「お金がお金を呼ぶ|投資で未来を切り拓く不労所得の魔法」

~前回のつづき~

●20年後に笑うのは“今”投資を始めた人~月5万円の選択が1400万円の差になる未来~

あなたは今現在

投資に馴染みが無いかもしれません。

毎月5万円貯金は出来るとして

20歳〜10年間貯めたら

いくらになりますか?

年間60万円ですよね?

10年間貯めると

600万円貯まります。

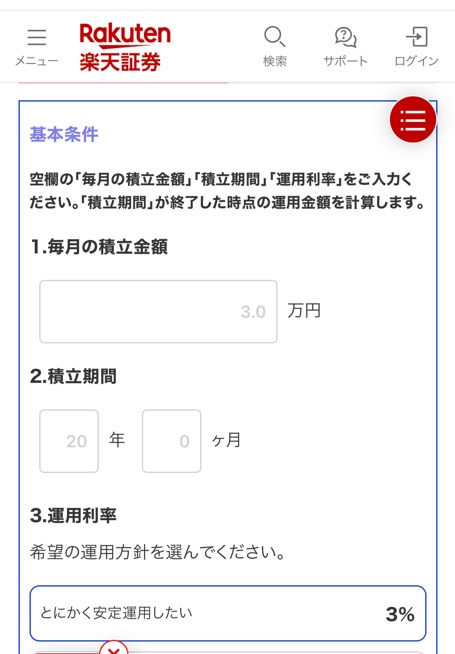

楽天証券のサイトに

という便利なサイトがあります。

(図1)

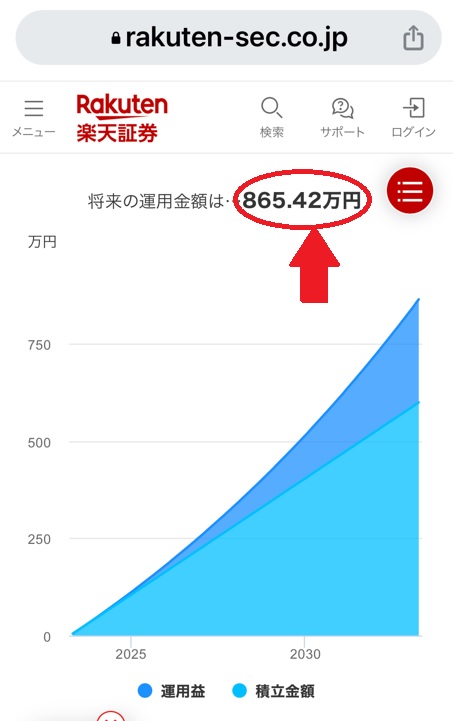

毎月5万円を

10年間投資利回り7%で運用すると

865.42万円になります。

(図2)

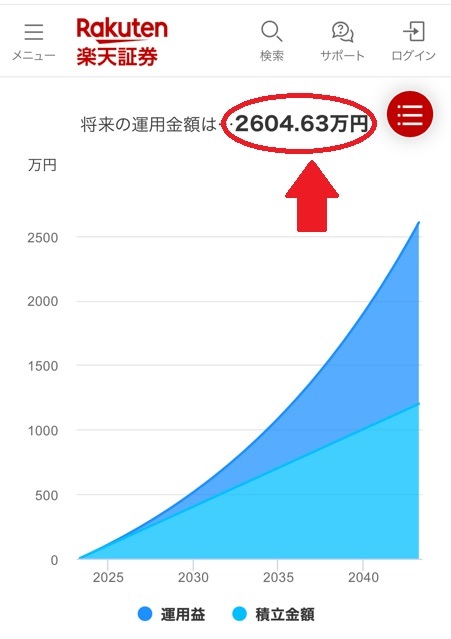

もしこれを20年続けたら

どうなるかというと

(図3)

2604.63万円になります。

結構すごくないですか?

普通に貯金だけしていたら

1200万円です。

その差

2600ー1200=約1400万円。

これが

『お金がお金を呼ぶ』という事です。

\NISAやるなら/

アインシュタインが

この世で一番大きな力は何かと

尋ねられた時に

『複利の力』と答えたという

エピソードがあります。

お金がお金をドンドン産んでいく

というのが複利の力です。

今年1万円増えたものが

また来年更に増えた1万円が

働いてくれるという状態です。

もしも20年前に

100万円を投資したら

いくらになっていたのか?

というサイトがあります。

登録して

運用したい数値(パーセンテージ)を

入力していきます。

(図4)

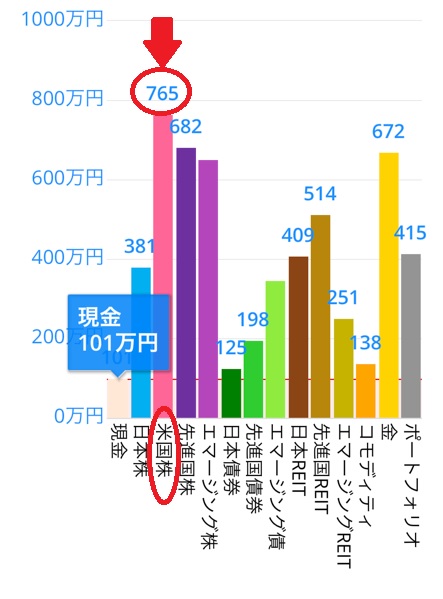

現金が101万円になっています。

これは預金にしていた場合です。

それ以外で増えているのが

日本株や米国株などがあります。

このグラフを見ると

・現金預金しておくと増えない

・米国株に入れると765万円に増える

(図5)

その他に投資しても

ただ貯金しておくよりも増えています。

ちなみに『エマージング』というのは

新興国のことで

まだまだこれから

伸びてくる国のことです。

現金で持っていると

一番増えてませんよね?

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

投資に馴染みがない方でも、毎月5万円を貯金することはできるかもしれません。

しかし、単に貯金するだけでは20年後に1,200万円にしかなりません。

一方、年利7%で毎月5万円を積み立て投資した場合、20年後には約2,600万円に増え、その差は約1,400万円にもなります。

これは「複利の力」によるもので、お金がお金を生み出し、時間が経つほど増え方が加速します。

実際、過去20年間で100万円を現金で持っていた場合ほとんど増えませんが、米国株などに投資していれば大きく増えていました。

将来の資産形成には、早くから投資を始めることが非常に重要です。

Citations:

[1] https://www.fsa.go.jp/policy/nisa2/tsumitate-simulator/

[2] https://www.rakuten-bank.co.jp/assets/intermediation/charm/tsumitate.html

[3] https://itf.minkabu.jp/simulation/calculator

[4] https://www.am-one.co.jp/shisankeisei/simulation.html

[5] https://diamond.jp/zai/articles/-/1036203

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Previous Post~

【Those who start investing now will be the ones smiling in 20 years — A ¥50,000/month choice that could mean a ¥14 million difference.】

You might not be very familiar with investing right now.

But let’s say you can save ¥50,000 each month.

If you start saving at age 20 and continue for 10 years,

how much will you have?

That’s ¥600,000 per year,

which means ¥6,000,000 over 10 years.

There’s a helpful tool on the Rakuten Securities website called

Rakuten Easy Investment Simulation.

(Figure 1)

If you invest ¥50,000 per month for 10 years with a 7% annual return,

you’d end up with ¥8,654,200.

(Figure 2)

And if you continue this for 20 years?

(Figure 3)

You’d have ¥26,046,300.

Pretty amazing, right?

If you only saved that money, you’d have ¥12,000,000.

So the difference is:

¥26 million − ¥12 million = roughly ¥14 million.

This is what it means when people say,

“Money makes more money.”

There’s a famous story that when Einstein was asked what the greatest power in the universe was,

he answered: “The power of compound interest.”

That’s the concept where money grows on top of money.

For example, if you earn ¥10,000 this year,

next year you’re also earning returns on that extra ¥10,000.

Now, what if you had invested ¥1 million twenty years ago?

There’s a site called Minna no Portfolio (Everyone’s Portfolio)

where you can input your desired asset allocation and see results.

(Figure 4)

If you had just kept it in cash, it would now be worth ¥1,010,000.

But investments in Japanese or U.S. stocks grew significantly more.

From the graph:

Cash doesn’t really grow.

U.S. stocks would have turned ¥1 million into ¥7.65 million.

(Figure 5)

Other asset classes also outperformed simple saving.

By the way, “Emerging” refers to emerging markets—

countries that are still developing and have high growth potential.

So when you just hold onto cash,

you’re getting the lowest return.

Special Thanks OpenAI and Perplexity AI, Inc