無制限

◆保険の見直しポイント

・保険会社を見直す

・契約条件を見直す

・車両保険を外す

◆車両保険は不要

・修理代が払えない人のもの

◆消費と浪費

・まぜるな危険!

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

車両保険は、修理代が自分で払えない人のためのものであり、基本的には不要です。

そもそも修理費用を用意できないのに無理して高額な車や新車をローンで購入するのは浪費であり、毎月の保険料という余計な出費を生みます。

保険は本来、万が一の大きな損害や破産を防ぐために入るもので、対人・対物賠償のような必要最低限の保障だけで十分です。

生活必需品として車が必要な場合は、数十万円の中古車で十分であり、移動手段以上の車を求めるのは浪費です。

保険や契約内容を見直し、車両保険を外すことで、無駄な出費を抑え、賢くお金を管理しましょう。

[1] https://hokentimes.com/article/businessinsurance/vehicle_insurance/

[2] https://www.insweb.co.jp/car/hokenryou/sharyouhoken-muda.html

[3] https://prtimes.jp/main/html/rd/p/000000007.000126702.html

[4] https://www.zurich.co.jp/car/useful/guide/voluntary-insurance/

[5] https://www.sbisonpo.co.jp/car/guide/vehicle/

[6] https://www.hokepon.com/column/column-sonpo-car-006/

[7] https://www.hokennomadoguchi.com/columns/songai/vehicle/

[8] https://www.insweb.co.jp/car/hokenryou/setsuyaku.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the previous post~

【Buy within your means — How much are you paying for “peace of mind” you don’t need?】

—

Car insurance for vehicle damage (comprehensive/collision coverage) is often unnecessary.

Let’s be clear — these types of insurance are for people who can’t afford repairs.

If you can’t pay for potential repairs out of pocket, you shouldn’t be buying that car in the first place.

For example, if you’re buying a 3-million-yen car (around \$20,000),

and you don’t even have the funds to cover basic repair costs —

then you have no business taking out a loan to buy that car.

Rather than paying monthly premiums for vehicle insurance,

you should focus on building up a repair fund —

enough to cover minor accidents or dents without financial stress.

It’s much wiser to save in advance than to insure for convenience.

It’s the same with health insurance:

Better to have enough saved for basic treatment and hospitalization,

than to keep paying for coverage you may never use.

People end up buying expensive insurance because they’re overextending themselves financially.

They’re buying beyond their means and using insurance as a cushion.

But that’s the root of the problem.

—

Insurance is for preventing bankruptcy — not for protecting your broken ego.

—

There’s a big difference between necessary spending (consumption) and wasteful spending (extravagance).

> “What if my car breaks down and I don’t have car insurance?”

If it’s a minor repair, you wouldn’t file a claim anyway — just fix it and move on.

If it’s a major accident that totals the car,

then maybe it’s simply time to downgrade to a cheaper car.

(The problem only arises when you assume everyone needs to own a new, high-end vehicle.)

Insurance should be for true emergencies —

events that could lead to financial ruin:

Accidentally killing someone

Massive liability or damages

Starting a house fire

Dying and leaving nothing for your children

Insurance exists to protect your family from being financially devastated.

But car insurance for your own vehicle?

That’s not about avoiding bankruptcy —

That’s about preserving a lifestyle you couldn’t afford in the first place.

People take out loans to buy cars they can’t afford,

then pay hefty premiums to protect that reckless choice.

This is not risk management — it’s lifestyle maintenance.

—

Let’s be clear:

Extravagance,

Insurance, and

Investment

are three very different things.

> “Don’t mix them — it’s dangerous!”

Getting comprehensive car insurance to sustain your desire for a flashy new car?

That’s nonsense.

—

Now, of course, cars can be a necessity for some people.

> “I live in a rural area and absolutely need a car for transportation.”

Fair point — that’s consumption, not extravagance.

But if it’s just a means of getting from A to B,

then a cheap used car should do the job.

Yet emotions get involved:

“I just want a nicer car.”

“I deserve to drive something at least this good.”

So they take out a loan.

But loans — especially car loans — are very expensive in the long run.

It’s always better to pay cash upfront, even if that means buying something modest.

A used car worth a few hundred thousand yen is more than enough —

and that way, you don’t need unnecessary car insurance.

If it breaks, fix it.

If it’s totaled, replace it — all within your budget.

The real problem?

People get insurance to cover their emotional overspending, not real risk.

—

【✍️ Summary】

🚗 Types of Auto Insurance in Japan:

Mandatory liability insurance (Jibaiseki)

Optional liability insurance

Comprehensive (vehicle) insurance

—

🎯 Insurance Grades (No-Claim Discount system):

No accidents? Your rate goes down.

One accident? Expect a 3-grade drop and a rate hike.

—

✅ What insurance is actually necessary?

Unlimited coverage for personal injury & property damage to others

—

🔍 How to review your policy:

Reconsider the insurance provider

Reevaluate your coverage conditions

Drop comprehensive/vehicle insurance if unnecessary

—

💥 Bottom line:

Vehicle insurance is for people who can’t afford repairs.

Don’t confuse necessities (consumption) with luxuries (waste).

“Mixing them is dangerous!”

Special Thanks OpenAI and Perplexity AI, Inc