「同じ積立でこれだけ差が出る|将来を見据えた賢い選択を」

~前回のつづき~

●“学資”と書いて、“損失”と読む保険~“貯金感覚”で保険を選んだ人の末路~

学資保険の考察をすると

積立保険の利回りというのは

会社・商品によって違いますが

年間0.7%程度が多いです。

という意見も

あるかと思いますが

これは大きな間違いです。

なかなか解約が出来ないなど

厳しい条件が付いています。

利回り0.7%で

20年間もしも

3万円ずつ積み立てた場合

20年後に

772万円になります。

20年✕12ヶ月✕20年=720万円

自分で積み立てた貯金で

772ー720=52万円

52万円分が増えた貯金分です。

20年間で

約50万円しか増えません。

と思うかもしれませんが

20年間は結構長いです。

これを投資の利回りが

もっとまともな商品に投資した場合

どうなるか?

仮に

7%で運用できたとしましょう。

7%が高い・安いと

色んな意見があるかと思いますが

私は全然

現実的な数字だと思っています。

それはまた

別の機会にお話しします。

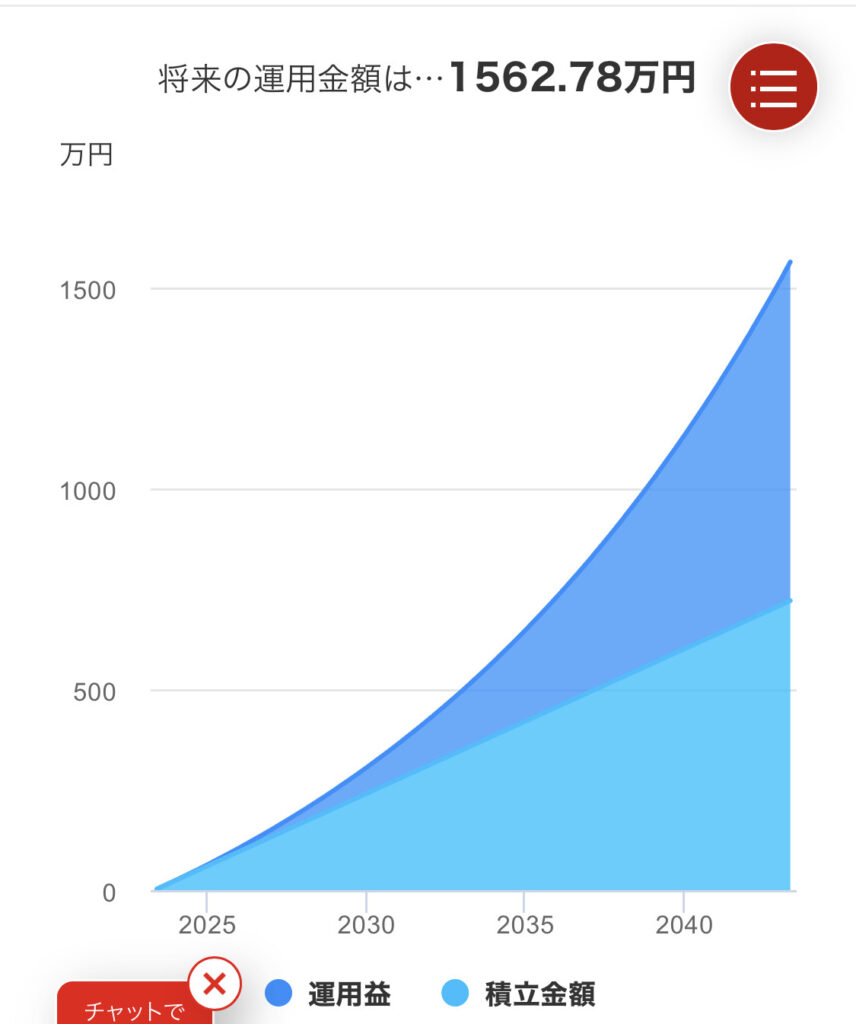

20年間3万円を積立てて

7%で運用した場合いくらになるか?

1,562万円になります。

積み立てた年数も金額も一緒なのに

1,562-772=790万円

差がつくことになります。

すごい差ですよね?

「株と投資信託と他の投資商品と

一緒にしてくれるな!」

という声が聞こえてきます。

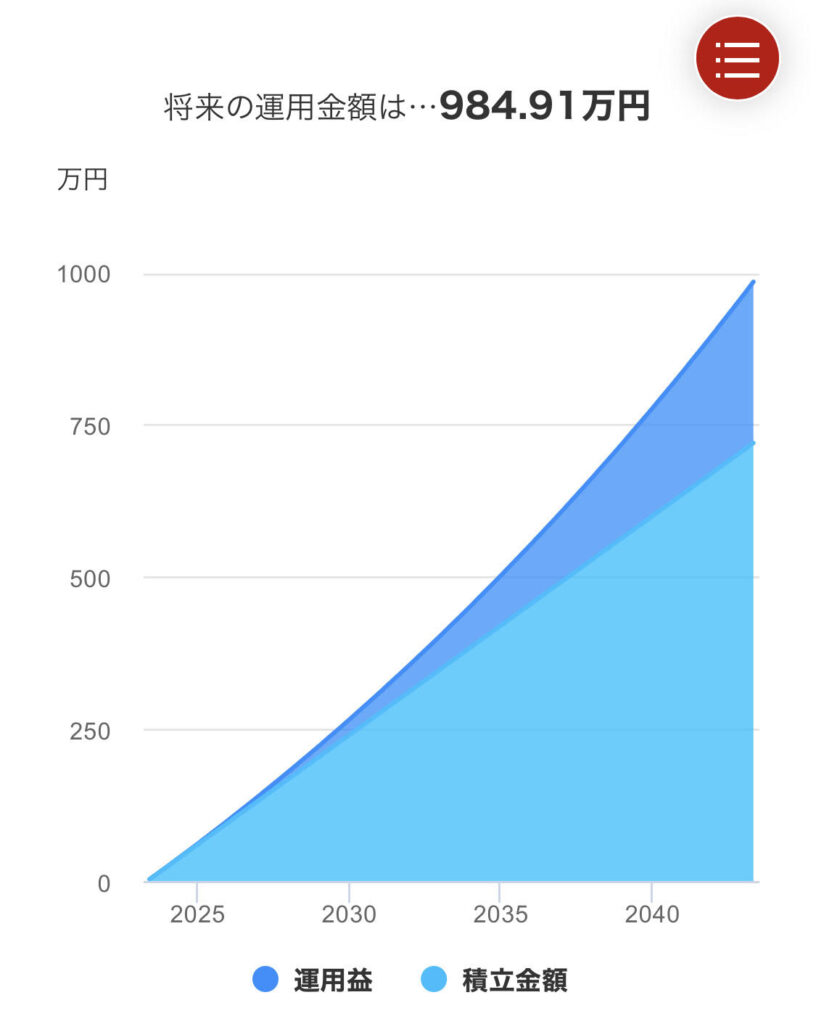

では比較的安全な

3%で運用したらどうでしょう?

約985万円になります。

保険であれば

772万円にしかならなかったのが

自分で安全に投資しても985万円

985-772=213万円

差がつきます。

というご意見もあるでしょう。

積立保険は

掛け捨て保険と投資信託が

セットになったものです。

(これは少しややこしいので

ここでは割愛します)

要は

非常に高い投資商品を

買っているんです。

そういう認識を

持っていただきたい。

積立保険は

死亡時の保証が付いてるとはいえ

ほとんど機能しないというのが

現状です。

貯蓄性のある保険は

補償が非常に薄いんです。

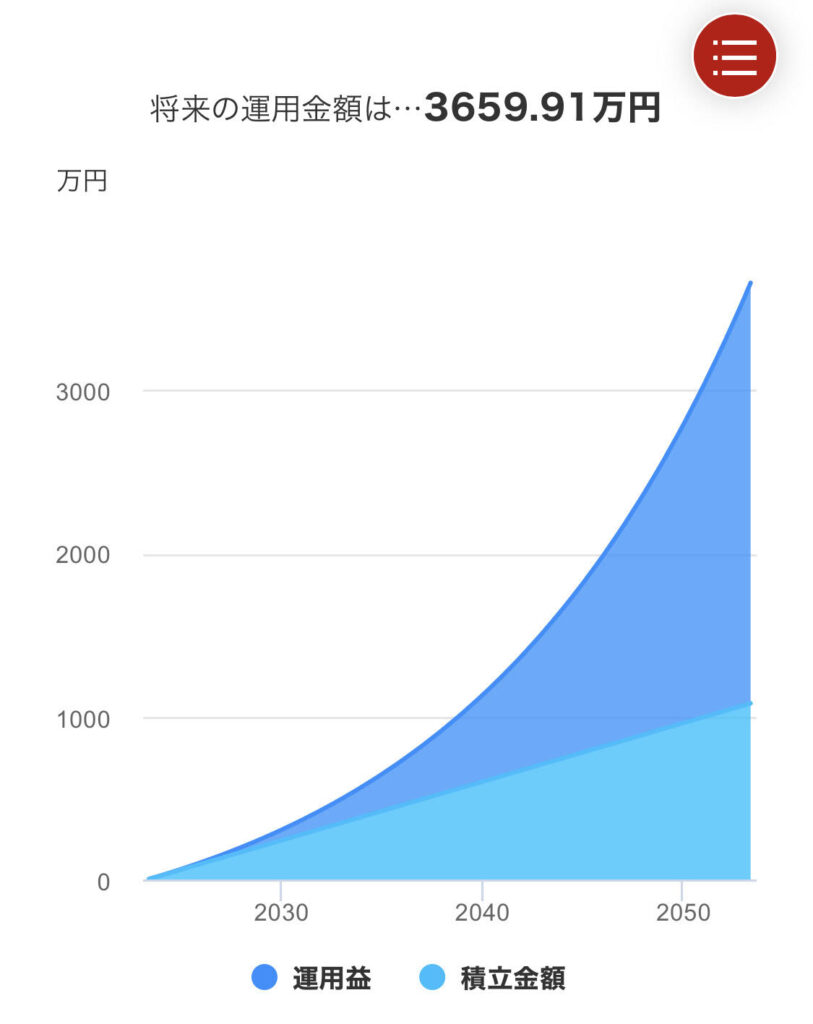

20年で

これだけ差が付くのであれば

30年だとどうか?

毎月3万円を

30年間積み立てた場合

7%の利回りで理屈上は

約3,660万円になります。

引き出す場合も

保険より非常に柔軟です。

同じ積立でこれだけ差が出るんです。

この認識をお持ちいただきたい。

積立保険というのが

同じ投資商品として見た場合

どれだけ利回りの悪いものなのか

という所については

理解しておいて下さい。

貯金をしたいのであれば

いつでも引き出せる状態に

しておく必要がある。

保険のリスクは

すぐに引き出せないんです。

貯蓄をしたいのであれば

貯金でOKです。

わざわざ難しい保険を

買わなくてもいい。

「あと10年したら元本割れしないので

とにかく損をしたくない!」

気持ちはわかります。

人間は損をしたくない動物です。

積立保険というのは

入ってしまった段階で

損失が確定してしまっています。

ほぼ損をする。

残念ですが

そのような認識をしておいて下さい。

なので

少しでも積立金額が少ない間に

解約してしまうのが得策です。

「損しないタイミングで 解約すればいいじゃないか!」

「あと何年かしたら

とりあえず元本分は帰ってくる!」

それであれば多少損してでも

戻ってきた金額を

他の投資に回してしまった方がいいです。

その方がお得です。

計算してもらえば分かると思います。

いま10万円損しないかわりに

将来数十万円を損する。

それを損したくないが為

に大きな何百万円

もしかして何千万円に

なったかもしれない将来の資産を

損してしまうということになる。

もったいないと

思うかもしれませんが

基本的にはほとんどの人が

今すぐ解約した方がいいです。

●返せなくなったとき、守ってくれるのは“家族”か“団信”か~団信は最後の保険~

住宅ローンには

団信(団体信用生命保険)という

保険があります。

住宅ローンを借りる人向けの

生命保険です。

もしも

家のローンを借りてる

借主の旦那さんが

死亡した場合や

高度障害になった場合

住宅ローンの残債

つまり残りの払わなければいけない金額が

免除になるシステムです。

その後は

その家にローン返済なし

すなわちタダで住めるわけです。

ローン残高は保険でゼロになって

家は遺族のものになるんですよ。

保険料は多くのケースでは

住宅ローンの金利に上乗せされている形で

支払っており

別途支払うわけではありません。

メリットとしては

・万が一のときに家族にローンを残さず家を残せる

・手続き不要でローンが完済される

デメリットとしては

・健康状態によって加入できない場合がある

・がん団信などは保険料(=金利)が割高になる

注意点としては

・高度障害の定義はかなり厳格(例:両目失明、手足の完全麻痺など)

・一度加入した団信の条件をあとから変えることは基本的に難しい

・加入前に持病がある場合、告知義務がある

民間の金融機関(銀行など)で

住宅ローンを組む場合は

原則加入が必須です。

フラット35(長期固定金利型の住宅ローン)では

団信は任意です

(ただし加入しないと金利が若干下がる代わりにリスクが残る)。

●“不安だから”貯めてるあなたへ~何があれば安心なんですか?~

一体何が不安なのか!?

不安を煽られる時代なので

不安になってしまうのはわかります。

何が不安なのか

考えていかなければならない。

いくら貯まったら安心なのか。

気持ちはわかります。

ではその「いざ!」が

・一体どんな時で

・いくらいるのか

ちゃんと数字で

考えておく必要があります。

●“家族に残したい”なら貯蓄型を選ぶ理由はない~保険にお金を預けるな~

気持ちはわかります。

自分に何かあった時に

家族にお金を残したい。

それだったら

掛け捨ての生命保険で

十分なんですよ。

貯蓄性のあるものにする

必要はありません。

掛け捨ての生命保険で

十分です。

これは

本来の生命保険の

意味があります。

『生命保険 掛け捨て』

で検索すれば

見切れないぐらい

たくさん商品ページが

検索結果として出てきます。

月々2,000円の支払で

死亡時1,000万円ぐらい貰える商品が

ゴロゴロあります。

Google先生に

ちょっと聞いてみるだけで

メチャクチャ出てきます。

というのであれば

支払金額を足せば

保証額は上がります。

興味があれば調べてみて下さい。

~~~つづく~~~

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

学資保険や積立型保険は、利回りが年0.7%程度と低く、銀行預金よりは良いように見えても、解約しづらいなどの制約が多いのが実情です。

例えば毎月3万円を20年間積み立てても、増えるのは約50万円程度にとどまります。

一方、同じ金額を年7%で運用できる投資商品に回せば1,500万円以上、年3%でも約1,000万円になり、保険との差は歴然です。

積立保険は死亡保障が付いているものの、保障内容は薄く、投資商品としては割高です。

貯蓄や資産形成が目的なら、柔軟に引き出せる普通の貯金や投資の方が有利です。家族にお金を残したい場合も、掛け捨ての生命保険で十分な保障が得られます。

保険で貯蓄をするより、目的に応じて投資や保険を分けて考えることが賢明です。

[1] https://my-best.com/1948

[2] https://www.hokende.com/life-insurance/education

[3] https://hoken-all.co.jp/article-5358/

[4] https://www.hokende.com/life-insurance/education/ranking

[5] https://www.behavior.co.jp/blog/life-insurance-rate-2025

[6] https://www.behavior.co.jp/blog/education-fund-nisa-vs-plan

[7] https://www.nanairolife.co.jp/hoken/educational-insurance-recommendation/

[8] https://konohoken.com/child-education/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Previous Post~~

【”Educational Insurance” is Read as “Loss” Insurance~The Fate of Those Who Chose Insurance Like a Savings Account~】

When examining educational insurance,

The return on savings-type insurance varies

by company and product,

but most commonly, it’s about 0.7% annually.

> \[Speech bubble] “That’s better than a bank!”

Some might say that,

but that’s a huge misconception.

These plans come with strict conditions,

like making it difficult to cancel.

Let’s say you save ¥30,000 per month

for 20 years at a 0.7% return rate:

In 20 years, you’ll have about ¥7.72 million.

But the amount you actually saved is:

20 years × 12 months × ¥30,000 = ¥7.2 million

The increase is: ¥7.72M − ¥7.2M = ¥520,000

So in 20 years, it only grew by ¥520,000.

> “Still, an extra ¥520,000 isn’t bad.”

You might think so,

but 20 years is a long time.

What happens if you had invested

in something with a reasonable return?

Let’s say you invested at 7% annual return.

Now, 7% may sound high or low,

depending on who you ask—

But I personally believe

it’s a realistic number.

(I’ll explain why another time.)

So, how much would ¥30,000/month for 20 years

grow at 7%?

It would become about ¥15.62 million.

With the same amount and duration of saving,

that’s a difference of: ¥15.62M − ¥7.72M = ¥7.9 million

That’s a huge difference, right?

> “But the risk is totally different!”

> “Don’t compare stocks and mutual funds

> with insurance!”

I hear you.

So how about a safer investment at 3%?

It would become about ¥9.85 million.

Whereas the insurance plan only gave you ¥7.72 million,

even a relatively safe 3% investment gives you ¥9.85 million.

That’s a ¥2.13 million difference.

> “But savings insurance comes with death benefits!”

Yes, some might argue that.

But savings-type insurance

is basically a combo of term insurance and mutual funds.

(It’s a bit complicated, so let’s skip the details here.)

Bottom line:

You’re buying a very expensive investment product.

Please understand it that way.

While it includes a death benefit,

in reality, it barely functions.

Insurance with a savings element

tends to have very limited coverage.

If this much difference happens over 20 years,

what about over 30 years?

If you save ¥30,000/month for 30 years

at 7% return, in theory, you’ll have:

¥36.6 million.

Also, you have much more flexibility in withdrawing your money

compared to insurance.

Same savings, but huge difference in outcome.

Please keep this in mind.

When viewed as an investment product,

savings-type insurance has terrible returns.

If your goal is saving,

you need to be able to access your money anytime.

With insurance, you can’t.

If you want to save, just use a regular savings account.

You don’t need to buy a complex insurance product.

> “But won’t I lose money if I cancel now?”

> “In 10 years, I won’t be in the red—

> so I don’t want to lose now!”

I understand how you feel.

People are wired to avoid losses.

But with savings-type insurance,

you’ve already locked in your loss the moment you signed up.

In most cases, you’re going to lose money.

It’s unfortunate, but that’s the reality.

So, the smart move is to cancel early,

while your contributions are still low.

> “I’ll cancel at the break-even point!”

> “If I wait a few more years,

> at least I’ll get my principal back!”

If that’s the case,

you’re better off investing that money elsewhere

even if you take a small loss now.

You’ll come out ahead in the long run.

Just run the numbers.

Avoiding a ¥100,000 loss now

could mean losing hundreds of thousands later.

You might even lose out on millions

in future asset growth.

It may feel wasteful,

but most people are better off cancelling now.

—

Who Will Protect You When You Can’t Pay Anymore?

Your Family or Group Credit Life Insurance (Dan-shin)?

Dan-shin is the Last Line of Defense

Housing loans come with

Group Credit Life Insurance (団信 / Dan-shin).

This is a life insurance policy

for people taking out home loans.

If the borrower—usually the husband—dies

or becomes severely disabled,

the remaining mortgage balance

is forgiven.

After that, the family can live in the home

without paying the loan.

The balance is wiped out by insurance,

and the house becomes the family’s asset.

In most cases, the insurance cost

is included in the mortgage interest rate—

you don’t pay it separately.

Advantages:

Your family won’t be left with debt if something happens

The mortgage is paid off automatically—no paperwork required

Disadvantages:

You may be ineligible if your health isn’t good

Special policies like cancer coverage often come with higher rates

Things to note:

The definition of “severe disability” is very strict (e.g., total blindness, full paralysis)

You can’t change the conditions after enrolling

If you have a pre-existing condition, you must disclose it

With private banks, enrollment is usually mandatory.

With government-backed “Flat 35” loans, Dan-shin is optional,

but skipping it lowers interest slightly and increases risk.

—

To Those Saving Out of “Anxiety”—

What Exactly Are You Anxious About?

What exactly are you afraid of?

It’s a fear-driven society,

so it’s natural to feel anxious.

But you have to examine:*What are you afraid of?

How much savings would make you feel secure?

> “Just in case something happens…”

I get it.

But that “something”—

What exactly is it?

How much money would it require?

You need to put numbers to those scenarios.

—

If You Want to Leave Money for Your Family,

There’s No Reason to Choose Savings-type Insurance

~~Don’t Entrust Your Money to Insurance~~

> “I want to leave money for my family!”

I understand the sentiment.

You want to provide for your family

if something happens to you.

But in that case,

term life insurance is more than enough.

You don’t need savings-type policies.

Term life insurance is sufficient.

That’s what life insurance is meant to be.

Just search “term life insurance” online—

you’ll find countless options.

You can get plans that pay out ¥10 million

for monthly premiums of just ¥2,000.

Seriously—just ask Google.

You’ll get more options than you can count.

> “But ¥10 million isn’t enough!”

Then just increase your premium,

and your coverage goes up.

If you’re interested, do some research.

Special Thanks OpenAI and Perplexity AI, Inc